“Sanctions for Sanctions Violation”: U.S. Department of Treasury Enforcement Actions Against the Financial Sector

In

Login if you are already registered

(votes: 1, rating: 5) |

(1 vote) |

Ph.D. in Political Science, Director General of the Russian International Affairs Council, RIAC member

Both Russian and foreign researchers have done much to study U.S. sanctions policy. Many focus on “initiator-target” relations, i.e. on state vs. state dyads. However, the U.S. government runs a proactive policy to enforce compliance from both business at home and abroad with the U.S. sanctions regimes. Literature often omits this state vs. business relationship, although business behavior may be crucial to promote or block the isolation of target-states. For business itself, sanctions pose a considerable political risk, fraught with material and reputational loses; the financial sector is under special risk. The article studies the U.S. Department of Treasury’s enforcement actions against financial companies. It raises the following questions: Why is the financial sector the most vulnerable to enforcement? What is the nature of risk for these companies – is it a result of the “special approach” of the government, or a consequence of structural features of the financial sector itself? Why do financial companies violate sanctions regimes? What are the strategies these companies have to deal with the U.S. government and to manage the risk? The research tests three hypotheses. (1) The financial sector suffers due to structural reasons; (2) Companies violate sanctions regimes due to reckless, rather than willful behavior; (3) They prefer to cooperate with the government and improve compliance rather than further conceal violations and repeat them. This rather shows how efficient the U.S. enforcement actions are at changing the behavior of business in financial sector. Testing these assumptions implies analysing 54 cases of enforcement actions against financial companies in 2009-2020, in comparison with a wider sample of 215 cases of other sectors of economy.

Article first published in Polis. Political Studies Journal (2020. No. 6. P. 73-90).

Timofeev I.N. “Sanctions for Sanctions Violation”: U.S. Department of Treasury Enforcement Actions against Financial Sector. – Polis. Political Studies. 2020. No. 6. P. 73-90. (In Russ.) https://doi.org/10.17976/jpps/2020.06.06

Economic sanctions are becoming an increasingly popular tool in U.S. foreign policy. In the 20th and early 21st centuries, the U.S. imposed sanctions more frequently than all other states and international organizations together, including the UN [Hufbauer et al. 2009: 89]. These sanctions are often imposed without the approval of the UN Security Council; that is, they are unilateral restrictive measures. The U.S. 2017 National Security Strategy sees sanctions as an element of containment and instrument for restricting adversaries' international potential. Such restrictions have long been used as a foreign political tool [Djazairi 2015], yet American sanctions policy has manifested several important trends for the last two decades.

First, instead of the sweeping embargoes typical of the 20th century, America’s restrictive measures have become more specifically targeted [Drezner 2015]. They are now aimed against specific persons, organizations or economic sectors. Previously, sanctions policy could be compared to area attacks; today, it could be compared to target shooting, which does not necessarily entail less damage. If targeted sanctions are imposed on companies that have strategic importance for a state, they could have extremely grave consequences [Gordon 2019] as they negatively affect the state’s population [Servettaz 2014]. Sanction policy is transformed into a policy of compiling “lists” of politically suspect persons and companies. It can be seen as part of a broader trend to compile security-related “blacklists” on an extremely broad range of issues [de Goede, Sullivan 2016].

Second, financial restrictions are beginning to play a greater role than trade sanctions. This development has been spurred by the globalization of financial markets, by the importance of the U.S. dollar as universal tender, and by the significant role American banks play in global payments. U.S. authorities have gained broad opportunities for tracking financial transactions around the world. Following the 9/11 terrorist attacks, the U.S. tightened its control over the banking sector, intending to combat international terrorism [Zarate 2013]; however, the side effects included the USA's supervisory powers expanding both domestically and internationally. Additionally, financial sanctions as such are fraught with a banking sector crisis in the targeted country, i.e., they could cause it major damage [Hatipoglu, Peksen 2018].

Post-COVID-19 Sanctions Policies

Third, the U.S. is making increasing use of extra-territorial restrictions punishing both American and foreign individuals and legal entities for violating American sanctions. This practice skews states’ sovereignty in favor of the U.S. Companies from the EU, Russia, China and other states prefer to comply with American sanctions, although, at the level of politics, their governments condemn Washington’s unilateral sanctions. National regulators are not always able to protect their businesses against actions taken by American authorities.

Such trends have transformed the political risks faced by international business. Any company can be hit by U.S. restrictive measures for deliberately or accidentally violating American sanctions regimes. These measures include monetary fines proportionate to the volume of the prohibited transactions. Unlike the harsher blocking sanctions, fines allow companies to continue operating, but they are fraught with major financial damage stemming from both paying the fine and from the costs of investigating the violations [Guerello et al. 2019].

The financial sector has found itself in particularly dire straits. A recent study of the fines imposed by the U.S. Department of the Treasury showed that banks account for a significant chunk of such payments [Timofeev 2019]. Compared to businesses working in other sectors, financial institutions are also fined more often. In other words, banks are particularly vulnerable to the consequences of violating U.S. sanctions regimes.

This situation suggests several avenues for research. Why are financial institutions the leaders in the number of violations and in payments made? What is the nature of the political risks for banks? Are they a consequence of the U.S. authorities’ special approach or do they result from the distinctive structural features of the financial sector? Why do banks violate U.S. sanctions regimes? Are they after superprofits or do they make management mistakes? Finally, what strategies do banks employ in interacting with the U.S. authorities? Do they cooperate? What are their strategies for minimizing their risks? These questions are also related to the more fundamental issue of research into the effectiveness of sanctions. Specifically, do sanctions induce change in the target's conduct? Why do they work in some cases and fail in others?

We propose the following hypotheses as answers to these questions: (1) the financial sector is particularly vulnerable owing to the distinctive internal (structural) specifics of the way it does business. The U.S. government applies to these the same rules as it applies to other businesses, but the nature of banks' activities (transaction volume, complicated structure) makes it particularly difficult for banks to comply with these rules compared to other sectors. (2) A 2019 study [Timofeev 2019] demonstrated that most companies commit such violations accidentally. This observation probably holds for banks as well. Payment volumes, however, suggest that the number of deliberate and “egregious” (as the U.S. authorities say) violations could be higher in the financial sector. (3) Banks cooperate with the U.S. authorities and improve the system for tracking possible violations. This conduct is generally typical of businesses that are liable to be fined. It means that the U.S. government is effective in forcing the international banking sector to comply with the restrictions and, consequently, to support the financial blockage of states on which the U.S. has imposed sanctions.

Key Concepts and Scholarship Overview

Economic sanctions consist of a set of restrictions in trade, finance, licensing, and other areas; these restrictions are used by the initiator state or by a group of such states against certain organizations or individuals. Sanctions are intended to induce the targeted state to modify its “conduct,” change its foreign or domestic policies. Scholarship usually considers three tasks that sanctions are intended to handle: coercion, constraining, signaling [Giumelli 2016]. Sanctions are different from trade wars [Pape 1997: 94-98]. In the former case, economic restrictions are used to political ends; in the latter case, tariffs and duties are used to create favorable conditions for domestic manufacturers. American law and administrative practices distinguish clearly between sanctions and a policy of duties and tariffs.

The U.S. imposes sanctions through executive orders or acts adopted by Congress and then signed into effect by the President. These documents may stipulate sanctions as general regimes (such as restricting a certain type of activity) or as restrictions on specific persons or organizations acting independently or on behalf of the targeted state. U.S. executive bodies are vested with the powers to expand these lists and apply restrictive measures. Such sanctions may be called “primary”: they are imposed directly on persons or entities on a blocklist or under a regime introduced by an act of Congress or by an executive order.

“Secondary” sanctions are restrictions against those who are somehow connected with the persons or organizations under “primary” sanctions, against those who act on their behalf or in their interests. They can be seen as “sanctions for violation of sanctions.” Some sources identify “secondary” sanctions with applying restrictions on foreigners, i.e., with extra-territorial sanctions (see, for instance, [Geranmayeh, Rapnouil 2019]). However, American regulators have imposed “sanctions for violation of sanctions” on U.S. citizens and organizations as well. Moreover, American citizens and organizations were initially the key subjects of legal rules. American administrative vocabulary also includes the “enforcement actions” concept; these actions target both Americans and foreigners. Although there is no generally accepted “secondary sanctions” concept, it appears expedient to use it in this particular meaning without reducing it solely to extra-territorial measures.

Several U.S. agencies are in charge of monitoring sanctions compliance. The Department of State supervises visa prohibitions and restrictions on weapons exports. The Department of Commerce supervises compliance with restrictions on selling American goods or foreign-made goods with American-made parts. The Department of Justice prosecutes cases of, for instance, premeditated conspiracy to violate a sanctions regime. Finally, the Department of the Treasury is in charge of a broad range of issues related to imposing sanctions on and restricting the activities of persons and organizations already hit by sanctions. The Department of the Treasury bears the greatest load of supervising sanctions compliance.

The Department of the Treasury has three principal enforcement options. The first is to block a violator company and put it on the so-called SDN list (Specially Designated Nationals and Blocked Persons List). SDN status means a virtually blanket prohibition on all economic transactions being conducted with such entities and persons. If this step is used as “secondary” sanctions, it means that this particular organization or person is equated with those that had been put on the SDN list under “primary” sanctions or those that had been caught red-handed cooperating with the latter. Recent examples include blocking two subsidiaries of Russia’s Rosneft for conducting transactions with Venezuelan companies on which the U.S. had imposed sanctions (February – March 2020). Blocking China’s COSCO Shipping Tanker and some other transport firms for transporting Iranian oil is another example (2019). Blocking sanctions constitute a very harsh measure that might result in a complete end to the company’s operations. It is highly likely to cease its international activities since banks and partners will fear being hit by U.S. sanctions as well.

The second option is a prohibition on maintaining corresponding accounts or payable-through accounts in U.S. banks, i.e., it essentially means cutting companies and individuals off from the American financial system and prohibiting them from making dollar payments. This measure is rarely applied.

Finally, fines constitute the third option. Fines cause damage to a company or person but still allow them to continue working. Fines are a convenient option against both small and big companies. In the latter case, fines make it possible to avoid shocks to the markets that are inevitable when big businesses are blocked. Fines are different from blocking sanctions in that they are used against “backbone” companies that generally abide by laws and play by the rules, while the SDN list is more convenient for blocking marginal companies that deliberately circumvent sanctions. This article specifically studies fines as a form of “sanctions for violating sanctions.”

Russian researchers have engaged in more active study of U.S. sanctions following the Ukrainian crisis and exacerbated relations with the West since 2014 [Afontsev 2015; Bartenev 2018], although the U.S. policy of imposing unilateral restrictions was previously studied as well (see, for instance, [Shakirov 2011]). Russian scholars studied relations between sanctions and the global economy [Simonov 2015] and investigated sanctions as a foreign policy instrument [Baluyev 2014], the effect of sanctions on the Russian economy [Gurvich, Prilepsky 2016], the relations between sanctions and investment in Russian regions [Kuznetsova 2016], the Russian banking sector’s adaptation to sanctions [Panova 2016], sanctions and the world order structure [Likhacheva 2019], and theoretical schools in exploring sanctions policies [Vaslavsky, Ananiev 2018; Ananiev 2019].

US Elections and Sanctions Against Russia

Foreign researchers have produced a large number of studies. Many works contextualize the issue within the “state-state” link: they assess the impact sanctions spearheaded by an initiator state or a coalition of such states have on the political course of the targeted state. Gary Hufbauer and his colleagues used quantitative methods in their classic monograph [Hufbauer et al. 2009]. Navin Bapat and his team did a huge amount of work: they compiled the TIES (Threat and Imposition of Economic Sanctions) database and produced several articles on different factors that influence sanction effectiveness [Morgan et al. 2014; Bapat et al. 2013]. Of particular interest is the analysis of the effectiveness of sanctions imposed by the UN Security Council [Targeted Sanctions... 2016], as well as analysis of the relationship between UN sanctions and unilateral restrictive measures [Brzoska 2015]. Daniel Drezner’s extensive work, starting with his early studies of the “sanctions paradox” [Drezner 1999] up to his recent assessments of today’s trends [Drezner 2015], also constitutes a major research effort. Studying the damage restrictive measures to the targeted country is a separate issue [Neuenkirch, Neumeier 2015]. There is a series of studies researching individual targeted states [Nephew 2018; Maloney 2015; Graaf 2013].

There are much fewer works studying sanctions from the “state-business” perspective in political science. Moreover, applying the analogy from David Easton’s systems analysis, political scientists and international experts prefer to avoid studying the “black box” and focus more on an analysis of “inputs” and “outputs,” i.e., a set of measures of the initiating countries and the results of their application for the economy and politics of the target countries. The “political kitchen,” or the functioning of state institutions responsible for sanctions as well as their influence on non-state goals, is receding into the background. Meanwhile, sanctions against business are directly related to the target countries because the refusal by business to work with countries that are under sanctions can cause them significant damage, and thus lead to a change in their policies.

This gap is partially filled by literature from related fields, such as jurisprudence, management, economics, and political economy. Many of them highlight the impact that sanctions have had on the financial sector. Sergey Glandin conducted an interesting study on the legal aspects of the U.S. sanctions policy [Glandin, Kadysheva, Keshner 2018; Glandin 2018a, 2018b]. David Restrepo Amariles and Matteo Winkler examined the legal and administrative aspects of U.S. sanctions against banks and their steps to minimize risk [Restrepo Amariles, Winkler 2018]. Steffen Hundt and Andreas Horsch conducted an event-driven analysis of sanctions against banks that violated restrictions that had been imposed on Iran. They revealed serious damage to the banks that were fined, but had little influence on the behaviour of other financial companies [Hundt, Horsch 2018]. However, an article by Stefano Caiazza and his colleagues showed that there has still been an impact on banks that have avoided sanctions, as they have altered their operations in the same way as companies that were fined [Caiazza et al. 2018]. Previous studies by Giampaolo Gabbi and his colleagues showed similar results based on a survey of representatives from 84 financial companies: banks that actively engage in international operations are more inclined to implement risk management mechanisms, fearing financial losses, as well as damage to their reputation [Gabbi, Tanzi, Nadotti 2011], and the existence of such mechanisms mitigates the risks for banks [Delis, Staikouras 2011]. Susan Walker described the impact of sanctions on attitudes towards humanitarian operations – banks are afraid to conduct them under the threat of sanctions [Walker 2017].

Studying specific cases of “secondary” sanctions against banks is of great value. Separate articles are devoted to the cases of Standard Chartered [Rosenzweig 2013; O’Brian 2014], Halkbank [Scott 2019], HSBC [Hardouin 2017], and JPMorgan Chase [Lee, Doddy 2011]. Reviews of a series of cases or their generalizations are also of interest, including in the context of the powers of federal and state authorities [Scott 2020; Kline 1999], as are analyses of the effectiveness of sanctions [Anglin 2016]. Researchers are also intrigued by the problem of the electronic screening of transactions for compliance with sanctions legislation [Evans 2010; Bamberger 2010], as errors in such programmes often lead to unintentional violations of sanctions regimes.

Studies carried out by lawyers, economists, and management specialists usually focus on individual cases or patterns of compliance practices. With a few exceptions, there is a clear lack of holistic studies that combine cases into single databases. This gap again takes us back to the methodology of political science. In a similar vein, Bryan Early and Keith Preble conducted a study to investigate cases where the U.S. Department of the Treasury imposed fines on international business [Early, Preble 2018]. In Russia, a similar study was carried out in 2019, albeit with different approaches to creating and analysing a database [Timofeev 2019]. However, in these works, companies in the financial sector are not placed into a separate category even though they are the ones that are subjected to the greatest burden in terms of fines, and thus the political risk associated with sanctions is the most pronounced for them. The purpose of the article is to fill in this gap in the literature.

Study Design

The imposition of sanctions by the U.S. Department of the Treasury and its Office of Foreign Assets Control (OFAC) is extensively regulated by 2009 guidelines that set several important parameters. First, the amount of the fine depends on the volume of transactions. Second, it is influenced by a number of aggravating and mitigating circumstances, the key ones being (1) whether the violation is voluntarily or involuntarily disclosed, and (2) whether the violation is classified as egregious or non-egregious. The latter is determined by a set of criteria which include: willful or reckless violation; and the availability of information on the violations and the damage caused to the U.S. sanctions programme. Additional circumstances include: the level of cooperation with the U.S. authorities, the size of the company and the specifics of its organization, the volume of transactions, the history of violations in the past, the existence of a compliance service (that monitors compliance with legislation), measures taken to mitigate the situation, and so on. The fine is structured so that the company bears responsibility in proportion to the financial scope of the prohibited transactions. It is beneficial for companies to cooperate with the authorities, take measures to rectify violations, voluntarily disclose violations, and not violate sanctions regimes in the future. In this case, they can count on a substantial discount from the base penalty and avoid the statutory maximum. Other agencies, such as the Department of Commerce or the Department of Justice, may conduct investigations concurrently with the Department of the Treasury. They can impose their own fines.

The investigation results in the Department of the Treasury and the company that committed the violation (or individuals in rare cases) reaching an agreement that details the amount of the fines (maximum possible, basic, final), the essence of the case, aggravating and mitigating circumstances as well as measures taken by the company to remedy the situation. The agreements are prepared in accordance with the 2009 guidelines and have a similar structure. The same organizational technique and more or less standardized outcomes make it possible to encode information in numerical form and create a single and comparable database in which the unit consists of a separate agreement. For example, the voluntary disclosure of a violation by a company may be coded as “1,” or as “0” if no such voluntary disclosure was provided. This procedure helps to enhance the level of the information obtained by transforming it from miscellaneous documents into a single database. The Department of the Treasury itself provides generalizations on closed and current cases and gives practical recommendations on how to avoid fines on this basis.

One drawback is that the regulator does not always detail the full set of circumstances in the agreement and sometimes they are not classified. However, even in this case, a very impressive amount of factual data can be obtained, and the lack of classification may be regarded as information.

The author’s U.S. Department of Treasury Office of Foreign Assets Control Enforcement Actions Database includes 72 variables. They can be divided into several groups: (1) information about the company (name, country, industry); (2) information about the fine (maximum, basic, final); (3) information about aggravating and mitigating circumstances; (4) information about measures taken to remedy the situation; (5) information about the regulators that were involved in the investigation. Data has been collected on 215 cases over the course of more than ten years (2009-2020).

The array that is obtained separates companies in the financial sector represented by banks. This only rarely includes payment systems (PayPal), brokerage services (Zulutrade), credit card processing companies (First Data) or a credit union (UN Federal Credit Union). Financial companies do not include, for example, insurance companies, as they have their own cluster and should be the subject of a separate study. Next, a statistical analysis of data on the financial companies is carried out, which is compared with data for the entire set of observed cases.

Analysis

The financial sector clearly stands out from other industries with respect to the number of fines imposed, accounting for 54 of 215 cases over the past ten years. In terms of the number of fines, the financial sector is followed by oil service companies (17 cases), manufacturing enterprises (17), medical equipment suppliers (14), insurers (14), logistics and transportation companies (12), and travel, trade, and telecommunications companies (10 each). There are only isolated cases in other industries (see Fig. 1). A much more important feature, however, is the proportion of payments made by the financial sector. A total of USD 5.656 billion was paid in 215 cases from 2009 to 2020. Financial companies accounted for USD 5.271 billion of this amount, while other sectors accounted for only USD 385.2 million. In other words, financial sector companies paid 93.2% of fines, although they make up a mere 25.2% of the total number of cases, while 74.8% of other companies only paid 6.8%. There is a clear asymmetry that does not work in the favour of banks.

Figure 1 [1] . Number of OFAC Financial Penalties: Distribution by Industry (2009-2020)

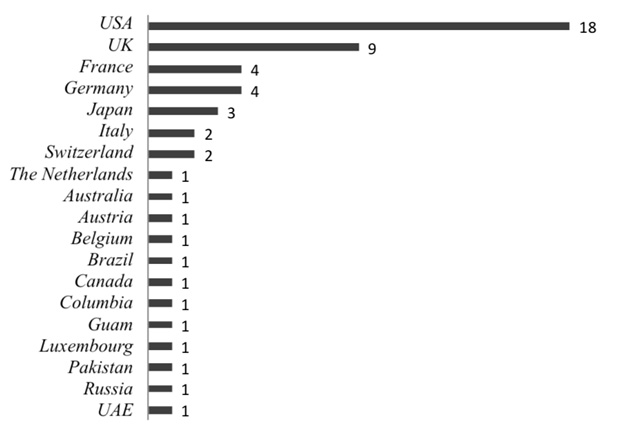

Of the 54 fines imposed on the financial sector, only 18 of them were in the United States (see Figure 2) even though U.S. companies account for the majority – 142 out of 215 companies – in the sample for all sectors. The financial companies that were fined include 23 in the EU (including the UK). Interestingly, the banking group also has its own asymmetry. Twenty-three banks from EU countries (including the UK at that time) paid USD 4.587 billion of USD 5.271 billion (87%), while all the rest paid only USD 683 million (13%). This “European paradox” was analysed in a recent work [Timofeev 2020] and can be explained, among other things, by the belated reaction of EU companies to U.S. legislative requirements.

Figure 2. Number of OFAC Financial Penalties: Distribution by Country (2009-2020)

If we rank the companies in terms of the amount of fines, the “top” 50% of companies account for more than 99% of all payments. The first quartile (25% of the “leaders”) accounts for 91.4% of payments, and the first decile (the five “leaders”) accounts for 62.8%, i.e., five companies alone paid significantly more than half of all fine payments, while eleven paid 91.4% of the amount. All these companies are European. As a whole, we have three asymmetries: (1) sectoral – the financial sector accounts for the majority of payments; (2) regional – most of the payments are made by European banks; (3) intra-industry – only a quarter of banks make almost all payments.

One of the reasons for the high vulnerability among banks is due to the large number of transactions that they carry out in their daily activities. This can be inferred by the number of transactions involving violations as part of a single investigation: 16 financial sector companies have more than 1,000 such violations, with the highest figure at 20,542 (ING Bank case in 2012). Ten financial companies have a number of violations ranging from 100 to 1,000. Another eleven have between 10 and 100. Only 17 companies have less than ten violations. The only sector that is comparable in terms of the number of violations is tourism. For example, the U.S.-Dutch company CWT B.V. committed 44,430 violations (2014 case). This is due to the fact that each voucher sold, for example, is counted as a transaction, and their number can be large. However, unlike banks, the volume of transactions itself is much smaller in this case, which means that the amount of the fines is also lower. The remaining sectors have fewer cases with a comparable number of violations. If financial and tourism sectors are excluded from the sample, only six companies have more than 1,000 violations. Twelve of them have numbers ranging from 100 to 1,000, 29 companies have between 10 and 100, and 60 of them have up to ten violations. In 45 of the 215 cases, the number of violations is not indicated.

Another feature of the financial sector is the simultaneous violation of multiple sanctions regimes (24 of 54 cases), and in some cases the number of such regimes is quite high compared with other sectors. For example, UniCreditBank in 2019 acknowledged violations of eight U.S. sanctions regimes over the course of several years. Credit Suisse AG and JPMorgan Chase violated six regimes each (in 2009 and 2011, respectively). In other words, banks and other financial companies tend to commit a large number of violations simultaneously under several programmes, which, taking into account the volume of transactions, generates a higher amount of fines.

The U.S. authorities classify violations by 18 of 54 financial companies as “egregious” (33%) and 28 as “non-egregious” (52%). No classification was given for the rest of the cases (15%) (this usually means that the violations are not “egregious”). However, the investigation documents only recorded a willful violation in two out of the 18 “egregious” cases. This sets banks apart from the rest of the sectors, where there are 30 willful violations. Almost all the other “egregious” cases involve reckless violations. This usually includes disregard for U.S. law, which is also considered a rather serious offence and may well be classified as an “egregious” violation. The low number of willful actions nevertheless shows that banks are often not pursuing selfish goals when committing violations, while in other sectors such behaviour is more common, although it is not overly prevalent. However, such violations may have aggravating circumstances that make them “egregious.”

Of the 54 financial companies, 21 of them (39%) did not have an adequate compliance service at the time of the violations, or they committed serious errors. In these cases at least, the U.S. authorities considered the state of compliance as an aggravating circumstance. In only three cases, compliance was sufficient (5%) and the violations were caused by factors beyond the service’s control, or there were isolated errors. No such estimates were given for the rest of the companies (56%). In some cases, the subsequent establishment or improvement of a compliance service is one of the conditions for concluding an agreement with the U.S. authorities to close a case. There are a number of standard operations in this regard that are used by both the financial sector and other companies. The most common ones are training courses for employees, the purchase of new software to monitor violations of sanctions, the preparation of manuals for employees, audits of transactions, the hiring of new employees, and the firing of those responsible for violations, among others. Of the 54 financial companies, 30 of them have taken at least one of these measures. There may actually be even more of them since such measures only started being recorded in the investigation documents relatively recently.

Statistics on the voluntary disclosures of violations to the U.S. authorities also provide some interesting information. Only 21 of 54 companies (39%) disclosed their violations voluntarily. The remaining 33 (61%) were “caught,” which led to higher fines. Going forward, though, almost all the companies cooperated with the authorities. Fifty of the 54 companies engaged in at least one form of such cooperation (the timely provision of all requested materials, the disclosure of all necessary information, signing a tolling agreement, etc.). Negligence or delays in interaction with the authorities were only seen in a few cases, but even in these cases there are elements of cooperation in other areas. In the four other cases for which the documents do not contain information about cooperation, it most likely took place. At the very least, they do not mention anything about a lack of cooperation. It is interesting that there are almost no “repeat offenders” among banks. With the exception of one bank, none of them had committed any violations in the five years prior to the investigation.

To illustrate the data we have presented, let’s consider a few typical cases. One of the most recent precedents is the UniCredit case, which was wrapped up in April 2019. Three of the bank’s branches – in Munich, Vienna, and Milan – were all fined simultaneously. Munich-based Unicredit Bank AG, which ultimately agreed to pay a fine of USD 553.38 million, was hit the hardest. Over the past ten years, it ranks fourth in terms of the fine amount and is among the five aforementioned banks that account for the lion’s share of all payments. According to the U.S. authorities, the bank committed 2,158 violations as part of eight sanctions regimes (against Iran, Cuba, Syria, Sudan, Burma, Libya, as well as non-proliferation and terrorism). The main issues are related to Iran. Along with the Department of the Treasury, the investigation involved other regulators, such as the Department of Justice, the Federal Reserve Board, the New York State Department of Financial Services, and the New York District Attorney's Office. Such a wide range of organizations is rather the exception than the rule (181 of 215 cases were investigated exclusively by the Department of the Treasury), but it is often seen in large-scale investigations. The complaints are related to transactions that the bank conducted from 2007 to 2011. This period of limitations is also typical, particularly in cases involving a large number of violations by major companies. Overall, according to our estimates, the average period from the time of the first violation to when an agreement is reached to end the case is more than six years. In this case, it is significantly higher. According to the U.S. authorities, UniCredit AG willfully violated the U.S. sanctions regime in a number of its operations. This follows from the bank’s internal guidelines that aimed to conceal information about unsanctioned transactions from U.S. intermediaries. In other cases, the bank simply did not monitor transactions that could have potentially been subjected to U.S. sanctions. This situation was not isolated and went on for many years, which the Department of the Treasury regards as an aggravating circumstance. Aggravating circumstances include the fact that the bank’s violations benefited the sanctioned organizations and individuals as well as the fact that the bank is a large and branched structure that is quite capable of ensuring it has adequate control mechanisms. Although UniCredit AG did not voluntarily disclose its violations (they were discovered by the U.S. authorities), the bank went on to actively cooperate with the Americans and took a number of measures to improve its transaction control system. The UniCredit AG case is an example of the “perfect storm” in which a company that violates the U.S. sanctions regime may find itself. Nevertheless, the bank managed to minimize the impact. If it had not cooperated with the investigation, it would have faced a USD 1.366 billion fine. Discounts for cooperation and other extenuating circumstances are a common practice by the U.S. Department of the Treasury. In doing so, it encourages companies to be more proactive in disclosing violations and preventing them in the future.

There are a number of other examples of the “perfect storm.” They include the textbook example of the French bank BNP Paribas, whose record fine has yet to be topped. The bank paid USD 963.619 million to the U.S. Department of the Treasury alone, and its total payments reached USD 9 billion for 3,897 violations as part of four sanctions regimes (Iran, Sudan, Cuba, and Burma). There were several circumstances working against the bank all at once: management was aware of the problems with monitoring transactions and the Americans found attempts to hide them, the violations were frequent and benefitted individuals and organizations from U.S. “blacklists,” and the bank did not voluntarily disclose them. Such circumstances are typical for “perfect storm” cases. These include investigations against Standard Chartered Bank, ING Bank, Credit Suisse AG, HSBC, Credit Agricole Corporate, and others.

Of no less interest is another type of case, when banks committed minor violations, yet managed to significantly minimize the damage by providing information to the U.S. authorities in a timely manner and having an effective compliance service. Recent examples include an investigation against the U.S. bank Western Union, which concluded in June 2019. The bank conducted 4,977 transactions with a company on the SDN list. The transactions with the company were not conducted directly, but on behalf of another agent bank in Gambia. As a result, Western Union itself did not notice the violations in time, although it should have monitored them. Once they were eventually identified, the bank voluntarily reported them to the U.S. Department of the Treasury and provided full assistance in the investigation. Interestingly, the U.S. authorities said the bank had an effective compliance service, and its oversight was considered an isolated case. As a result, the bank was fined USD 401,600, although the maximum amount could have exceeded USD 1.2 billion.

U.S. enforcement actions have been imposed on a Russian bank as well. In 2014, the Bank of Moscow agreed to pay a fine for 69 violations of the U.S. sanctions regime as part of the non-proliferation programme. Back in 2008-2009, a Russian bank conducted a series of transactions with Bank Melli Iran, which had been on the SDN list since 2007. The transactions were conducted with the mediation of U.S. banks, which gave the American authorities a reason to file claims against the Russians. The bank itself did not voluntarily report the violations, but this was due to a lack of information about them, and not because of malicious intent. At any rate, the violations were classified as “non-egregious.” The main issues with the bank were standard: lack of proper control over transactions, negligence, and the benefit that the SDN listed organization received. However, the bank actively cooperated in the investigation and took a number of measures to remedy the situation. As a result, the amount of the fine was set at USD 9.49 million, although its base amount (without discounts) was USD 14 million, and the maximum amount could have significantly exceeded both the base and final payment.

Major Russian banks try to comply with the U.S. sanctions regimes. The same goes for Chinese banks. However, there is a paradoxical situation here: Russia and the PRC are viewed by the Americans as strategic threats, but their businesses, particularly those with internationally oriented activities, carefully comply with U.S. laws. Russian and Chinese banks have been on the SDN list, but they were relatively small banks that willfully worked in sanctioned sectors. Large banks shy away from such risks. Over the next ten years, the number and amount of fines against European banks may also significantly decrease. High-profile investigations and heavy fines seemingly force both those who have already been investigated by the Americans and those who have escaped this fate to adapt to the risk of sanctions. This suggests that the U.S. sanctions are effective in this segment: they force companies to change their behaviour by avoiding interaction with sanctioned persons and companies. This means that they contribute to their further isolation.

Conclusions

The financial sector is most vulnerable to risks associated with U.S. sanctions regimes. For major banks that are active internationally, these are usually unintentional violations of U.S. sanctions against third countries. Such violations can lead to fines and, as a consequence, serious financial losses. Financial companies lead the way both in terms of the number of violations as well as the proportion of payments. This “lead” can be attributed to the specifics of the banks’ activities – a large number of operations and the difficulty of monitoring them. However, the analysis showed that in many cases the banks’ compliance services that are responsible for complying with the law were not ready to work with the U.S. requirements: they often did not notice violations, while in other situations management preferred to conceal them. More often than not, there is no malice in a bank’s violations, but, rather, deficiencies in monitoring. The most common behavioural strategy for financial companies is cooperation with the U.S. authorities, and one of the key measures is an improvement in monitoring tools. Our data does not offer an indication of the effect that fines have had on other banks. Apparently, they force them to be more careful. Banks learn from the mistakes of those that have been previously investigated, but the extent of this effect has yet to be determined. For now, it is clear that financial companies seek to avoid repeatedly violating the U.S. sanctions regimes, which is typical for companies from other sectors.

The data shows that U.S. fines are highly effective. They force companies to change their behaviour, distance themselves from those under sanctions, and contribute to the isolation of the latter. Banks play a key role here since a lack of access to financial services can damage any sector of a target country’s economy, i.e. it is universal. The “state-business” relations are fundamentally different from “state-state” relations. Business is more loyal to the requirements of the United States, both with regards to companies from U.S. allies as well as those whom the United States considers competitors or adversaries. China and Russia are among the latter. Even in a situation where relations at the political level can be strained, business tries to follow U.S. laws.

Article first published in Polis. Political Studies Journal (2020. No. 6. P. 73-90).

Timofeev I.N. “Sanctions for Sanctions Violation”: U.S. Department of Treasury Enforcement Actions against Financial Sector. – Polis. Political Studies. 2020. No. 6. P. 73-90. (In Russ.) https://doi.org/10.17976/jpps/2020.06.06

1. Figures 1 and 2 contain the author’s data.

(votes: 1, rating: 5) |

(1 vote) |

Are We in for Epidemics of Sanctions?

‘Selective’ Bipolarity? From a Coalition of War to a Coalition of SanctionsThe most important task for the diplomacy of Washington and Beijing will be the fight for major players

US Elections and Sanctions Against RussiaThree key risks for Russia