Chinese Version of the Great Depression Syndrome?

Investors look at computer screens in front of

a electronic board displaying stock information

at a brokerage house in Fuyang, Anhui province

March 31, 2015

In

Login if you are already registered

(no votes) |

(0 votes) |

PhD in Economics, Head of Department of Assessment and Coordination of International and Duel Master's Degree Programs, MGIMO-University, MFA of Russia

The People's Bank of China may come to a decision on the next reduction of the discount rate or of mandatory reserve requirements for banks, if in the coming months consumer price inflation in the country continues to fall. This was announced at the beginning of March 2015 by a representative of the Monetary Policy Committee of the People's Bank of China. The intention to continue easing monetary policy had been expressed in anticipation of the next National People's Congress, which discussed the prospects for economic growth this year and defined the milestones of the country’s economic development.

The People's Bank of China may come to a decision on the next reduction of the discount rate or of mandatory reserve requirements for banks, if in the coming months consumer price inflation in the country continues to fall. This was announced at the beginning of March 2015 by a representative of the Monetary Policy Committee of the People's Bank of China. The intention to continue easing monetary policy had been expressed in anticipation of the next National People's Congress, which discussed the prospects for economic growth this year and defined the milestones of the country’s economic development.

In pursuit of liquidity

In the last six months, the Chinese monetary policy authorities have twice reduced the levels of the key interest rates in order to increase liquidity. In November 2014, the People's Bank of China cut interest rates on loans down to an annual 5.6% (by 0.4 percentage points) and on annual deposits to 2.75% (by 0.25 percentage points) [1]. In early March 2015, the corresponding figures were reduced by 0.25 percentage points to 5.35% and to 2.5% respectively. Moreover, in February 2015, mandatory reserve requirements were reduced by 0.5 percentage points (from 20% to 19.5%) [2]. On the one hand, a relatively small reduction in reserve requirements can be viewed as an attempt by the monetary policy agencies to maintain the stability of the banking system, while on the other hand, it serves as another signal to encourage consumer activity, to lower the savings rate and to stimulate demand.

Nevertheless, despite the dynamic efforts by the monetary policy authorities to stimulate domestic demand, expectations of increased deflationary pressure on the economy are still present. The current structural imbalances in the Chinese economy are a clear reflection of the consequences of increased production in the pursuit of export earnings in the absence of an adequate forecast of demand dynamics on both the domestic and foreign markets.

Despite the dynamic efforts by the monetary policy authorities to stimulate domestic demand, expectations of increased deflationary pressure on the economy are still present.

At the end of 2013, it became clear that the potential of the export-oriented model, which had provided high rates of GDP growth for several decades as well as the ability to build up international reserves, was exhausted. China then headed towards the reorientation of its economic system through the implementation of a large-scale package of market reforms involving the withdrawal of the state from most sectors of the economy, an encouragement of free competition, and the diversification of the sources of economic growth [3]. Beijing has focused on the transition from the model of expansion driven by foreign trade to the relatively more rapid accumulation of investments and the adoption of measures stimulating domestic demand and consumption. The government is taking active measures to stimulate household consumption and private sector development. Structural reforms affecting both fiscal and monetary policies are aimed at “stimulating innovation and improve productivity, deterring impractical investments and increasing the income and consumption of households.” [4]

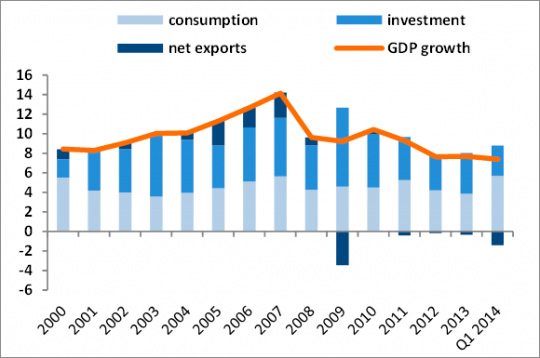

Indeed, the contribution of net exports to GDP growth in recent years has significantly decreased [5]. However, to what extent can the growth in domestic consumption resulting from the dynamic actions of the government (mainly due to the expansion of public expenditure) and of the monetary policy agencies (by encouraging borrowing for current consumption and development of small and medium-sized enterprises) offset this decline?

On the eve of depression

Back in the late 1990s, Nobel Prize winner in economics Paul Krugman warned about the threat of economic crises resulting from failures on the demand side of the economy. [6]

However, the central problem of the Chinese economy today is not so much the lack of growth in consumption, as the mismatch between its redundant productive capacity [7] and the chronic excess of supply over demand. And narrowing this gap in the short term appears to be unlikely.

The current situation is the result of the long-term economic strategy of the country, its level of exports, which in combination with the high price competitiveness of Chinese goods (provided, inter alia, by keeping the exchange rate of the yuan artificially low, which was very popular during the 2000s) and growing demand in foreign markets has for a long time borne fruit in the form of higher export revenues, the possibility of replenishing international reserves and the return of some part of the proceeds into production. The inertia in support for increasing the volume of production is most likely to continue in the next few years, although the rate of increase will gradually decline.

In turn, active measures to stimulate domestic demand are a recent trend, and will take time to stir the economy and overcome the high propensity to save, which is typical of most Asian countries.

Indeed, the contribution of net exports to GDP growth in recent years has significantly decreased .

In 1929, a similar mismatch between supply and demand, i.e. an overproduction of goods triggered by previously rapid economic growth, coupled with a lack of liquidity to balance excess supply and restrictions on the use of monetary policy instruments due to the gold backing requirements of the US dollar, generated a large-scale collapse of the US economy. Deflation and overstocking forced many businesses into bankruptcy overnight, causing a decline in stock market indices, growth in unemployment and a sharp reduction in income and quality of life [8].

In China today, supply greatly exceeds demand [9], and the structural reforms put into practice by the government and the People's Bank of China in anticipation of the due economic benefits in the long run are unlikely to stimulate consumption to the extent that could balance the country's economy in the short term.

Diversification of the economic growth model

According to UNCTAD experts, in recent years China has maintained the trend of reducing the “contribution” of net exports to GDP growth, while investments in fixed capital and private consumption, increased by the accelerated growth of wages, continue to stimulate the growth of production [10].

In 2014, World Bank experts forecast China’s slowdown in economic growth from 7.7% in 2013 to 7.6% and 7.5% in 2014 and 2015, respectively, while it was expected that the decline in the investment growth would be offset by growing domestic consumption due to increased household income [11]. This did happen in the first quarter of 2014. In 2013, it was domestic consumption that accounted for 5.7 percentage points of GDP growth in China [12]. The growth rate of consumption expenditure of the urban population showed a steady upward trend: from 9.5% on an annualized basis in the fourth quarter of 2013 to 9.9% in the first quarter of 2014. In 2013, the growth rate of retail sales reached 13.1%, which was slightly less then compared to the level of 14.5% in 2012, but car sales rose sharply from 6.9% in 2012 to 15.7% in 2013 [13].

Despite the increased “contribution” of domestic consumption to GDP growth, it was not sufficient enough to maintain the usual growth rates [14]. As a result, in early March 2015, the government was forced to refine the target GDP growth in 2015 from 7.5% to 7% [15]. Deflationary trends will put strengthening pressure on the national currency, which will decrease export competitiveness and reduce further export revenues and the share of net exports in GDP growth.

However, the central problem of the Chinese economy today is not so much the lack of growth in consumption, as the mismatch between its redundant productive capacity and the chronic excess of supply over demand.

The growth of external debt, especially in the corporate and banking sectors, is another alarming trend amidst this apparent “crisis of overproduction.” Although, according to recent estimates, credit growth has slowed [16], the level of borrowing in the Chinese economy remains significant. The level of outstanding bank debts in 2013 reached 135% of GDP as compared with 105% in 2007; the debt of the corporate sector makes up 125% of GDP and is one of the highest among the Asian countries [17]. At that, household debt during the same period totaled only 20% of GDP, which is an added testimony to the fact that the Chinese population has a long way to go to become a “consumer society.”

Cautious optimism

China is facing a “crisis of overproduction” caused by multi-year structural imbalances, aggravated by the worldwide consequences of the 2008-2009 crisis. Nevertheless, there are little grounds for expecting a collapse, which, in terms of its economic aftermath, is comparable to what happened in the United States in 1929.

First, China is one of the few countries that have launched a program of economic restructuring before reaching the bifurcation point and the sudden collapse of the market.

There are little grounds for expecting a collapse, which, in terms of its economic aftermath, is comparable to what happened in the United States in 1929.

Second, despite the continued surplus conditions, the gap between supply and demand is gradually narrowing through increasing the rate of growth of the domestic consumption and by reducing the rate of production expansion. In particular, in 2013, the growth rate of investment in manufacturing fell to 18.5% compared to 22% recorded in 2012. In addition, significant investment resources are being directed towards the development of infrastructure (irrigation, transport and logistics networks, high-speed lines, ports, etc.), and the expansion of tertiary industries (primarily labor-intensive ones, like construction that promotes employment generation, since human resources are a relatively abundant agent of production in the Chinese economy). In other words, the state adopted a policy of not just stimulating demand, but of improving its quality and increasing the share of services in GDP structure and its growth rate too.

Third, despite the maintained regime of effective intervention rate, which significantly limits the discretion of monetary policy, forcing central banks to carry out large-scale interventions to influence the exchange rate and inflation, counties today, particularly China, are relatively free to use the instruments of their monetary policy to increase liquidity.

References

1. China cuts interest rates to ease deflation worries // China Daily. 28 February, 2015. Available at: http://www.chinadaily.com.cn/business/2015-02/28/content_19680921.htm

2. Ibidem.

3. East Asia: the diversification of sources of economic growth // Asia-Pacific region: Economy, Politics, Law, 2014, # 3-4. Pp. 63-65 (in Russian)

4. David Dollar. Sino Shift // Finance and Development. IMF. June 2014. Vol. 51, No. 2. Pp. 11.

5. China Statistical Yearbook 2014. National Bureau of Statistics of China.

6. Paul Krugman. The Return of Depression Economics. USA, 1999.

7. George Magnus. Causes and consequences of China’s contagious case of deflation // Financial Times. 24 December, 2014. Available at: http://www.ft.com/cms/s/0/4e01133c-8a14-11e4-9271-00144feabdc0.html#axzz3VQwUZRyM

8. China Statistical Yearbook 2014. National Bureau of Statistics of China.

9. Ibidem.

10. UNCTAD Trade and Development Report, 2013, New York, Geneva, 2013. С. Iv.

11. China Economic Update. World Bank. June 2014. P.1.

12. Ibid., P.4.

13. Ibidem.

14. Asia-Pacific Trade and Investment Report 2014. UNESCAP. 2014. Р. 8.

15. Highlights of China's gov't work report for 2015. Available at: http://www.china.org.cn/china/NPC_CPPCC_2015/2015-03/05/content_34957640.htm

16. China Economic Update. World Bank. June 2014. P.5.

17. Ibid., P.6.

(no votes) |

(0 votes) |