Nord Stream 2: Pros and Cons

In

Login if you are already registered

(votes: 1, rating: 5) |

(1 vote) |

When Gazprom announced that it was adding two gas pipelines to the Nord Stream project at the St. Petersburg International Economic Forum in June 2015, few people expected the company to garner so much interest in such a short time. The initiative, which has since been given the name Nord Stream 2, is now key to Gazprom’s European ambitions, following the failures of South Stream and Turkish Stream.

When Gazprom announced that it was adding two gas pipelines to the Nord Stream project at the St. Petersburg International Economic Forum in June 2015, few people expected the company to garner so much interest in such a short time. The initiative, which has since been given the name Nord Stream 2, is now key to Gazprom’s European ambitions, following the failures of South Stream and Turkish Stream.

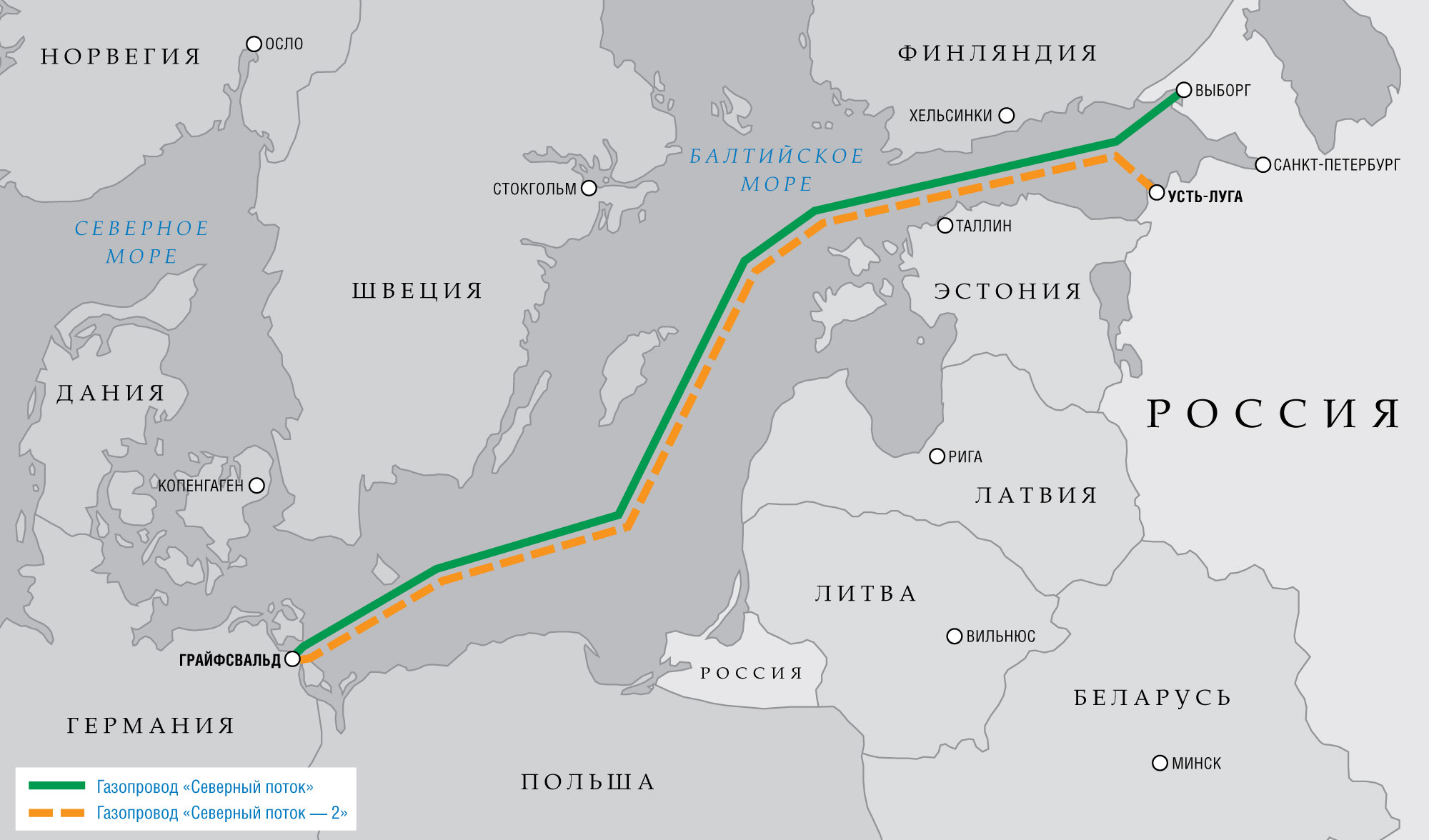

The Nord Stream 2 Shareholders Agreement was signed in September 2015, crystallizing the participants in the project: Gazprom was accorded 51 per cent of the share capital, with each of the foreign partners – E.On, Royal Dutch Shell, Wintershall/BASF and OMV – receiving 10 per cent. The French company Engie controlled 9 per cent of the shares, but Gazprom sold it 1 per cent of its own shares so that all the foreign companies had 10 per cent each. The combined capacity of the third and fourth pipelines of the trans-Baltic channel is expected to reach 55 billion cubic metres per year, the same as Nord Stream 1 (which is still not running at full capacity). Unlike the first two lines, which start at Vyborg, Nord Stream 2 is expected to originate from Ust-Luga.

All the foreign companies taking part in the Nord Stream 2 Project have a connection with Russia. E.On operates five power plants in Russia. Royal Dutch Shell owns 27.5 per cent of the share capital in the Sakhalin-2 project. OMV has been a reliable partner for decades (in 1968, it became the first Western European company to sign a contract for the supply of gas from the USSR). And Wintershall and Engie own shares in Nord Stream 1. All the companies involved in the project are interested in consolidating their positions on the Russian market, especially given the current geopolitical tension and the sanctions regime.

Nord Stream 1, 2

Although Nord Stream 2 involves companies from numerous countries, at the political level, the greatest amount of support for the project is being provided by Germany. The German federal authorities are actually in a difficult position here, as Berlin needs to avoid suspicion of non-compliance with EU energy market legislation while at the same time pursuing its own interests. By following a policy of not helping, but at the same time not opposing Nord Stream 2, the federal authorities escape the wrath of other EU member states, preferring make reference to the purely commercial nature of the energy initiative. However, there are a number of factors that would suggest Berlin is very interested in Nord Stream 2 becoming a reality:

- The official visit of German Vice-Chancellor Sigmar Gabriel to Moscow in late October 2015 revealed Berlin’s interest in the project being carried out outside the legal framework of the EU institutions. Gabriel said that the most important thing was to ensure that all decision-making remain under the competence of the German authorities, so that Berlin can limit the “opportunities for external meddling”.

- A few days before Christmas, the Federal Cartel Office of Germany passed a decision allowing European companies to take part in the share capital of the project, thus completing the legal registration of the joint venture that would build the gas pipeline.

It is worth noting that Berlin repeatedly stated that one of the requirements for the completion of the Nord Stream 2 project was to preserve Ukraine’s status as a transit country after 2019. Gazprom had been voicing its desire to stop transporting gas via Ukraine for years. However, after June 2015, against the backdrop of intensive discussions on the parameters of Nord Stream 2, the Russian company softened its position and agreed to continue supplying gas after the 2019 cut-off point.

Despite all the rhetoric about European solidarity and the need to build a common energy policy, implementing the Nord Stream 2 project is about money first and foremost. For example, high-ranking representatives in Poland who joined Central European calls to have Nord Stream 2 included on the agenda of the EU Summit that took place on December 17–18, 2015 in order to block it have said that Warsaw is prepared to take part in the project if a gas pipeline runs through Polish territory. It is precisely this loss of transit fees that would be the most painful consequence of Nord Stream 2 for Central and Eastern European countries. Ukraine, Slovakia, Poland and, to a lesser degree, Romania, the Czech Republic and Hungary could suffer substantial losses if transit through their territories were to cease. Even during the crisis in 2015, Ukraine received around $2 billion in transit fees (the 2013 figure was double this amount). And this is why the Ukrainian establishment continues to demand that the Nord Stream 2 project be banned, as it is not in the interests of Kiev.

If Nord Stream 2 comes into being, then gas will continue to be delivered via Ukraine, as Gazprom’s long-term contractual obligations require it to guarantee the stable supply of gas to Central and Eastern European countries. However, gas not intended for Central and Eastern Europe, including that which travels through the Yamal–Europe pipeline, will run through a new route, and Germany will become the largest gas hub in Europe. Gazprom, in turn, will become the leading supplier of gas to Germany, with a 60-per cent share of the market. But there are a number of obstacles in the way of Nord Stream 2 becoming a reality. The most often cited of these – that increasing gas supplies is impractical and uneconomical – are unsubstantiated and unfounded, and they present far less risk than the obstructionist position of the European Union.

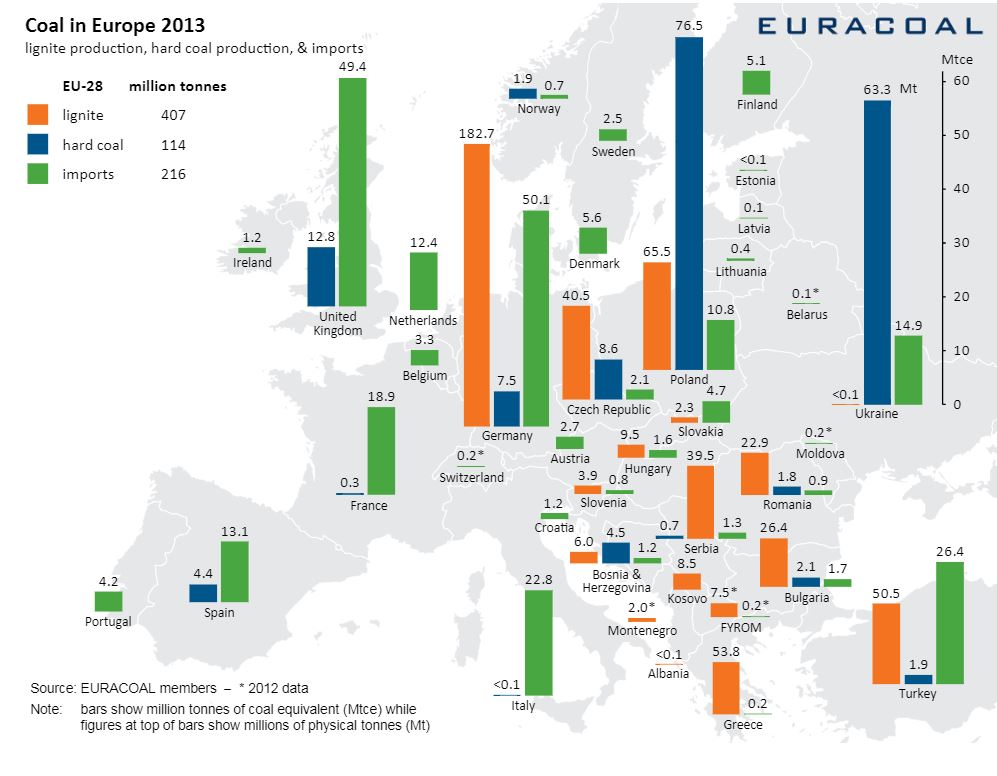

The main argument of articles that express scepticism about the feasibility of the Nord Stream 2 project is that European demand for gas will inevitably fall in the long term. The 23-per cent drop in gas consumption in 2013–2014 is used as a basis for furthering this argument. The reason for this sharp drop, however, is the revival of one of the most polluting energy sources, namely, coal. Coal became a kind of buffer for a number of countries during the financial crisis. It was thanks to its low price and availability (especially of the particularly environmentally un-friendly lignite variety) that countries such as Germany and the United Kingdom made sure that the power energy continued to turn a profit.

In terms of electricity production, Europe has developed in the opposite direction to that of the United States. The growth of shale gas production in the United States has contributed to the overall decline of coal use for energy purposes, with the excess cheap coal being exported to Europe. However, the signing of the Paris Agreement on December 12, 2015, which aims to prevent the average global temperature from increasing by more than 2°C above pre-industrial levels, means that the prospects for the coal industry in Europe are looking very gloomy indeed. The governments of several Western European countries are seeking either a complete ban on the use of coal (the Netherlands, for example), or to reduce its use to a minimum (1 per cent in the case of the United Kingdom). In addition to government measures, the European coal industry is under threat from the rising costs of resources. According to the International Energy Agency (IEA), by 2025, one tonne of coal could cost $30. This figure could be as high as $50 by 2040.

In light of all this, there is likely to be a pronounced increase in gas consumption in Western Europe in the next few years. According to IEA forecasts, demand for gas in Europe will not drop until at least 2040, and will demonstrate a growth of 0.8 per cent throughout this period (to 610 billion cubic metres of gas by 2040). The viability of Nord Stream 2 is supported by the slowdown in gas production rates in Western Europe.

The Netherlands reached its gas production peak in 2007–2008, and given the rapidly falling production rates at its largest oilfield in Slochteren, the country is likely to be a net importer of “blue-sky fuel” within 15 years. Since 2005, the United Kingdom has been consuming more natural gas than it can produce. In parallel with its own falling production rates, London will gradually phase out the country’s coal-fired power plants, which pollute the environment greatly. This will add greater incentive to import gas. By 2020, the United Kingdom is expected to import 70–75 per cent of its gas. France has still not managed to work out a consistent line with regard to replacing the power stations that are to be decommissioned by 2025 because of its commitment to increasing the share of nuclear energy its energy mix to 50 per cent. As such, the country could also benefit from an additional source of energy.

Paradoxically, Germany, the country that is most interested in seeing Nord Stream 2 come into being, faces the most obstacles to increasing the share of gas in its energy mix. 2015 figures show that 44 per cent of the country’s electricity was produced at coal-fired power plants. And after government initiative to introduce fees for using old power stations was nixed under heavy pressure from the coal lobby, it would seem that the situation is unlikely to change in the near future, especially given the fact that parliamentary elections have been set for 2017.

On the whole, despite the ups and downs of individual countries, the state of affairs on the Western European gas market are conducive to the construction of a new gas pipeline. But it is not the state of affairs that will decide the fate of Nord Stream 2, as the actions of the European Commission suggest that the project will inevitably be met with administrative resistance from Brussels. President of the European Council Donald Tusk has already stated that Nord Stream 2 does not meet EU standards, as it does not strengthen energy security in the Union. The lack of proper regulation with regard to marine gas pipelines means that no one can stop Gazprom from building Nord Stream 2. The rest, it would seem, will depend on the extent to which the German regulatory authorities are able to keep the Nord Stream 2 issue under its authority.

Gazprom could also face problems from within, as the Power of Siberia pipeline, which is estimated at $55 billion, could tie up the Russian company’s financial and production capabilities. Given the fact that Gazprom is locked in negotiations on the possible use of third-party gas in the Power of Siberia project, there is nothing to suggest that the company can guarantee an additional 55 billion cubic metres per year.

At present, Russia transports around 56 billion cubic metres of gas via Ukraine. If it is built, Nord Stream 2 will not solve all the problems associated with conducting business with Ukraine – especially as the pipeline will probably not run at full capacity (which is the case with the first Nord Stream pipelines) – but it will minimize them significantly. And this is precisely what Gazprom needs, given its financial balance has been hovering in the red for some time now.

The only serious obstacle to the project is the fact that the EU structures represent the interests of almost the entire continent. At least seven European Union countries – Poland, Romania, Slovakia, Hungary, Latvia, Lithuania and Estonia – have, out of fear of losing transit fees or out of blatant Russophobia, protested the Nord Stream 2 project. On the basis of the petition signed by seven countries, and with the interests of the Poseidon gas pipeline that will connect Italy and Greece in mind, the European authorities announced the intention to strengthen control over the energy sector through access to commercial contracts and pricing details.

The rational interests of the European Union with regard to Russia boil down to achieving the best possible negotiating position against the background of falling production from other sources that traditionally supply gas to Europe. The European Union could act irrationally and prioritize purchases of more expensive natural gas (as is the case with Lithuania, with plans to purchase LNG from the United States) although this is an unlikely scenario given the slow economic growth on the continent.

People often make the mistake of thinking that the interests of Russia and the interests of Gazprom are the same. In this case, however, they are largely the same. The Russian government does not care who produces and supplies the gas – Gazprom or Novatek, which also seeks to export gas to Europe. All it cares about is whether these activities generate revenue. The intertwining of the government apparatus and Gazprom does not promote competition on the domestic market in Russia. The gas sector needs to be liberalized, even if only partially, if Russian gas companies want to increase their competitiveness. But even if the Russian gas market is liberalized, the European structures are unlikely to change their attitude towards Russian gas supplies. Accordingly, Nord Stream 2 is necessary because it would minimize the risks associated with transit supplies through unstable states while at the same time retaining Russia’s market share.

(votes: 1, rating: 5) |

(1 vote) |