Greece at the National Elections’ Crossroads: A Step Towards Left or Right?

Vostock Photo

A supporter of Alexis Tsipras, leader of

the Greek radical left main opposition party

SYRIZA, displays a poster reading "Change

Greece - Change Europe" during the last

preelection rally of the party in Athens,

22 January 2015

In

Login if you are already registered

RIEAS Senior advisor based in Athens, Greece and Associate at the Centre for Strategic Studies, University of Jordan

Director of the Research Institute for European and American Studies based in Athens, Greece

The upcoming January 25, 2015 national elections in Greece highlight a major challenge as they present a struggle between anger against austerity and fear of euro exit. The apparent reason that led to early national elections is the failure of the coalition government to obtain a parliamentary majority to appoint a candidate as president of the Republic.

The upcoming January 25, 2015 national elections in Greece highlight a major challenge as they present a struggle between anger against austerity and fear of euro exit. The apparent reason that led to early national elections is the failure of the coalition government to obtain a parliamentary majority to appoint a candidate as president of the Republic [1] . The hidden motive behind the declaration of early elections however was the volatile political landscape that made strenuous coalition government’s compliance with the Troika’s tough agenda thus postponing structural policy reforms by fear of the social effects that could be translated into high political cost. The Greek Prime Minister was between Scylla and Charybdis in terms of sustaining the coalition government and meeting Troika’s demands for unimpeded economic support.

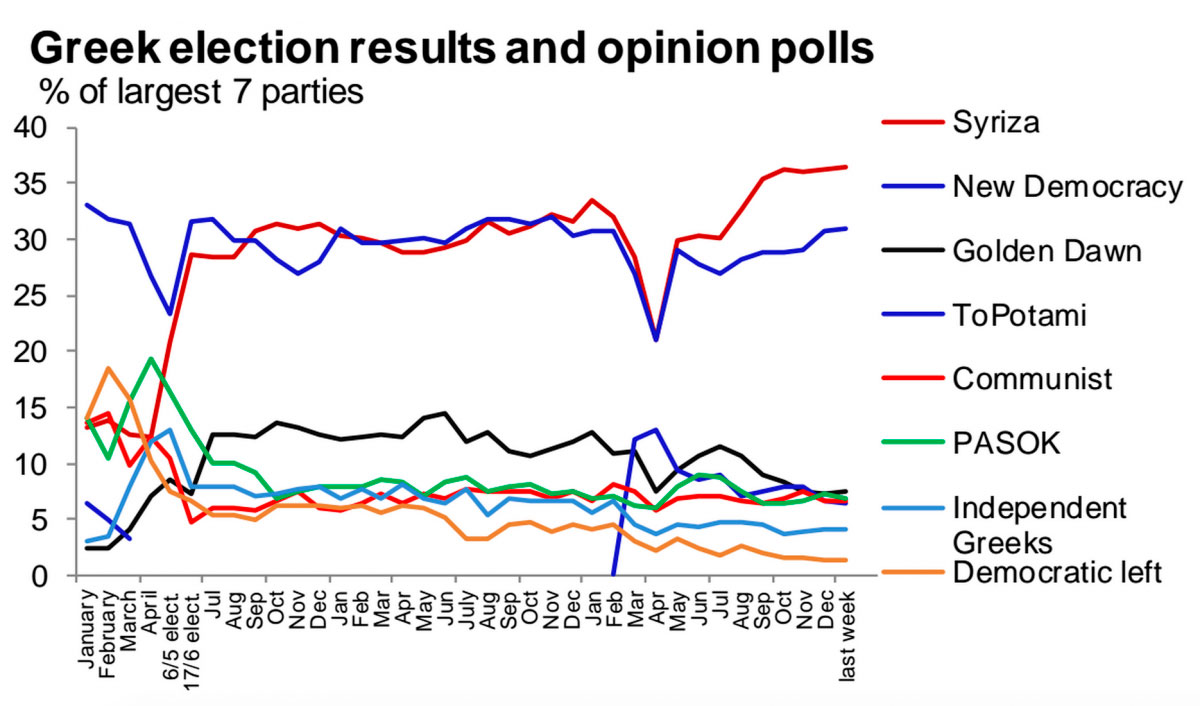

The majority of polls show that SYRIZA, the main opposition party that has engulfed supporters from radical leftists to socialists in an effort to broaden its electoral base, will maintain a clear lead with percentages ranging from 28 to 31, while the ruling New Democracy’s performance ranges from 23 to 28 % [2]. The coalition partner PASOK continues to shrink from the 2009 voter turnout of 43.92 % to 12.28 % in the 2012 national elections. A progressive shrinkage is recorded for center-left DIMAR, formerly coalition partner, with limited chances to enter parliament because of the alibi it offered to the coalition government’s strict austerity policies [3]. Polls also suggest that the Communist party of KKE, the liberal party of The River, and the nationalist Golden Dawn are certain to enter parliament.

The Greek Prime Minister was between Scylla and Charybdis in terms of sustaining the coalition government and meeting Troika’s demands for unimpeded economic support.

The formation of a majority government is a spinous matter because of the partisan fragmentation and the existent electoral law which although awards a 50 bonus seat to the winning party, it simultaneously conditions the ability to form a majority on the voter turnout of political parties that remain outside parliament [4]. In case that no party forms a majority government, the Greek President will have to give order to the winning party’s leader to form a coalition within three days, and if he fails the same process will be followed with the second and third parties’ leaders. In the event of a failure, a second round of elections has to be held within a month [5].

The prospect of political instability has generated a cataract of reactions that have directly affected the country’s economy with most prominent investors’ selling Greek bonds and stocks. Greek stocks have fallen 24 % since early December 2014 when national elections were declared for early 2015 instead of 2016 as originally scheduled. The Athens Stock Exchange slipped on January 5, 2015 to its lowest level since November 2012. Greek bonds have lost 7.4 % over the same period presenting the worst performance of 34 sovereign securities tracked by Bloomberg's World Bond Index [6].

force-it-out-of-the-euro

Greek elections results and opinion polls,

Jan 2, 2015

Election campaigns’ intensity to affect voting intention differs significantly from one another and differences are meant to have far-reaching consequences for the cognitive strategies used by Greek voters. Throughout the election campaign, the essence is that the ruling party centers on a “roadmap” of measures for a “post-bailout Greece” concurrently using fear factors such as default and euro exit, while the major opposition relies on anti-austerity whilst unfolding a citizen-centric tactics.

The ruling party highlights that Greece has emerged from a six-year recession with the achievement of primary surplus and that the focus has already shifted on a growth plan for post-crisis which entails gradual tax reduction across middle-class households, support of the shipping, energy, pharmaceuticals and technology sectors, introduction of additional reforms to restrict bureaucracy and of an investment incentives’ package that foresees reduction of production costs and social security contributions. At the same time, the ruling party bases its campaign on fear factors with the aim to moderate austerity-produced public anger, with most protrusive an argument that Greece would be led to default and exit from the European single currency by the declared policies of the major opposition.

Does Greece really need debt relief? Is a euro exit possible? Can the vicious cycle of deflation that Greece faces be defeated and how?

A chain reaction was almost instantly triggered in the form of large-scale bank withdrawals amounting to €7 billion since December 2014 ahead of the January 25, 2015 elections according to data published by the Bank of Greece with large companies and individuals being the first to heave deposits [7]. The pressing liquidity conditions, as consequence of the growing outflow of deposits and the issue of treasury bills (T-bills) imposed by the State, have driven the country’s systemic banks to request cash from the Bank of Greece through the emergency liquidity system (ELA) [8].

Prime Minister of Greece and leader of New

Democracy Antonis Samaras

SYRIZA for its part attempts to display a strategy of image normalization prescribing a political program advertised as a viable alternative without endangering euro membership, in a country where unemployment has reached almost 1.5 million of a labor force of 4.5 million, incomes have declined to an approximate average of 50 %, hospitals are understaffed with lack of nurses and medical doctors, and working conditions are governed not only by three or five month temporary contracts but also by rented employees who receive freelancing rather than regular payments. The major opposition’s political proposals revolve around debt renegotiation aiming at partial debt relief, the fight against austerity with the gradual reintroduction of the minimum wage of €751 [9] , income redistribution through a radical tax system, debt restructuring for the most vulnerable households, and restoration of market liquidity by means of state control of the banking system. In a calculated attempt to broaden its electoral base, the major opposition has appealed to reluctant conservative social groups and devout Christians with the conduct of its leader’s visit to Mount Athos in summer 2014 and his participation in the public ritual of Epiphany in early January 2015 [10].

At a time when Southern European countries and France oppose the German-led austerity orthodoxy, a series of questions emerge and are related to the next Greek government’s strategy vis-à-vis Troika to secure ''trade-offs'' among issues that currently appear to be uncompromised with most prevailing the following: Does Greece really need debt relief? Is a euro exit possible? Can the vicious cycle of deflation that Greece faces be defeated and how?

Although a Greek exit will not be a systemic event causing a simultaneous breakdown in global confidence and trade as evidenced in the wake of the Lehman Brothers collapse, the travails of Europe will unquestionably impact the global stock markets and will send waves of shock to global confidence.

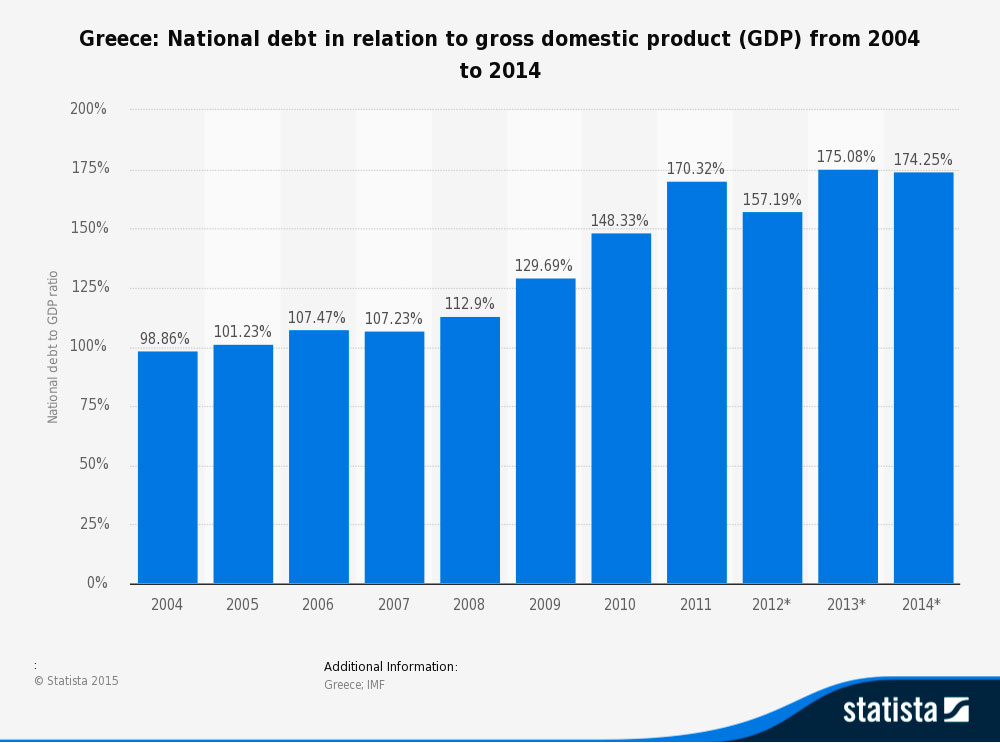

There is little doubt that the country’s debt-servicing bill declined because private financial investors have been replaced by Eurozone countries which currently own 60 % of Greece’s €322 billion government debt that equals to 179% of GDP [11]. The concluded extension of the country’s repayments to 2054 and the cut in interest payments is considered by many as equivalent to a haircut. Scepticism, however, seems to prevail when it comes to the feasibility of the country’s debt, in accordance with the official Eurozone projection, to fall as share of its GDP below 124 % in coming years [12] for three main reasons: First, growth forecasts are considered overly optimistic given that they predict nominal GDP growth of approximately 5 % annually from 2016 till 2020. Second, the hypothesis that Greece will achieve annual primary budget surplus equivalent to 4 % of the GDP is viewed as unrealized. Third, the crisis has migrated to the real economy in the form of deflation that makes Greece unsustainable given that, in 2014 alone, real interest rates exceeded 3 % due to the prices’ fall by 2.6 % [13].

A way out of the crisis, which has penetrated the European foundations, entails a debate on the kind of Europe that all member states envision.

That said, any debt restructuring process needs to maximize benefits based on a mutual agreement between Greece, the EU and the IMF so that a new deal renders Greece sustainable thus creating a precedent for sorting out Eurozone’s problems. The Outright Monetary Transactions (OMT) program of the European Central Bank (ECB) endorsed recently by the European Court [14] , which provides the purchase of hundreds of billions of Eurozone countries’ sovereign bonds on secondary markets, presents an enhancement in the bargaining power of any new elected Greek government and also advances the ECB’s plans for significant quantitative easing against the forces of deflation [15]. Specifically, the OMT program is appropriate to reduce interest rates on government bonds restoring significantly financial normality to states concerned, thus permitting the ECB to exert monetary policies in an environment of greater stability [16]. When it comes to the possibility of a Greek exit from the Eurozone, the challenges that may accrue can prove multifold. Although a Greek exit will not be a systemic event causing a simultaneous breakdown in global confidence and trade as evidenced in the wake of the Lehman Brothers collapse, the travails of Europe will unquestionably impact the global stock markets and will send waves of shock to global confidence. Equally important, the risk of contagion will increase, despite the various rescue mechanisms, and European policy makers will have to “circle the wagons” around the other periphery countries to cease occurrence. In other words, Greece could create a massive shock for financial markets and despite the fact that an exit from the eurozone is complicated technically, it could result in contagion because financial investors would try to test other Eurozone countries.

A way out of the crisis, which has penetrated the European foundations, entails a debate on the kind of Europe that all member states envision. Greece and its new-to-be-elected government could play a vital role in shaping the European debate away from populist slogans by fostering partnerships for a universally beneficial deal that could make European countries and their economies sustainable. In essence, at the end of the day, Europe is offered the chance to “write her injuries in dust, but her benefits in marble” [17].

References:

1. Stavros Dimas was appointed as presidential candidate and attracted the support of 168 MPs out of the 300, short of the 180 required votes. In accordance with the Greek constitution, the parliament was dissolved and January 25, 2015 was set as date for the conduct of national elections.

2. “Seven Party Parliament with No Majority”, Proto Thema (Daily) , 19 January 2015

3. F. Chatzistavrou and S. Michalaki, “Reshaping Politics of the Left and Centre in Greece after the 2014 EP Election”, EPIN Commentary, No.21, 110 September 2014.

4. Paris Ayiomamitis, “Greek Election Math and Scenarios: A Handy Guide”, The Press Project, 8 January 2015

5. Ibid. The Greek president will have to appoint the head of the Supreme Court as prime minister, the parliament will dissolve and a caretaker government will be established so that the second round of elections takes place.

6. Jonathan Stearns and Nikos Chrysoloras. “Samaras Faces Greek Voters Skeptical of His Euro-Exit Warnings”, Washington Post (Daily), January 5, 2015

7. “Seven Billion Euro in Outflows after the Declaration of Elections”, Proto Thema (Daily), January 19, 2015

8. The repeated issue of T-bills has caused a major blow to the Greek banking system’s liquidity as it is evidenced by the State raise of €2.7 billion in November 2014, the secure of €3.2 billion in December 2014 and the reserve of €2.7 billion in January 2015. Yiannis Papadoyiannis, “Greek Banks Make Requests for ELA Funding”, Kathimerini (Daily), January 16, 2015.

9. “Syriza’s First Act in Office: Raise Minimum Wage”, The Times of Change (News and Media Network), January 16, 2015

10. “Epiphany for the Greek Left: Spreading His Wings”, The Economist, January 6, 2015.

11. Dimitra Defotis, “Greek Victor: Debt Relief”, Barron’s (Magazine Weekly Edition), January 17, 2015.

12. Stephen Fidler, “Politics Risk Tripping Up Greece on Debt Relief”, Wall Street Journal, January 16, 2015

13. Ibid.

14. Court of Justice of the European Union, Press Release No 2/15 Luxembourg, 14 January 2015.

15. Jana Randow, “Europe’s QE Quandary”, Bloomberg, December 30, 2015.

16. Yanis Varoufakis, “On the ECB’s Latest Contradiction (And How It Helps Greece)”, January 15, 2015. Accessed at: http://yanisvaroufakis.eu/2015/01/15/on-the-ecbs-great-contradiction-and-how-it-helps-greece/

17. Paraphrase of a quote by Benjamin Franklin.

(no votes) |

(0 votes) |