Sunrise Expected Late: How Long Japan Will Be in Recession?

In

Login if you are already registered

(no votes) |

(0 votes) |

Notwithstanding a quite ambitious economic plan of reforms initiated by the Prime Minister Shinzō Abe Sind known as “Abenomics”, mid-November 2014 has shown that Japanese economy is not getting better. The Prime Minister Abe has turned to extreme measures – dissolution of the parliament with the new elections set for December 2014. Once ranking among the top three most innovative and strongest economies, Japan has now been stagnating for several years. What underlies this recession? How long will it stay like this? What public measures can be anticipated in order to deal with the stagnation? RIAC has asked Irina Timonina to give her expert point of view. Irina Timonina is a Dr.in and the Dean of International relations department at the Russian Presidential Academy of National Economy and Public Administration, professor of Institute of Asian and African States of Moscow State University (MSU).

Notwithstanding a quite ambitious economic plan of reforms initiated by the Prime Minister Shinzō Abe Sind known as “Abenomics”, mid-November 2014 has shown that Japanese economy is not getting better. The Prime Minister Abe has turned to extreme measures – dissolution of the parliament with the new elections set for December 2014. Once ranking among the top three most innovative and strongest economies, Japan has now been stagnating for several years. What underlies this recession? How long will it stay like this? What public measures can be anticipated in order to deal with the stagnation? RIAC has asked Irina Timonina to give her expert point of view. Irina Timonina is a Dr.in and the Dean of International relations department at the Russian Presidential Academy of National Economy and Public Administration, professor of Institute of Asian and African States of Moscow State University (MSU).

Why has there been a slump in the economy at this particular time? How significant is it?

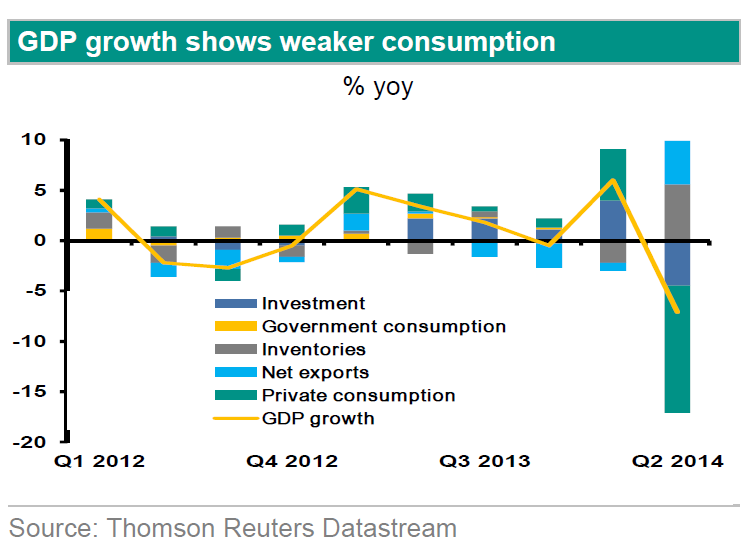

The results for the second quarter of the 2014 financial year (the financial year in Japan starts on 1 April) were quite worrying for the Japanese economy. The country’s economy effectively found itself in a position of technical recession after showing negative growth over the previous two quarters. Data from the Economic and Social Research Institute published on the website of the prime minister’s office showed that annual real GDP went down by 1.2% in the second quarter, domestic demand and household consumption expenditure fell by 1.5% and 2.8% respectively, and investment in housing construction fell by 12.3%. The deflator stood at 95.4% [1].

The trigger for this recession was the increase in consumption tax from 5% to 8% at the beginning of the current financial year. Japan’s prime minister Shinzo Abe, speaking at a press conference on 18 November 2014 after the publication of the statistics for the second quarter of the 2014 financial year, openly admitted the negative influence of this measure on the macroeconomic figures [2]. A few days earlier Ryuzo Miyao, a senior executive of the Bank of Japan and member of its Policy Board, had talked about the weakening of the Japanese economy caused by the fall in demand following the tax increase [3].

The consequences of such a fiscal measure could hardly have been a surprise for the country’s government. Parallels are inevitably being drawn with the situation in the mid-1990s, when at a time of certain upward trends during the prolonged recession in the last decade of the twentieth century the government also raised the consumption tax (from 3% to 5%) in order to resolve the problem of a growing budget deficit and debt, as a result of which the anticipated positive trends were cut back. The current tax rise, however, cannot be explained away as rashness or lack of foresight on the part of the government: it was a step that had to be taken to try to ease the problem of Japan’s huge national debt, which in relation to the country’s GDP is the biggest of any developed country (more than 230% of GDP). At the same time, the government probably reckoned that the possible negative impact of raising the tax would be offset by a growth in employment and incomes, but that did not happen.

The warning sign was the marked reduction in investment in housing construction. If we look again at the parallels with the 1990s, it’s worth recalling that during that recession it was the rate of investment in housing that supported the economic situation.

The reaction of economic agents to the current tax increase, which judging by the performance of economic indicators has proved to be quite unhealthy, was also caused by a number of factors in the external environment. Among these there is the general slowdown in growth rates in the global economy, including the Asian economies, and also the rise in the level of risk in foreign operations, due to the events in Ukraine and other issues. It is well known that the external market has always played a most important role in the Japanese economy and continues to do so, but in the last three years Japan has had a negative balance of trade. At the same time the rise of 7.4% in the annual growth rate of exports in the second quarter of the current financial year proved to be not enough to inject dynamism into the whole economy. Another factor that can be added to this is the weak growth in exports to the USA and China, which are critical markets for Japanese exports, and the continuing trend of moving production overseas, which is also a factor in the country’s ailing exports.

Thus it was probably a combination of negative trends in the domestic and external markets that caused a serious weakening on the demand side of economic growth.

What steps is Prime Minister Shinzo Abe’s government going to take?

At the 18 November 2014 press conference after publication of the statistics for the second quarter of the 2014 financial year Japan’s prime minister Shinzo Abe announced a decision to postpone the next increase in the rate of consumption tax (to 10%), previously planned for October 2015, until April 2017 [4].

We shall probably witness a seesaw effect, bearing in mind the change of priorities in favour of a further easing of monetary policy with the aim of reviving the economy. Shinzo Abe has proposed a new package of measures aimed primarily at small and medium business and the regions.

The Bank of Japan has raised the bar with its measures to buy back up to 80 trillion yen of government bonds against the previously planned 60–70 trillion and is ready to take a range of further measures to stimulate the economy, which include using pension fund money.

And of course, action to counter deflationary trends remains on the agenda.

When talking about the potential possibility of overcoming the recession in the Japanese economy, it is worth considering the following point. In the situation that has come about, is it possible in principle to shift the country’s economy onto a trajectory of sustainable growth on the basis of traditional stimulus measures, or should these still be preceded or at least accompanied by structural reforms, in particular those proposed in Shinzo Abe’s strategy?

What will be the priority areas of economic policy?

First Results of Abenomics: Growth and Social

Equality

It looks as though the strategic priorities of “Abeconomics” will continue. In any case Shinzo Abe speaks plainly about his intention to implement his strategy consistently over the next three years and marks its real achievements in terms of a rise in the level of employment and a growth in pay.

On the whole we should not expect Shinzo Abe to abandon his strategy or radically rethink it, at least before the next elections and before the data are available for the third quarter of the current financial year.

The Bank of Japan is placing its hopes on a revival in the global economy and a possible rise in exports of capital goods, electronic parts and components, and also an increase in the number of tourists coming to Japan, as well as on levelling out the current balance of trade by exporting services. In addition, the engine of growth will continue to be exports and investments by companies (which have remained just above the zero mark), especially investments in innovative development, although these have not secured a marked acceleration in GDP.

The fall in oil prices could also be a favourable factor, but if the downward trend continues it could become an additional deflationary factor for the Japanese economy.

Won’t the economic recession lead to a change in the Cabinet?

It’s impossible to predict, but the elections in December 2014 will probably determine the level of trust.

One thing can be said, however: Shinzo Abe is facing a dilemma (which governments of European countries have also run into): should he balance the budget or continue to stimulate economic growth, which would be accompanied by an easing of monetary policy and a rise in spending? It would seem that there is no best solution to this problem.

Incidentally, Abeconomics got a very positive rating from Nobel Prize winner Joseph Stiglitz, who wrote in 2013 that with his structural, monetary and fiscal policy Shinzo Abe had done what America should have done long ago. At the same time Joseph Stiglitz emphasised the importance of tax and budget incentives, believing that it is not national debt that is the cause of slow growth, but slow growth that has entailed an increased deficit [5].

Interview by Maria Gurova, programme assistant.

1. http://www.esri.go.jp/index-e.html

http://www.esri.cao.go.jp/en/sna/data/sokuhou/files/2014/qe143/gdemenuea.html

2. http://japan.kantei.go.jp/96_abe/statement/201411/1118kaiken.html

3. Economic Activity and Prices in Japan and Monetary Policy, Speech at a Meeting with Business Leaders in Nagasaki, Bank of Japan, 12 November 2014

4. http://japan.kantei.go.jp/96_abe/statement/201411/1118kaiken.html

5. Joseph E. Stiglitz, “Japan Is a Model, Not a Cautionary Tale,” New York Times, http://opinionator.blogs.nytimes.com/2013/06/09/japan-is-a-model-not-a-cautionary-tale/

(no votes) |

(0 votes) |