The Asia-Pacific Region Arms Market

MH-60R Seahawk helicopters

In

Login if you are already registered

Centre for Analysis of Strategies and Technologies

The Asia-Pacific region (APR) combines the most dynamically developing countries in the world, and this applies to both economic growth and development of the armed forces. Virtually all countries in the region have been increasing their military spending in recent years, and this trend continued even during the peak of the global economic crisis. This makes APR countries an attractive market for arms suppliers. The continued growth in military spending and volume of arms imports into the region poses the question: does the development and technical re-equipment of the armed forces of APR countries strengthen stability in the region or is it a threat to its security?

The Asia-Pacific region (APR) combines the most dynamically developing countries in the world, and this applies to both economic growth and development of the armed forces. Virtually all countries in the region have been increasing their military spending in recent years, and this trend continued even during the peak of the global economic crisis. This makes APR countries an attractive market for arms suppliers. The continued growth in military spending and volume of arms imports into the region poses the question: does the development and technical re-equipment of the armed forces of APR countries strengthen stability in the region or is it a threat to its security?

ATP is a major global producer and one of the largest importers of weapons

On the one hand, APR may be called the world’s weapons blacksmith’s shop – two-thirds of world weapons production are concentrated here. Outside this region, there is only one region with a highly developed arms industry of its own – Western and Central Europe.

On the other hand, most of this production is concentrated in just three countries - the USA, Russia and China, other nations are compelled to import weapons. Therefore, the region is among the largest arms market, along with Western and Central Europe, the Middle East and South Asia. APR countries account for about one-third of world imports of arms, and half of the world’s 10 largest arms-importing countries are located here. The volume of arms supplies to the region between 2007 and 2011 increased by 21.5% in comparison with the period between 2002 and 2006 – from 62.2 to 75.6 billion dollars at 2011 prices (see Table. 1).

Table 1.APR countries in world imports of arms

| Country | Position by volume of imports among APR countries | Position in the world | Volume of arms imports between 2007 and 2011, at 2011 prices, million USD | Share in world arms imports between 2007 and 2011 |

|---|---|---|---|---|

| South Korea | 1 | 2 | 12200 | 5.53 |

| China | 2 | 4 | 10879 | 4.93 |

| Singapore | 3 | 5 | 8817 | 3.99 |

| Australia | 4 | 6 | 8270 | 3.75 |

| USA | 5 | 8 | 7694 | 3.49 |

| Malaysia | 6 | 13 | 5335 | 2.42 |

| Chile | 7 | 18 | 3863 | 1.75 |

| Japan | 8 | 20 | 3739 | 1.69 |

| Indonesia | 9 | 27 | 2931 | 1.33 |

| Canada | 10 | 28 | 2823 | 1.28 |

| Vietnam | 11 | 30 | 2382 | 1.08 |

| Colombia | 12 | 34 | 1746 | 0.79 |

| Thailand | 13 | 42 | 858 | 0.39 |

| Taiwan | 14 | 53 | 686 | 0.31 |

| Ecuador | 15 | 55 | 609 | 0.27 |

| Rest of APR countries | 2805 | 1.27 | ||

| APR as a whole | 75637 | 34.27 |

Source: SIPRI Arms Transfers Database.

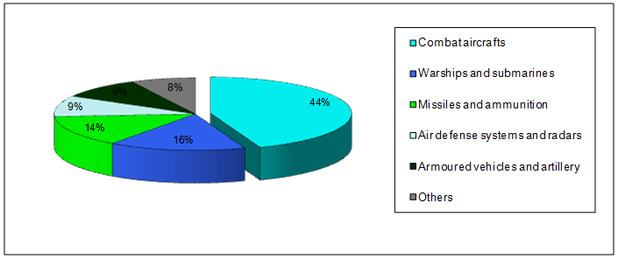

The arms supply structure in APR countries (see Fig. 1) is broadly consistent with the global structure, where combat aircrafts are in the dominant role – 45% of the volume of shipments. However, there are some differences: in arms imports by APR countries, the proportion of supply of armoured vehicles is significantly lower – 9%, at a global average of 15%. This is largely due to the fact that the leading arms importers among APR countries have their own program of production of armoured vehicles. China, Japan, and South Korea produce their own tanks, Taiwan and Singapore also produce their own armoured vehicles and artillery. Besides, the arms supply structure in APR countries has a higher percentage of naval equipment (warship and submarines) – 16%, at a global average of 13%.

Fig. 1. Arms supply structure in APR countries by types of equipment

Source: SIPRI Arms Transfers Database.

Which countries in APR are importing weapons and why

According to the degree of involvement in arms trade, APR countries can be divided into several groups.

First group – major industrial powers, possessing the most powerful military-industrial complexes, capable of producing almost all types of weapons in significant quantities. Above all is the United States, the largest military power in the world and the main exporter of weapons, and Russia. These two countries account for 54% of total world arms exports (see Tables 2 and 3). This category may also include China. China is still dependent on imports of weapons, especially of high-tech designs, but provides its own armed forces with most types of military equipment, and it is itself a large exporter. Pakistan is the main buyer of Chinese weapons. This country and China are jointly developing the JF-17 Thunder/FC-1 fighter jet aircraft. In addition, China supplies missiles and guided bombs to Pakistan, and provides technical assistance in the construction of warships. Pakistan is for now the only major military power that chose Chinese-made weapons, which retains the label of low-grade weapons for the poor. However, the list of importers of Chinese weapons is constantly expanding. It includes the countries of Asia, Africa and Latin America. There is no reason to doubt that in this decade, China will transform from a country, mainly importing weapons into a net exporter.

Table 2.APR countries in world exports of arms

| Country | Position by volume of imports among APR countries | Position in the world | Volume of arms imports between 2007 and 2011, at 2011 prices, million USD | Share in world arms imports between 2007 and 2011 |

|---|---|---|---|---|

| USA | 1 | 1 | 67309 | 30.49 |

| Russia | 2 | 2 | 52489 | 23.78 |

| China | 3 | 6 | 8146 | 3.69 |

| Canada | 4 | 14 | 2196 | 0.99 |

| South Korea | 5 | 15 | 1345 | 0.61 |

| Australia | 6 | 22 | 499 | 0.23 |

| Chile | 7 | 32 | 172 | 0.08 |

| Singapore | 8 | 39 | 108 | 0.05 |

| Japan | 9 | 45 | 69 | 0.03 |

| Indonesia | 10 | 55 | 7 | 0 |

| APR as a whole | 132340 | 59.95 |

Source: SIPRI Arms Transfers Database.

Table 3.Main arms suppliers to APR countries between 2007 and 2011

| Exporter | Volume of arms exports to APR countries between 2007 and 2011, at 2011 prices, million USD | Share in the APR market | Main buyers of arms among APR countries |

|---|---|---|---|

| USA | 27443 | 36 | South Korea, Australia, Canada, Singapore, Taiwan |

| Russia | 14054 | 19 | China, Vietnam, Indonesia, Malaysia |

| France | 8521 | 11 | Singapore, China, Australia |

| Germany | 6978 | 9 | South Korea, Malaysia, Chile, USA |

| UK | 3359 | 4 | USA |

| Netherlands | 2468 | 3 | Indonesia, Chile |

| Switzerland | 1462 | 2 | USA, China |

| Spain | 1460 | 2 | Malaysia, USA |

| Canada | 1450 | 2 | USA |

| Italy | 1388 | 2 | USA, Chile, Malaysia |

| Israel | 1287 | 2 | Singapore, Colombia |

| Others | 5767 | 8 | |

| Total | 75637 | 100 |

Source: SIPRI Arms Transfers Database.

Second group of countries – developed countries that have modern armed forces, but do not have the military industry, capable of maintaining them. This category includes Japan, Australia, Canada, New Zealand, Taiwan and South Korea. Imports of weapons to these countries are subject to the logic of a cyclic renewal of a fleet of combat equipment. These countries regularly place orders for large series of military equipment. In recent years, Australia (6th place in the world in terms of imports between 2007 and 2011) made it in the list of major importers of arms. Does this mean that the country is preparing for a major war, or that militarist forces have come to power? No, it is just means that the time has come to replace older models of weapons with new ones and, therefore, Australia has signed several contracts for the supply of modern equipment, especially aircrafts. For example, Australia bought from the USA 24 fighter aircrafts (F/A-18E Super Hornet) and a large set of arms worth $4.8 billion, transport aircrafts C-17A Globemaster-3 and anti-submarine helicopters MH-60R Seahawk. After executing these contracts, Australia will become one of the largest importers of weapons.

South Korea and Taiwan occupy a special place in the region. Faced with severe external threats, they are forced to maintain a high level of combat readiness by the armed forces and, accordingly, resort to frequent military purchases. As U.S. allies, the two countries can obtain weapons under U.S. military assistance programs. Now these countries are at different phases of renovation cycles of their armed forces. South Korea is ranked second in the world (after India) for arms import with an annual purchasing volume of over $2 billion. The country imports large quantities of arms from the USA, primarily combat aircraft (anti-aircrafts) and missiles, and (anti-ship missiles and air-to-air rockets). However, Taiwan in recent years has significantly reduced its imports, while in the second half of the 1990s the country was the world leader in the procurement of armaments. Then, fearing a sharp rise in the capabilities of the Chinese National Liberation Army, buying large amounts of military equipment from Russia, the leadership of Taiwan implemented a forced large-scale rearmament program, and today this country no longer has any major need for new supplies.

The third group consists of countries with territorial or political claims against each other. This includes countries in South-East Asia, as well as Peru and Ecuador. Military procurements in these countries are subject to the logic of maintaining parity with their potential opponents in the development of the armed forces. Vietnam, Malaysia, Indonesia and Singapore, which have historically difficult relations, keep track of each other’s military acquisitions and develop their armed forces to meet new threats.

Singapore stands out among the countries of South-East Asia. This small island nation has powerful modern armed forces and is among the five largest weapons importers in the world. Moreover, the country has a developed defence industry and is close to being self-sufficient in a number of weapons (primarily on equipment for ground troops and warships). Malaysia and Indonesia have their own military industry, although not so developed. These countries have announced a cooperative effort to develop their military-industrial complex in order to reduce dependence on imported weapons. A wide geographical diversification of suppliers is a peculiarity in Southeast Asia’s arms imports. Over the past ten years, more than ten countries supplied weapons to Malaysia. This practice is considered as a reflection of the multi-vector nature of foreign policy in the region, even though it negatively affects the combat capability of the army because the military would have to master the weapons of different manufacturers.

The fourth group consists of states which, because of weak economic development, cannot maintain modern armed forces and carry out large-scale arms purchases. These include Cambodia, Philippines, and Papua New Guinea. There are weapons supplies to these countries from time to time – second-hand and deactivated weapons are mostly imported.

Finally, the fifth group consists of countries that do not have their own armed forces or that have decorative armed groups – Pacific island nations, Costa Rica, and Panama. The military security of such states is guaranteed by the major powers, and so, weapons for them are not a necessity.

Russia in the APR arms market

Today, the APR is the second most important arms market for Russia after India. From 2007 to 2011, our country supplied weapons worth $14 billion to APR countries, accounting for about one-third of all Russian arms exports (see Table 4).

Table 4. Main buyers of Russian arms among APR countries

| Buyer | Supply volume between 2007 and 2011, at 2011 prices, million USD | Share of total volume of Russian arms exports between 2007 and 2011 |

|---|---|---|

| China | 8359 | 15.93 |

| Vietnam | 2319 | 4.42 |

| Malaysia | 2255 | 4.3 |

| Indonesia | 774 | 1.47 |

| Peru | 122 | 0,23 |

| Colombia | 108 | 0,21 |

| Others | 117 | 0,22 |

| Entire APR | 14054 | 26,78 |

Source: SIPRI Arms Transfers Database.

The structure of Russian exports to the region by type of weapons differs from the overall structure of Russian arms exports. Russia virtually does not supply armoured vehicles to APR countries (an exception is supply contracts for a total of 71 BMP-3F infantry fighting vehicles to Indonesia), but the proportion of ammunition (especially missiles) and aircraft engines (due to supply to China) is significantly higher. The proportion of supply of air defence systems is above normal. However, combat aircrafts maintain a dominant role in the export structure – over 50%.

China has been Russia’s main partner in the sphere of military-technical cooperation in the region since the mid-1990s. For both sides, this cooperation was of great importance. It can be argued that it was arms supply to China that allowed the Russian military-industrial complex surviving and maintaining its potential in the 1990s, when the volume of orders from the Russian army was reduced to a minimum. At the same time, delivery of Russian high-tech equipment and mastering of its licensed production in China allowed China taking its military-industrial complex to a new level. The latter circumstance caused a significant reduction in the supply of Russian weapons to China because the Chinese no longer needed many kinds of weapons, as they were able to produce them by themselves. For example, China mastered the production of J-11 fighter aircrafts, which is essentially a copy of the Russian Su-27, and J-15 – a copy of Su-33. China is only interested in the most high-tech products – aircraft engines and missiles. Russia supplies AL-31FN engines for the Chinese J-10 fighter aircrafts, and Kh-59MK missiles for the Chinese Su-30. In March 2012, it became known that Russia and China were close to signing a contract to supply 48 Su-35 fighter aircrafts worth about $4 billion. However, there is an obstacle – Russia is demanding a guarantee from China not to attempt to copy the fighter aircrafts which, obviously, the Chinese were counting on. The outcome of these negotiations will determine the future of Russian-Chinese military-technical cooperation.

The second most important partner for Russia’s military-technical cooperation among the APR countries is Vietnam, which signed one of the largest contracts in recent years with Russia – for the supply of six submarines (project 636) worth about $2 billion. Besides, Vietnam received two frigates (project 11661) and a total of 28 Su-30MK aircraft fighters and other weapons. In 2012, the country is expected to receive additional batch of 20 Su-30MK2 aircraft fighters. Su-30MK aircraft fighters are generally Russian “bestseller”. They were also ordered by Malaysia (18 machines) and Indonesia (received 5, ordered 6 more). Indonesia was granted a loan of $1 billion up to July 2013 by Russia to purchase weapons.

Perspectives

Thus, China, Vietnam, Indonesia and Malaysia account for 95% of Russian arms exports to APR. Exports to other countries in the region are sporadic in nature. At the same time, Russia is not present in a number of intensive markets, especially South Korea and Singapore. This is due to the traditional political orientation of these countries to the United States. However, it is obvious that with the gradual reduction of supplies to China, Russia will have to seek new markets. The possibility of supplying ready-made systems to such countries as Korea and Singapore is unlikely, while a joint development of weapons systems may become for Russia the most perspective option for a military-technical cooperation.

With regard to the relationship with current major buyers of weapons among APR countries, much will depend on the development of Russian combat aircraft program, in the first place is the program on Su-35 construction (and on the progress of the Russian-Chinese negotiations on this subject), and in the longer perspective is the fifth generation fighter. If Russia will be the first to enter the military aviation market of the countries of this region with such a fighter, then there will be no doubt that Russian exporters would maintain their position there. However, the opportunity to significantly increase Russian arms exports to APR countries has been largely exhausted. The task rather is to maintain current supply levels. The situation can only change through an escalation of existing conflict in the region, leading to an abrupt increase in arms procurement.

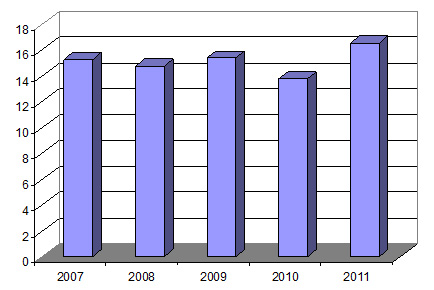

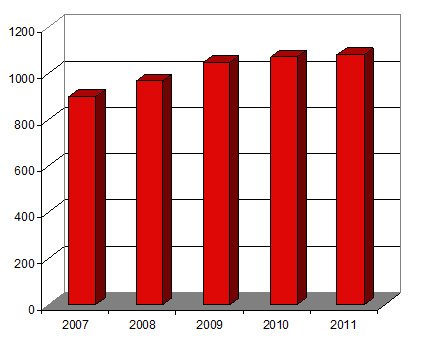

The main sources of tension in the Asia-Pacific region are known: the Korean and Chinese-Taiwanese problems, territorial claims, ethnic and religious conflicts in Southeast Asia, the border conflict between Peru and Ecuador. Escalation of any of these conflicts in the near future, and corresponding increase in the supply of weapons is possible, but as long as growth in arms imports (see Fig. 2) by APR countries is generally in proportion to their economic development, and increase in budget and military expenditures (see Fig. 3).

Fig. 2. Total import of weapons by APR countries (in billions of dollars at constant 2011 prices)

Source: SIPRI Arms Transfers Database.

Fig. 3. Total military expenditures of ATP countries (in billions of dollars at constant 2010 prices)

Source: SIPRI Military Expenditure Database.

It is hoped that increase in imports of weapons by APR countries is just another reflection of the growing role of the region in world politics and economics, and not a preparation for a major military conflict.

(no votes) |

(0 votes) |