China’s Energy Crisis

In

Login if you are already registered

(votes: 1, rating: 5) |

(1 vote) |

Researcher, Junior Research Fellow at the Lomonosov Moscow State University, Senior Lecturer at Asian and African Studies from Moscow State University

In September–October 2021, more than 20 of China’s provinces, autonomous regions and direct-administered municipalities (hereinafter provinces) had to face power failures. In most regions, they affected industrial enterprises and commercial organizations. Restrictions were imposed on the use of air conditioning and outdoor lighting. In Liaoning, Jilin and Heilongjiang—China’s north-eastern provinces—blackouts began without warning, something that affected even publicly significant facilities. As a matter of fact, traffic lights stopped working while the system of water supply malfunctioned, which is previously unheard of in China, where the energy sector is intended to protect the population and socially significant enterprises from possible technological and economic shocks as much as possible.

Given China’s involvement in global value chains, the impact of the energy crisis reverberated at enterprises both in China and abroad in a wide range of sectors. Goldman Sachs estimates suggest that power failures have affected about 44 per cent of the industrial enterprises in China alone. The blackouts and resulting delays in supply chains largely drove the September 2021 spike in producer price index by 10.7 per cent year-on-year. This was the highest that the indicator had been since 1996.

It is no coincidence that the media keeps mentioning that China has not had any such blackouts for around ten years. Indeed, with the old model’s resources exhausted, China has embraced structural economic and industrial reforms, while its GDP growth started to slow down. For the last few years, the world’s largest energy system in terms of installed capacity and power generation has had excessive capacities. The Chinese energy sector has, therefore, come out of the most difficult stage of the pandemic in a state that would have been unprecedented for the late 2010s.

At the same time, the autumn crisis of 2021 cannot be said to have arrived as a complete surprise, as China also experienced power supply problems in late 2020.

A comparative analysis of the factors that informed the crises in 2011 and 2021 reveals a number of similarities. On the one hand, such parallels indicate that these phenomena may be cyclical, occurring due to economic developments and fluctuations in prices of energy sources. On the other hand, they testify to China’s failure to resolve the major contradictions in the sector in spite of the many reforms. China still lacks flexibility in diversifying its structure of power generation to mitigate the threats to its energy security—the same is true for its pricing mechanisms amid a market transition that is still incomplete as well as for the country’s approaches to managing and implementing the directives issued by the central authorities.

In September–October 2021, more than 20 of China’s provinces, autonomous regions and direct-administered municipalities (hereinafter provinces) had to face power failures. In most regions, they affected industrial enterprises and commercial organizations. Restrictions were imposed on the use of air conditioning and outdoor lighting. In Liaoning, Jilin and Heilongjiang—China’s north-eastern provinces—blackouts began without warning, something that affected even publicly significant facilities. As a matter of fact, traffic lights stopped working while the system of water supply malfunctioned, which is previously unheard of in China, where the energy sector is intended to protect the population and socially significant enterprises from possible technological and economic shocks as much as possible.

Given China’s involvement in global value chains, the impact of the energy crisis reverberated at enterprises both in China and abroad in a wide range of sectors (from automaking and smartphone manufacturing to cardboard packaging). Goldman Sachs estimates suggest that power failures have affected about 44 per cent of the industrial enterprises in China alone. The blackouts and resulting delays in supply chains largely drove the September 2021 spike in producer price index by 10.7 per cent year-on-year. This was the highest that the indicator had been since 1996.

It is no coincidence that the media keeps mentioning that China has not had any such blackouts for around ten years. Indeed, with the old model’s resources exhausted, China has embraced structural economic and industrial reforms, while its GDP growth started to slow down. As a result, power consumption fell too, and power generating equipment started working shorter hours. For the last few years, the world’s largest energy system in terms of installed capacity and power generation has had excessive capacities. The Chinese energy sector has, therefore, come out of the most difficult stage of the pandemic in a state that would have been unprecedented for the late 2010s.

At the same time, the autumn crisis of 2021 cannot be said to have arrived as a complete surprise, as China also experienced power supply problems in late 2020. Besides, in the summer of 2021, some of China’s provinces experienced power shutdowns, having to redistribute their grid load.

A comparative analysis of the factors that informed the crises in 2011 and 2021 reveals a number of similarities. On the one hand, such parallels indicate that these phenomena may be cyclical, occurring due to economic developments and fluctuations in prices of energy sources. On the other hand, they testify to China’s failure to resolve the major contradictions in the sector in spite of the many reforms. China still lacks flexibility in diversifying its structure of power generation to mitigate the threats to its energy security—the same is true for its pricing mechanisms amid a market transition that is still incomplete as well as for the country’s approaches to managing and implementing the directives issued by the central authorities.

The Principal Causes of the Crisis

In the last decade, China has undoubtedly implemented structural reforms in its energy sector. However, they have not radically changed the balance of forces so far as we can tell. The share of thermal power plants (TPPs) in the country’s power generation dropped in 2021, as compared to January–September 2011, from 82.6 per cent to 71.2 per cent, with over 90 per cent of them using coal. Clearly, this sector is still critically dependent on coal supplies.

Given the large share of coal TPPs in China’s power generation, coal shortages—whether physical shortages, price hikes or undeveloped logistics channels meant to ensure timely supplies from domestic and international sources—have repeatedly resulted in power failures in the past.

Over the nine months of 2021, coal production in China was increasing at a rate (3.7 per cent in year-on-year) slower than the energy generation at the nation’s TPPs as well as the consumption of such energy (11.9 per cent and 12.9 per cent respectively) [1]. This came to be the case for a number of reasons:

- As part of the nation’s environmental policy and the overproduction struggle waged by the central authorities in 2016–2020, coal mines with a total capacity of 1 billion tons a year were shut down.

- In 2021, in an effort to improve labour safety following a series of emergencies, enterprises with the capacity of 20 million tons were shut down, and that was in the Henan province alone.

- A relatively weak dynamics stemmed, among other things, from the numerous inspections of mining enterprises for compliance with environmental and labour safety standards.

- Torrential rains in the Shensi province, one of China’s principal coal mining hubs, forced shutdowns at 60 mines at the height of the energy crisis in October. It was not until mid-December when the operations resumed.

- The anti-corruption campaign in the Inner Mongolia Autonomous Region (IMAR), China’s another important coal-mining centre, is another factor, while legislative changes had their effect as well. Amendments to China’s Criminal Code came into force on March 1, 2021. For the first time ever, the Code imposed criminal liability for potentially dangerous illegal actions even if they do not result in major accidents with a large number of victims or in other grave consequences. Besides, China’s coal businesses do not have the right to mine coal in excess of their licensed capacity. It has become all too risky to mine coal above that figure, which companies could easily do before. As a result, the drop in production was estimated at 90 million tonnes as compared to the previous winter.

Since the mid-2000s, coal prices have been determined by market mechanisms. Both crises (in 2011 and in 2021) occurred amid growing coal prices. Typically, September is not the time for surged coal consumption and coal prices—yet, in 2021, coal futures and spot prices increased severalfold in China, with coal prices generally growing on the global market and amid high demand and falling supplies. Back in June 2021, energy coal futures were traded at approximately CNY 800 per ton; on October 19, the price reached a record high of CNY 1982 per ton. Coal mining companies are believed to have the capacity to fully cover their costs and make profits at prices of CNY 450–650 per ton, while this figure is even lower in the IMAR. The authorities believe prices within the range of CNY 500–570 per ton to be adequate for long-term contracts. They tend to assume that prices in this range will generate sufficient profits for mining companies without TPPs having to pay too much for fuel. Additionally, at this price level, Chinese-mined coal can compete with foreign supplies.

Approaches to determining electric power tariffs for coal-fired TPPs have changed over the past decade. In 2011, coal-fired TPPs sold electricity at fixed rates. From January 1, 2020 until October 14, 2021, a system of market energy sales operated in China, where 70 per cent of the country’s coal-fired TPPs participated. The final rate was determined through the “base rate + fluctuations within the 10–15 per cent range” formula. The rate at which TPPs provided electricity to power grids in late 2019 under a preliminary agreement was set as the base rate. To ensure a smooth transition to the new pricing system, average rates for industrial and commercial consumers could decrease but not increase.

Thus, a full-fledged electric energy market has failed to emerge in the past decade. The rates did not reflect the real costs borne by generating companies either before the 2011 crisis, or in 2021, which is an important feature of the industry. It is no accident that the energy sector is called a “shock absorber” that ensures the relatively sound development of the Chinese economy. When fuel prices fluctuate wildly, state-owned generating companies always suffer financial losses—that is, the more energy they produce, the greater their losses are. Reports of China’s leading generating companies suggest that only Huaneng (华能) showed profit in 2011 out of the “big five” generating companies. In January–August 2021, coal-burning generation and heating companies suffered a 15.3-per cent drop in profits, while the profits of coal-producing grew by 145.3 per cent.

As in 2011, unsatisfactory financial results of coal-fired TPPs were recorded even before the crisis peaked, and the much-needed pricing reforms had to be postponed. Both times, generating companies pointedly refused to sustain losses (for instance, they did not purchase coal at peak prices and spent their reserves until they ran out, or, alternatively, shut down for maintenance).

Curiously, one conclusion China drew from the previous crises was that power generating companies that happen to own coal mines demonstrate greater stability amid price fluctuations. Economists are yet to assess whether this strategy was justified—for instance, for the State Energy Investment Corporation (国家能源投资集团) established in 2017 through the merger of Godian (国电), a generating company, with Shenhua (神华), China’s largest coal-mining company.

The crises in 2011 and 2021 had to do with with climate as much as with the issues in the coal industry. China tends to consume ever more power, as air conditioners are widely used during the hot summer months, while electric heaters are used in the cold winter months, particularly in the south of the country where no central heating is available. For instance, back in August 2020, the State Grid Corporation of China (SGC of China) reported record jumps in load in 11 provincial grids and across one regional grid. A new record was set in January 2021 amid low temperatures, followed by another record in July. Grid load typically drops in September; however, this year was an exception, as China experienced its hottest September since 1961.

Heat was the factor behind the shortages in both 2011 and 2021, and not only because it drove power consumption for air conditioning. In both cases, heat also resulted in lower water levels and, as a consequence, reduced HPP generation, which increased the load of the TPPs.

In the realities of China’s energy sector as it stands today, nature has also affected the generation of renewable energy sources (RES). For example, reports surfaced on September 21, 2021 claiming that power generation at wind power plants (WPPs) in China’s northeast dropped sharply. Out of almost 35 GW of the installed RES capacity, less than 10 per cent generated at least one kW/h. A similar situation occurred in the region in the summer of 2021.

The problem is not so much that power generation at RES power plants is unstable and has sharply dropped. Unlike TPPs and NPPs, they are not considered as sources for providing the system’s base load. Problems only emerge when the system has no generation reserves and storage systems capable of offsetting these fluctuations or has no options to supply energy from other regions or abroad. The Liaoning province is a case in point. Starting in 2016, the Heilongjiang, Jilin and Liaoning provinces in China’s northeast have consistently been shutting down their low-efficiency coal-mining enterprises so that the local TPPs have largely come to depend on coal shipments from the IMAR. Besides, north-eastern grids actively put WPPs into operation. In the autumn of 2021, high coal prices (as well as coal shortages) driven by the specifics of energy rates resulted in only about a half of the installed capacities of its coal-fired TPP actually functioning during the Liaoning blackouts. As a result, current frequency in the grid dropped below 49.8 Hz, with a simultaneous drop in WPP generation. Energy sector enterprises were forced to cut the power supply, including for the population, since the drop in the currency frequency below 49.9 Hz posits a safety threat for energy supply. In particular, it can cause serious damage to all sorts of power-generating equipment.

Does Coal Have a Future?

Finally, the actions on the part of the local authorities have played an important role in the crisis breaking out in some regions. For instance, they introduced harsh administrative measures to achieve target indicators drawing on the “double control” policy of energy consumption and the GDP’s energy intensity (双控制度).

In August and September 2021, the National Development and Reform Commission (NDRC) released documents listing all the provinces that risked failing in the tasks set under the “double control” policy by the end of the year. The NDRC also demanded that control be tightened over enterprises in energy-intensive sectors and enterprises with high greenhouse emissions, and that their financing be reduced. Success in implementing the “double control” policy is one of the criteria for assessing the work of local officials. As a result, several provinces, including Jiangsu and Guangdong, started cutting off energy supplies to enterprises. In individual provinces, it was recommended that enterprises operate at specifically indicated hours only.

The “double control” policy was first proposed in 2006 as part of the 11th Five-Year Plan. Its implementation had already resulted in power shutdowns, although parallels can be found – not with the events of 2011, but with the 2010 shutdowns. For instance, in September 2010 (a few months before the conclusion of the 11th Five-Year Plan), local authorities in several provinces, including Zhejiang and Jiangsu, started cutting the power supply to industrial enterprises in order to reduce the GDP’s energy intensity by 20 per cent and comply with the target indicators set forth in the Five-Year Plan.

Another example of how the administrative leverage of the local authorities can affect the development of the energy sector is the slow progress of inter-provincial energy trade. In a country where the largest generation facilities are far removed from the principal consumers, investment in the development of the power grid has significantly increased over the last decade. More liberal power deliveries could improve energy security. Nevertheless, the share of inter-regional power exchanges over the first nine months of 2021 amounted to 8.5 per cent of the power generated in China, while the share of inter-provincial power exchanges was 20 per cent. This situation stemmed from measures to protect companies doing business in a given province (and, accordingly, to maintain the income level of local budgets).

Therefore, a whole group of factors may be identified as causes of the crisis, and the impact of each varied by province. While contemporaneous, they were not always interconnected. Additionally, many were similar in nature to the factors that resulted in power failures in the early 2010s. That is, over these years, China continued to exist amid a virtually complete set of conditions for a large-scale energy crisis.

Evidently, the only reason the country escaped a crisis earlier on was because several other conditions were not met. First, there were no major spikes in coal prices prior to the pandemic, which allowed generation companies to operate normally. Second, in the era of a “new normalcy,” the spike in industrial power consumption and high export rates required for a large-scale crisis were absent. When China’s economy began to rebound after the coronavirus outbreak, these conditions were finally met.

Dynamics of Energy Consumption Growth in China’s Secondary Sector in January–September 2011–2021

Compiled by the author using data from stats.gov.cn, customs.gov.cn, cec.org.cn

Given that the tertiary sector has been seriously hit by the pandemic-related restrictions, economic growth was largely achieved in the secondary sector. As a result, energy consumption in the secondary sector in January–September 2021 grew by 12.3 per cent year-on-year, including by 9.5 per cent in the four largest energy-intensive sectors (construction materials manufacturing, ferrous and non-ferrous metallurgy, and the chemical industry). Meanwhile, exports grew by 28,1 per cent year-on-year in September 2021. On the whole, export grew by 22.7 per cent in first nine months of 2021 back to the 2011 levels.

Anti-Crisis Measures

To get the situation under control, the Chinese authorities took steps to increase coal production, simultaneously reducing coal prices while increasing electricity rates, which generally repeats the anti-crisis measures of ten years ago.

In particular, permission was given to resume production at the mines that had been shut down. Additionally, production was increased at the mines in operation. Coal mines in China are built to produce about 3–6 million tonnes a year, and the allowed capacity is set at 1 million tons, so that production can, if necessary, be made to fit economic needs The allowed production limit on coal have increased. In particular, plans for the fourth quarter include ramping up production by 55 million tons, which will make it possible to stabilize prices and balance out supply and demand. The permitted annual production volume will thus total 220 million tons, which is 5.7 per cent higher than in 2020. Additionally, the customs service received coal deliveries from Australia that had arrived in Chinese ports before the restrictions were imposed.

At a meeting with representatives of mining companies, the authorities clearly signalled that coal prices needed to go down. One option being considered is to work out a new coal pricing mechanism based on the “base price + fluctuations” formula (with account for the expenses and reasonable profits of mining companies amid market changes). Plans involve linking pricing mechanisms for coal and electricity.

Additionally, the NDRC has adjusted electricity rates. Starting October 15, all coal-fired TPPs were mandated to sell electricity on the market. The fluctuation corridor was increased to +/–20% of the base rate. Industrial and commercial consumers will also have to purchase electricity on the market. At the same time, preferential rates for this category of consumers have been abolished. These fluctuation limits will not extend to energy-intensive enterprises whose energy consumption is covered by the “double control” policy, nor will they apply to the spot market. Grid companies will act as intermediaries for those who are unable to participate in the trading. Thus, power plants will be able to offset some of their generation costs at the consumers’ expense. These changes, however, do not extend to consumers in the agricultural sector, who will continue to receive electricity at reduced fixed rates.

In addition, coal-burning enterprises and heating facilities were given tax benefits in the fourth quarter of this year. Additionally, China promptly reached agreements with its Russian partners on increasing electricity deliveries to China.

Finally, as in 2010, the government was critical of local authorities expending excessive efforts on reducing the GDP’s energy intensity. Li Keqiang pointed out that “it is not a sports competition to reduce emissions.” At the same time, China is not planning to abandon its previous commitments to reduce emissions and energy consumption per GDP unit. Work on shutting down inefficient coal-fired TPPs will continue in order to reduce the average amount of coal needed to produce one KWh from 305.5 grams of reference fuel in 2020 to 300 by 2025.

Prospects for the Energy Sector

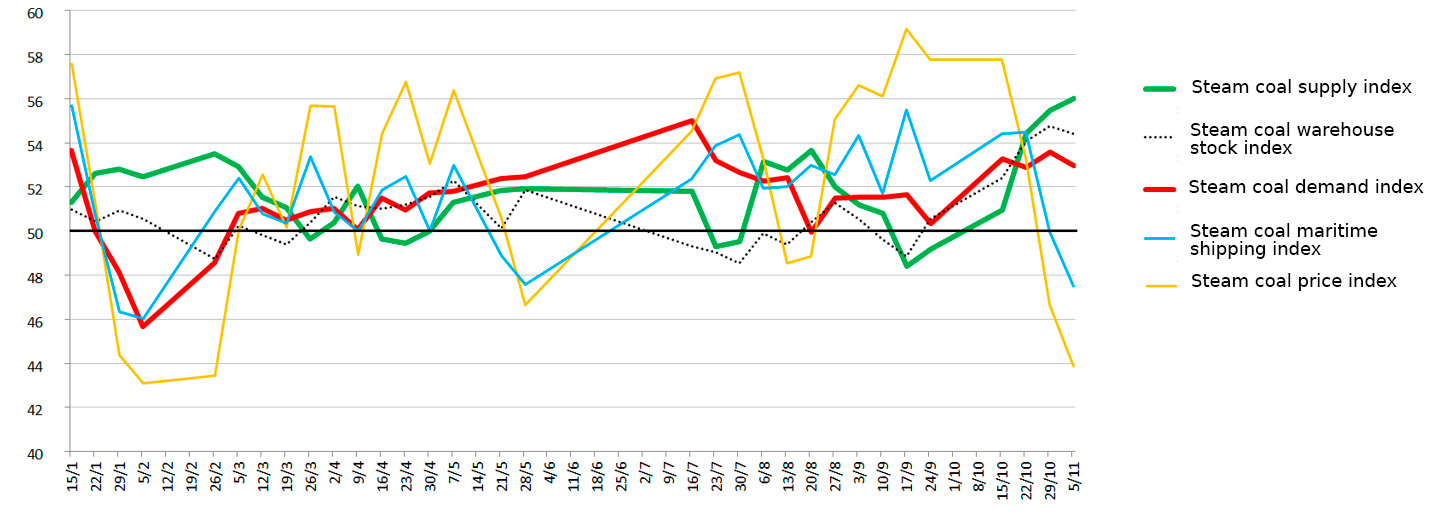

The intervention of the authorities helped stabilize the situation and contain a further growth of steam coal prices which, in turn, allowed coal-fired TPPs to replenish their fuel supplies at lower prices.

Purchasing Managers Index (PMI) sub-indices for steam coal

Compiled by the author using data from cec.org.

Regions have started to transition to new electricity rates. For instance, at October trading, the average price of electricity in the Jiangsu province was CNY 468.97 per MW/h, which is 19.97 per cent higher than the base rate for coal-fired TPPs (CBY 391 per MW/h).

At the same time, even though coal prices have fallen, they remain relatively high. Thus, a 20-per cent hike in rates is not sufficient to make up for the losses sustained by coal-fired TPPs.

The situation will also be affected by the climate factor by the end of the year. According to meteorologists, winter in China has been setting in earlier over the past decade. As a result, eight provinces and regions in the northeast and northwest of China had to turn on central heating two weeks earlier than usual this year. Additionally, HPP generation will remain low until the end of winter.

However, it is unlikely the 2021 crisis will have a major impact on energy supply in the long term. China has no shortage of generating capacities. Despite the increase in the number of operating hours, coal-fired TPPs function at almost 20 per cent below their maximum load. There are no grounds to believe that China will continue to have a double-digit GDP growth once the post-pandemic rebound is over. As other countries recover from the pandemic, the dynamics of China’s exports are likely to slow down. Additionally, the Chinese economy is undergoing a structural transformation that entails a drop in the share of the secondary sector in the GDP. In the long term, this process will naturally be conducive to decreasing the GDP’s power intensity.

Risks most likely stem from the fact that China’s energy sector is developing towards increasing fluctuations in the production and consumption of power. For instance, in the first nine months of 2021, households accounted for 14.7% per cent of energy consumption in China, which is below the world average (26.6 per cent in 2019). And this will only grow as the average income of the population increases, which, in turn, will increase the energy system load in peak hours.

Additionally, China is developing transportation using new types of fuel, primarily electricity. China is the world’s leader in electric car sales. As of year-end 2019, domestic electric car sales in China accounted for less than 5 per cent of all cars sold in the country. This figure increased to 11.6 per cent over the nine months of 2021, and plans involve bringing it to 25 per cent by 2025. Electric buses and electric cars are actively introduced as means of public transportation and in taxi services. The development of smart energy infrastructure required to charge electric cars has been put on the list of “new infrastructure” (新基建) sectors currently given development priorities.

Finally, China will continue to develop RES as part of its effort to achieve carbon neutrality. RES are characterized by interruptible generation, which will require far more flexibility in the energy system than had been envisioned when the system was being developed to provide power to major state-owned industrial enterprises as its principal consumers.

Solving this problem will require both technological and institutional changes. Technologically, generation will require greater diversification, including not only RES, but also power plants providing the baseload. With that goal in mind, for instance, the local authorities in Zhejiang are planning to increase the installed capacity of gas-fired power plants. Increasing the capacity of NPPs to 70 GW by 2025 will also help handle the problem. The importance of energy storage systems and carbon capture and storage are also becoming increasingly important. A significant role will be assigned to energy conservation and to using electricity rates to regulate energy demand.

From the point of view of institutional transformation, it would be wise to remove local administrative barriers for power interchanges and to switch the energy sector to a flexible market pricing system in order to improve the adaptability of energy systems to fluctuations in supply and demand. Transitioning to a market pricing system is the most difficult aspect of sectoral reforms, since the energy sector is among the last to have launched market transformations. It is no accident that the NDRC’s directive on improving the rate-setting system for coal-fired TPPs refers to improving “largely market-driven” energy pricing (完善主要由市场决定电价的机制). The 2021 crisis certainly accelerated important sectoral reforms, but China is still not developing a full-fledged energy market. Rather, it is liberalizing the sector very carefully. This approach, however, only makes it possible to mitigate the current contradictions, not to develop a long-term solution, and that makes similar crises possible in future.

1. Western media greatly overblow the significance that the unofficial prohibition on importing coal from Australia has had for the problems of China’s energy sector. The share of imports in China’s coal consumption is not great, and it is important mostly for coastal provinces where it is cheaper to receive coal shipped by sea from abroad than to have Chinese-produced coal shipped by rail across the entire country. When China refused to purchase Australian coal in 2021, it fairly quickly increased deliveries from Indonesia, Russia and other countries. The problem is rather that in an emergency, China has less room for manoeuvre.

(votes: 1, rating: 5) |

(1 vote) |

The History of Coal as a Fuel and its Prospects in the 21st Century

Both… But Can We Do Without the Emotions, Please. Towards a Discussion on Renewable Energy Sources and the Nuclear Energy SectorCombining renewable energy sources and other low-carbon types of energy such as nuclear power and natural gas does not at all contradict the ideology and essence of “Energy 4.0”

A Renaissance of Fossil Fuels: Consequences of Europe’s Energy Market PanicHoping that winter 2021–2022 will come to be mild

High Hopes for Low Temperatures: COP-26 Results in Consensus but Disagreements RemainToday, the world can only effect the green transition by a gradual replacement of technologies