Russia-U.S. Economic Relations: Old Problems and New Horizons

In

Login if you are already registered

(no votes) |

(0 votes) |

PhD, Associate Professor, Department of Political Science and Sociology of Political Processes, Faculty of Sociology, MSU

Russia-U.S. relations are in a protracted state of transition. The relatively clear framework of strategic confrontation that existed during the Cold War has been diluted, and the two sides are in a painful process of searching for a basis for partnership. However, despite certain progress made during the “reset” initiative, it is clear that, in order to overcome the legacy of the past, some more solid systemic foundations for cooperation are needed.

Russia-U.S. relations are in a protracted state of transition. The relatively clear framework of strategic confrontation that existed during the Cold War has been diluted, and the two sides are in a painful process of searching for a basis for partnership. However, despite certain progress made during the “reset” initiative, it is clear that, in order to overcome the legacy of the past, some more solid systemic foundations for cooperation are needed. How the response to the Syrian civil war has developed shows that, although the parties have different views on addressing this issue, they can still find compromises. Individual successes in further bilateral partnership are interspersed with the periodic cooling of relations, thus prompting the Russia-U.S. dialogue to develop along a curve that rises and falls. Whether or not it will be possible in the future to decrease the amplitude of these fluctuations depends not only on the will of the governments and diplomats in question, but also on whether we succeed in establishing a system-wide groundwork for interaction. Voices are increasingly being heard on both sides arguing that economic relations could become just such a system-forming element. However, multiple hurdles spring up during attempts to implement the apparently simple equation “good business relations equal good political relations.” First, the economic agenda that was pushed aside to the margins of bilateral dialogue has been excessively politicized. Second, relations remain broadly one-dimensional – lacking a deeper mutual integration of business communities. Therefore, there is a clear need to define the vectors of economic cooperation that will not only contribute to further trade growth but which will also help address the strategic tasks that Russia is facing: attracting investment and improving the investment climate, modernizing Russia’s industrial and technological potential and a quantum leap in innovation development.

Under the Sign of WTO

However, multiple hurdles spring up during attempts to implement the apparently simple equation “good business relations equal good political relations.” First, the economic agenda that was pushed aside to the margins of bilateral dialogue has been excessively politicized. Second, relations remain broadly one-dimensional – lacking a deeper mutual integration of business communities.

Three landmark events for Russia-U.S. economic relations took place in 2012 that had been anticipated for over 20 years. On August 22, 2013, Russia became the 156th member of the World Trade Organization (WTO), and in November, the U.S. Congress repealed the Jackson-Vanik Amendment, after which President Barack Obama signed an Act on permanent normal trade relations (PNTR) status for Russia.

The U.S. expert and business community hailed the latter as a victory, pushed through by American lobbyists representing in the first place the interests of 700 companies that are members of the American Chamber of Commerce in Russia (ACCR). The Washington-based Coalition for US-Russia Trade that unites 22 companies, including PepsiCo, General Electric, Caterpillar, Boeing, Procter&Gamble and other major corporate entities was the most significant pressure group calling for Russia to be given PNTR status. Before this historic event took place, the Peterson Institute for International economics calculated that, after Russia’s accession to the WTO, U.S. exports may increase five-fold i.e. to about $50 billion from today’s $10.7 billion (just 0.6% of the total volume of U.S. exports). It is worth noting that Russian exports to the U.S. totaled $29.3 billion in 2012, i.e. it is three times as large as U.S. exports to Russia, and the negative trade balance between the U.S. and Russia has increased over the past eight years from $4.4 to $18.6 billion. From the inception, the United States regarded Russia’s WTO membership as an opportunity for its producers to compete for the rapidly growing Russian market, where the U.S. lags behind the EU and China.

Russia-U.S. Relations: Go Economy!

Trade relations between the U.S. and Russia are developing around some key commodity items: Russia supplies oil and oil products (74 percent of the total volume of U.S. exports), metals and metal products, and gems (15 percent), chemical products (8 percent); and buys machines and equipment (56 percent of U.S. exports to Russia), food products and agricultural raw materials (15 percent), and chemicals (13 percent). The numerical prevalence of these goods compared to other categories has been noted for several years, but the total volume of trade turnover is clearly inconsistent with the two countries’ economic potential. U.S. companies hope that Russia’s adoption of WTO rules will allow them to significantly reinforce their positions and diversify their exports to the Russian market. The U.S. International Trade Commission notes that there is a growing demand for U.S. products in Russia. It mentions computer equipment and software, and chemical products (the exports of the latter increased 700 percent 2009 to 2011) in particular. The manufacturers also intend to increase supplies of technical machinery and special equipment given the expected reduction of import duties in Russia. The U.S. agricultural sector has particular expectations in connection with the WTO – especially the suppliers of meat and poultry who are currently waiting for Russia to review their certification standards – which would limit the options for Russia to slap restrictions on U.S. imports.

Nevertheless, the reduction of customs’ duties after Russia’s WTO accession will be gradual, taking from 2 to 7 years. Therefore, it offers a medium-term possibility that U.S. exporters will benefit. However, according to World Bank estimates even before Russia’s WTO accession, its tariffs fell from the average 14 percent to 8 percent, but this only had a modest impact on Russia-U.S. bilateral trade. On the other hand, even high tariffs did not prevent Russia from actively increasing its trade with the EU and China during the 2000s. Therefore, the tariff policy is not the only impediment to Russia-U.S. bilateral trade relations. Based on current trends, moderate growth in trade can be forecasted for the next 2-3 years and the predicted 5-fold increase of U.S exports to Russia seems unlikely for the time being.

Besides, there are no compelling grounds for favorable forecasts suggesting that Russian supplies to the U.S. will grow. The “shale revolution” may help the U.S. reduce its dependence on foreign oil – the main item it imports from Russia. Today, sales of Russian oil to the West coast of the United States has dropped to 2009 levels, at 174 thousand barrels for 2012, slipping below the record highs of the mid-2000s when supplies were approaching the 500-thousand-barrel mark. Therefore, Russian and U.S. energy companies have scant grounds to consider the U.S. a priority market for the further diversification of fuel and energy supplies.

Cooperation among oil and gas companies on Russian and American oil and gas fields and in third countries seems a much more promising area. Agreements between Rosneft and ExxonMobil on joint exploration of the Arctic shelf and oilfields in the Gulf of Mexico and Texas made a breakthrough in this direction. It is hoped that Rosneft will become the first Russian company not only to enter the U.S. market but also to gain access to the latest technologies used in shale production.

Investment Climate

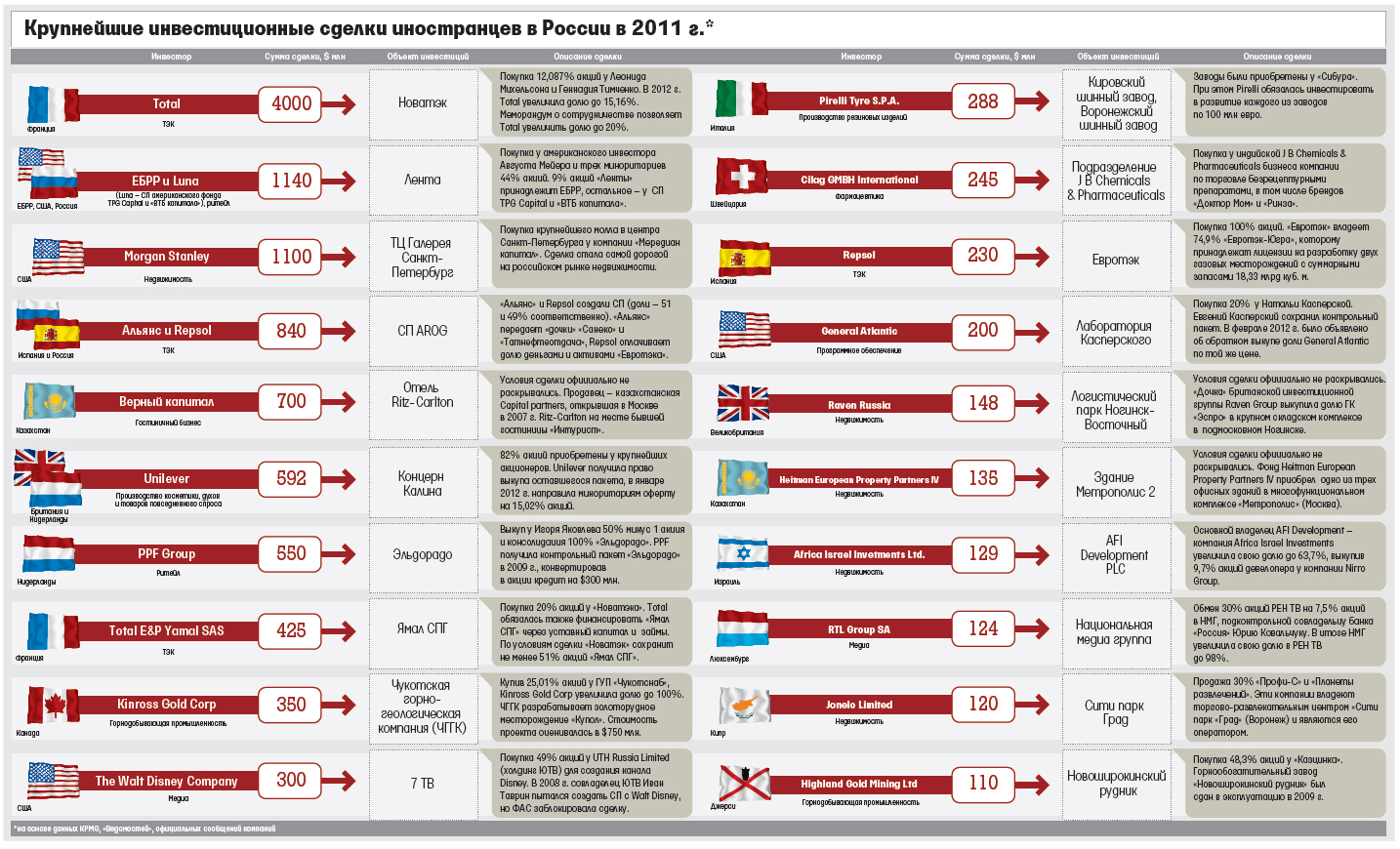

Russia-U.S investment cooperation today remains uncertain. In 2012, direct investments (DI) to the Russian economy totaled $18.6 billion whereas total investments amounted to $353.3 billion. However, the volume of cumulative investments from the U.S. has barely changed since 2005, at around $7-8.5 billion, of which DI totaled $3-4.5 billion – an indicator that does not even put the U.S. as among Russia’s top 10 leading investment partners. Natural resources and the consumer market remain the main objects of interest for U.S. investors. 50 percent of all direct investment from the U.S. come from three energy giants: ExxonMobil, ConocoPhillips, and Chevron, which are interested in major oil production projects such as Sakhalin-1, Caspian Pipeline Consortium, Narianmarneftegaz etc. At the same time, the assets of a number of other major corporations in Russia’s food sector (PepsiCo; Mars), automotive industry (General Motors; CAT; Ford), information technologies (IBM; Microsoft), and aircraft industry (Boeing) have became some of the most profitable in the world. However, the large scale initial investments made by most of these corporations took place in the 1990s while today they have refocused on an incremental growth strategy. In the regional profile, most American investment, 82 percent, is focused on Moscow, the Moscow Region, St. Petersburg, the Arkhangelsk Region and Krasnodar territory, while recently economic cooperation has expanded with the Tyumen and Samara regions and the Republics of Tatarstan and Komi.

The Russian investors are essentially not involved in the service sector, which is the foundation of the U.S. economy. The potential is also limited because investment is focused on major strategic sectors, which are under partial protectionism from the government.

Russian business is also gradually increasing its investment activity in the U.S., especially in the metals sector, which accounts for 65 percent of Russian investment by the three leading companies in the sector – Severstal, Norilsk Nickel and EVRAZ. All these companies have been engaged in active expansion on the U.S. market since 2007-2008. Thus, bilateral investment activity is focused on the industrial energy sector and several industrial giants. The Russian investors are essentially not involved in the service sector, which is the foundation of the U.S. economy. The potential is also limited because investment is focused on major strategic sectors, which are under partial protectionism from the government, stipulated in the U.S. Foreign Investment and National Security Act of 2007. On the other hand, U.S investors in Russia are discouraged by strict regulations, opaque investment procedures and the lack of a clear mechanism to protect investments made.

The outcome of negotiations on uniform methods of tax information exchange will in many ways determine the future of Russia-U.S. investment cooperation. As of January 1, 2014, the U.S. will see the Foreign Account Tax Compliance Act (FATCA) come into force. It was enacted to combat tax evasion by U.S. citizens but authorizes the Internal Revenue Service (IRS) to make inquiries into accounts opened in U.S. dollars. On the one hand FATCA can be considered as optimization taxation in off-shore zones, and on the other – as a mechanism that will allow the U.S. to systematize and consolidate information on dollar-denominated financial flows, which, as skeptics say, will give the U.S. economy a competitive advantage while compromising the economic sovereignty of the countries that will sign up to the new regulations. Russia, along with many other countries, in the world is definitely in a losing position because of the extremely high dollar dependency: 45.8 percent of national reserve assets are held in U.S. dollars, and the dollar accounts for the lion’s share of financial transactions in the country. In other words, in order to maintain the status quo on the domestic market Russia cannot but join the FATCA. The only question is to how this will be organized. An intergovernmental agreement between Russian and U.S. tax agencies to regulate corruption would be the best possible solution. This would not only reduce the risk of financial isolation of certain Russian banks, but it will also reveal new opportunities for state regulation of domestic financial sector. It makes sense for Russia to use the opportunity of its G20 Chairmanship and propose FATCA issues in a multilateral forum.

The Shadow of the Congress

WTO Director General Pascal Lamy and

Russian Prime Minister Dmitry Medvedev, 2011

However, despite some successes in bilateral economic cooperation, politicization remains a problem. Thus, Congress members who are most conservatively minded vis à vis Russia and who have consistently slowed down the process of repealing the Jackson-Vanik amendment managed to legally link PNTR status with the Magnitsky Act, creating a negative media environment for this landmark improvement in economic relations. It is indicative that the law, which was initially opposed by the Barack Obama Administration and the U.S. business community, was passed with the direct involvement of just a few interest groups – none of which was related to business. The adoption of the Magnitsky Act among other factors was due to the Russian side’s lethargy – with officials preferring not to interfere with the legislative struggle in Washington.

This suggests that the Russian business community and government have a very important task – to create a systemic pro-Russian lobby in Congress. The Russian side’s inactivity extends to trade relations. Thus, the U.S. still maintains anti-dumping duties on carbamide, ammonium nitrate and hot-rolled steel supplied from Russia. According to U.S. Assistant Secretary of Commerce Michael Camuñez, the anti-dumping measures often remain in force because the Russian companies are unwilling to push for their renegotiation. Russian companies (and Government entities) prefer to act through intermediary pressure groups – specialized consulting and legal agencies working on a contractual basis. However, these entities have limited influence – they can help penetrate the business establishment (as APCO Worldwide Inc. did for Rosatom subsidiaries Techsnabexport and UraniumOne), or sign a business agreement, but they are unable to promote the interests of entire sectors of economy. That requires a coordinated strategy among Russian corporate groups, industrial associations and alliances, and their official registration in the Congress’ lobbying structures.

The examples of China and Japan show that only by developing extensive business networks across the U.S. and building direct contacts with the local and federal authorities can an effective lobbying network be created. This reveals the main problem of Russian-American economic partnership, namely its persistent structural limitations. Both trade relations and investment interaction between Russia and the U.S. have been concentrated at the top of the two countries’ economic hierarchies. A middle and lower level of interaction is required to build a more reliable systemic basis of Russia-U.S. relations. There are grounds to believe that not just small- and medium-size enterprises but also innovation-based business will provide that level of interaction.

Innovations in the Economy – Innovations in Relations

The problem for the U.S. innovation community also results from the fact that innovation companies, foundations and incubators often lack sufficient information regarding the Russian market. It was a surprise for many U.S. investors that Russia was rated 14th in the Bloomberg and Business Week ranking of the top innovative countries far ahead of China and Israel.

Developing innovative businesses is a priority area not only for Russia’s economy but also for building partnership relations with leading trading partners, including the United States – one of the world leaders in the support, development, promotion and application of innovations. The potential of cooperation with the U.S. in this area significantly expands the opportunities for the implementation of foreign economic strategy. The United States, as a world leader in innovation development, has transformed technological development into a pillar of the economy – not only demonstrating the advantages of economic growth through innovation but also offering new opportunities for Russian businesses.

The main strategy for technological cooperation should focus on the joint funding, development and commercialization of innovations. Venture funds that are ready to finance promising start-ups are the driving force of this funding. In recent years, venture funds have preferred to invest in information and communication technologies (ICT). The global ICT market exceeds $3 trillion but U.S. and Russian participation is highly skewed – 28 percent against 1.8 percent, respectively. Nevertheless, Russia is gradually gaining influence on the innovation market, especially due to the aerospace industry, nano- and bio-technologies and atomic energy uses.

The problem for the U.S. innovation community also results from the fact that innovation companies, foundations and incubators often lack sufficient information regarding the Russian market. It was a surprise for many U.S. investors that Russia was rated 14th in the Bloomberg and Business Week ranking of the top innovative countries far ahead of China and Israel. However, statistical successes are not enough – it is necessary to start working directly with potential American partners. This is how the business started in Russia for the well-known Californian incubator, Plug and Play Tech Center (PnP), which initially did not consider the project as promising. Only after many months of negotiations initiated by the Global Venture Alliance did the PnP approach the Russian market. However, after initially supporting 5 start-up projects, the company narrowed its activity to promoting the interests of U.S. IT companies and internship programs for Russian entrepreneurs in the United States.

Barack Obama and Dmitry Medvedev tare

discussing membership of Russia in the WTO

Cooperation in the area of innovation also has its concealed risks. The main risk for improving relations between the Russian innovation community and U.S. investors and scientific centers, against a backdrop of increased corruption and feeble domestic opportunities for the Russian scientists and entrepreneurs, is the risk that individual experts and entire enterprises will leave the country.

U.S. investors realize that there is a great potential for Russian innovations but they also see that, due to red-tape and a lack of relevant regulations relating primarily to protecting property rights, they are hesitant to directly support independent domestic start-ups. They prefer instead to invest in high technologies on Russian territory together with major corporate entities thus reducing administrative risks and increasing the potential successful commercialization of high-tech products. A clear example is the Rosnano Corporation that signed a $760 million contract with the U.S. Domain Associates venture fund to finance 20 medical companies in Russia. Moreover, 4 SelectaRus and BindRus laboratories are being built in Khimki as a result of the joint project of Rosnano, Selecta Biosciences and BIND Biosciences for a total of $94.5 million.

Another model for the development and further commercialization of technologies is the establishment of inter-regional partnership alliances along the lines of the EURECA program under the U.S.-Russia innovation corridor. The Program covers joint activities between the St. Petersburg University of Information Technologies Mechanics and Optics, the Nizhny Novgorod State University, the Maryland University, the California University and Purdue University with a goal to integrate the Russian higher education institutions and technological centers in the program at an early stage of technological development; develop the culture of innovation and enterprise among young researchers; create infrastructure to support technology transfers, and to attract seed and venture capital. Another example of implementation is the Innovation Hub in Houston, Texas, established under the auspices of the U.S.-Russia Chamber of Commerce to attract Russian companies, which provides them with an opportunity to open branches and commercialize technologies in the United States. It should be noted that this process is not unilateral – several Russian regions also position themselves as potential clusters for U.S. innovation companies. Steps have been taken to promote the country’s Special Economic Zones (SEZ) for high technologies in Dubna, St. Petersburg, Lipetsk and Tomsk. Currently, one-quarter of all announced foreign investment in high tech SEZ has been U.S. capital – 25.8 out of 100 billion Rubles, and an increasing number of U.S. innovation companies, universities and venture funds have been showing interest in these SEZ. There are also examples of more specialized single-discipline cooperation, such as the establishment, together with Arizona State University, of a joint Russia-US Cancer Research Center based at Altai State University. It is the scientific and academic model that has the greatest relevance and potential for Russia, since it is a matter of the long-term development of the economic and innovative culture and deeper integration processes.

There is no doubt that cooperation in the area of innovation also has its concealed risks. The main risk for improving relations between the Russian innovation community and U.S. investors and scientific centers, against a backdrop of increased corruption and feeble domestic opportunities for the Russian scientists and entrepreneurs, is the risk that individual experts and entire enterprises will leave the country. U.S. partners are interested not only in creating an innovation environment in Russia (which is for them a mid- and long-term prospective) but also in attracting highly skilled Russian specialists to the U.S. This is why it is necessary to create a system in which Russian specialists can obtain new competencies in the U.S. without breaking their institutional ties with Russian – this decision will require substantial financial support from the Government and major businesses in addition to measures to make the research and business environment more attractive.

Searching for Solutions

The following measures are proposed as ways of overcoming the existing limitations in trade and investment activities:

1.Work more actively to establish multi-industry alliances. There are more than 7500 industrial associations in the U.S., but their interaction with Russian industrial and business groups clearly falls short. The Russian-American business dialogue launched in 2008 and the Russian Union of Industrialists and Entrepreneurs’ (RUIE) experience with America’s business community should be used as a benchmark for policy and consultation. In a dynamically transforming fuel and energy market there is a clear need not only to support inter-corporate contracts but also to pull the Russia-U.S. energy dialogue out of a semi-frozen state.

2. A new regional investment initiative is required to strengthen the economic interaction among the constituent regions of the Russian Federation and the United States of America. For this purpose it is recommended to use channels of communication with federal and regional parliaments and executive authorities, and also with regional business associations and the business community. The Russian Government and major businesses should more actively support the Russian American Pacific Partnership, furthering the goal of inter-regional interaction between the U.S. and Russia and deeper integration of the Russian Far East in the APEC and global economic environment.

3. U.S. investors fear the high risks associated with problems in foreign companies privatizing property, and, therefore tend to avoid major initial investments, preferring instead projects that offer good short-term profit generation prospects. The problems of undesired filters in the investment environment should be more actively revealed to show that Russia is prepared for an open dialogue and greater transparency.

For this to happen, it will be necessary to monitor investment problems by sector, company and individual regions and to detail the results on bilingual websites. This will help increase the level of natural competition among Russian sectors and regions that want to attract U.S. investment. The RUIE, Chamber of Industry and Commerce of Russia, U.S. Chamber of Commerce and the U.S.-Russia Business Council should all participate as consultative and coordinating bodies.

Second, the mechanisms that protect investments against political, currency exchange and other risks should be introduced more actively. At present there is no uniform interpretation in Russia of an international legal mechanism for investment protection as enshrined in two Conventions: the Seoul Convention (that Russia joined in 1992), and the Washington Convention (not ratified by Moscow). Using the momentum of negotiations on FATCA accession, Russia should intensify discussions on investment legislation and investment insurance.

4. Promoting Russian-American cooperation on innovations requires not only the development of the domestic investment climate but also a more aggressive promotion of the opportunities offered today by the Russian side. It makes sense to more actively engage Russian and foreign advertising, marketing and consulting companies that could help develop a strategy to promote Russian innovations to the U.S. market. Another important element is extending the practice of holding more events such as the forum on Global innovation partnership and Russian innovation week in California since a large number of investors and companies still have only a vague notion of Russia’s innovation potential.

However, the key link is the development of channels of communication among Russian and U.S. Universities, research centers and innovation enterprises. Bilateral partnership and technology exchange programs should be introduced that would allow Russian scientists and business to replicate the experience of promotion, marketing and commercialization of technologies – the elements that domestic innovation specialists chiefly lack. The government agencies’ role is to establish the necessary legal framework in order to enhance the commercialization of innovations. In this vein, it seems logical to establish a separate agency under the Russian Government or President that would lead the formulation and implementation of comprehensive measures to provide legal and information support to the innovation sector.

5. Finally, Russia needs today not just the lobbying of its interests in the U.S. but a more thoughtful strategy for promoting its image and more direct contacts with the U.S political and business establishment. For the time being, Russia has not yet established a fully-fledged lobbying network, although there are grounds to believe that it might emerge. Individual Russian companies and businesspeople participate in status meetings at the highest level, but if Russia is not interested in a more considered movement into the U.S. economic space, then it makes sense to take a look at the example of China. Since 2010, the major Chinese trade and industry associations have been launching concerted efforts to register as official lobbyists in the U.S. Congress and today they are acting as important players on Capitol Hill. Intermediary lobbying firms, such as McGraw-Hill, APCOWorldwideInc, and Ketchum, whose services are hired by the Russian corporate business, perform well at the initial stages. However, in order to find a systemic basis for interaction to overcome the inertia of American establishment, knowledge of the U.S. legislation and an understanding of the nuances of the decision-making process are required.

Russia and the U.S. have a long way to go in overcoming their differences and the relics of the Cold War. As long as mutual economic interests are not priorities on the agenda, political differences will remain a determining factor – whether the President is a Republican or a Democrat – and whichever party controls majority in the U.S. Congress.

(no votes) |

(0 votes) |