Oil and Gas Digest

In

Log in if you are already registered

Internet like Steam Engine, is a Technological Breakthrough that Changed the World

Peter Singer

Up to recently, I was sceptical about Singer's quote. As my economic background reminded me that the light bulb was more revolutionary for growth, and as I am quite a social person, I avoided too much online interaction; but my (belated) discovery of Twitter altered my views. I was never going to tweet about futile things like 'how good was my sandwich', but rather form it into a serious research and database tool. I also realised that I could share further, thus I am introducing my First RIAC Monthly Digest. My aim here is to recap, analyse, and offer links to top: Oil&Gas News, Pictures & Videos, from experts and institutions I follow. Also, please feel free to leave a comment below!

March's Top News:

- Xi Jinping... From Russia With Love:

Xi Jinping visit to Russia was highly symbolic, as is the case with first foreign visits (See: NTS). Energy was at the forefront of the visit with two different outcomes for the oil and gas talks. The other issue was geopolitics as the visit signalled that the world is changing by shifting West to East (See: Reuters). Xi argued that its "time to drop the Cold War mentality" as "no single nation or group can dominate world's affairs"; this could be just rhetoric, but it still aids to dispel some peoples worry that Russia's Chinese neighbour could be a threat, while also calling for the final end of USA's hegemony (See: SCMP). Albeit, it is hard to see China not taking the lead regionally and globally in the future as it clearly dominates, particularly in the BRICs (economically and politically). The days of it being the young brother of Russia, are unfortunately gone (See: TheDiplomat). With the recent BRICs summit, it seems that the vehicle for progress will be this institution, and it is 'not dead' as Western media believed (See: Global Research). It will be nevertheless vital that asymmetry is breached amid major BRIC players, in particularly, Russia will need to wield its natural resources carefully - not to end up feeding the dragon. Before entering the realm of energy, its important to point out that last Chinese leader, Hu Jintao, also came to Russia on a first state visit. Then no major deals were finalised and this had an impact on low expectation of this trip, particularly in respect to gas (See: MoscowTimes).

OIL: Xi Jinping considered the trip "a great success", as China was able to acquire natural resources it needed for its economic miracle, especially in respect to oil (See: BruneiTimes). Oil discussions were a success, as Rosneft and CNPC signed several agreements; including first ever Arctic joint-venture for an Asian country (See: Bloomberg). Alexander Novak, Russia's Energy Minister, said Rosneft will send an extra 2 million tonnes of oil to China along ESPO oil pipeline in 2014, and will gradually increase such shipments to 15 million tonnes by 2018; which is huge news for players involved (See: Interfax). Due to these deals China will overtake Germany as a top destination for Russian oil. USA and China currently both import around 6 million barrels of oil per day, with latter forecasted to overtake the long-time leader due to its booming transport sector (See: WashingtonTimes). If deal with Russia goes to plan, it should overtake the US oil consumption, particularly as it is still a developing country. Oil contract news come at the same time when China records huge increases in its proven domestic reserves, with 13% rise in oil, 33% rise in natural gas, and 24% in unconventional sources (shale, methane, or alike) (See: ECNS). Also, China's domestic production has increased by 1% in oil and 5.4% in gas in 2012 - albeit not a very impressive growth figure (See: ChinaSecuritiesJournal). Therefore, securing long-term deals for Russia is crucial to avoid competition from within China, but it also indicates that China is prepared to diversify its supply.

GAS: Xi Jinping visit did not generate outright deals, and it appeared that the mass media was right to dampen expectations towards only possible conclusions around the end of 2013 (See: FoxBusiness). The most recent negotiations have lasted since 2004, when Gazprom signed a cooperation deal with its Chinese counterpart for up to 68 bcm of gas (See: Bloomberg). This was a sizeable figure for China, as it is an emerging player in regards to this fuel type; although it currently adds up to a small portion of its overall energy mix, its growth has been very rapid. China has single-handedly fuelled more demand for LNG and expanded not only in its domestic, but also in international markets, like Africa (See: NYT). I was personally excited about opportunities between Russia and China, as Energy Minister Alexander Novak, issued a statement that both were working on gas and oil deals prior to Xi's arrival (See: Prime). I even hoped to discuss these issues with Novak personally, at "The Russian Energy Conference", which was run by Vedomosti Business Daily, but unfortunately due to the deal between Rosneft and TNK-BP, he could not go. During Xi's visit, it seemed that oil was clearly a more appealing energy source, as it is less politicised and China's desired price of $250 does not meet Russia's expectations of $300 per 1000 cubic meters (interestingly, the formers wish is very low, as Turkmen's gas goes to China at $345 before it crosses the boarder into China).

GAS: Post-Xi's visit developments suddenly picked up as it appears gas negotiations occured in the background outside public eye. Victor Zubkov, Chairman of Gazprom, issued a statement that a deal is due to be finalised in June (See: InterfaxEnergy). The gas deal is for 38 bcm of gas, which is less than anticipated 68 bcm and vitally price was not set, which is obviously a serious concern (See: InterFax Energy). Additionally, Russia was unable to play-off Europe against China, due to the latters pressure. Russia hoped to supply both markets with its European gas fields, thus making its customers compete against each other (See: Reuters). However, on the brightside Gazprom agreed with China in regards to long-term contracts, thus allowing it to develop the riskier fields as export was more guaranteed. At first, I was sceptical about the deal due to the lack of a solid price and as talks with China (depending on where one starts) stretch 45 years - making another Chelyabinsk asteroid more likely. My scepticism eased upon the news that Gazprom has green-lighted a major gas field in Siberia: Chayanada. As reported Gazprom's Chayanda produced gas will be delivered via the 3,200 kilometres long Yakutia-Khabarovsk-Vladivostok pipeline (see map below), with 61 bcm top capacity; the pipeline is scheduled for 2017 (See: OGE). Surely this must mean that the deals are serious and will be carried out. Also, it has been reported that Russo-Sino pipelines could be extended to India increasing Russia's regional reach (See: RussiaIndiaReport). Overall, it will be key that Russia agrees a good price for its gas, as my previous blog's discussed, as it cannot end up in a situation whereby it subsidies China.

- All Aboard Rosneft! TNK-BP Done Deal:

The deal between Rosneft, BP and AAR Consortium, for the acquisition of TNK-BP by the former party was completed on 21 March (See: RT). Speculation over the possible acquisition were ongoing for a very long time - with many anticipating a possible closing date around the end of 2013, or even a possible collapse of the deal. But, speculation proved fruitless as Rosneft acquired TNK-BP for a hefty sum of $55 billion (See: OGE). I was again unfortunate, not to speak with Alexander Novak, Minister of Energy, at "the Russian Energy Conference", due to this deal being done outside the public eye - as is the case in the world of energy. A mixed reaction can be said in regards to this deal. As, on the one hand, it only increases gigantomanic tendencies in Russia - as everything has to be big - but this is perhaps an overstatement as the government has indicated that it wishes to give more emphasis on small power generation (FedPress). However, it is difficult to ignore the words of Alexei Kudrin, who said that one inefficient giant is taking over an efficient company. Also, the deal gives ammunition to those who are against increasing state intervention; as the deal means that over 50% of the energy market is state run. On the other hand, the deal will allow Rosneft to integrate TNK-BP efficiency into its bigger system, thus possibly increasing efficiency overall. Also BP will be involved through direct positions on the board, so it may transfer efficiency from the actual BP parent company, which will want to see Rosneft succeed, as it will now own 19.75% stake in the Russian giant (2nd biggest after the Kremlin) (See: MoscowTimes).

Rosneft has now become the world's biggest oil company by surpassing Exxon Mobil, but only time will tell if the TNK-BP deal will benefit Russia. I doubt BP's seats on Rosneft's board will be purely honorary as some suggest, and I think they will influence development in Russia in a positive way. For instance, horizontal fracking will be introduced from BP's experience which will increase efficiency by allowing for rejuvenation of old-Soviet fields (See: Energy&Capital). Russia has used fracking for years in Siberian oil heartland to stimulate production, but with BP, it could alter it thanks to the shale revolution technology of turning the drill-bit 90° to bore horizontally that way reaching more bearing rock. Topic of efficiency will certainly remain "sexy" in energy dialogues, with Rosneft's (and other giants) ability to develop fields quickly being vital; as it reduces costs and the end price, thus ultimately making Russia fuels more competitive. For instance, Norway's state owned Statoil should be applauded, as it managed to find and efficiently develop the huge offshore Skuld Field (with life-cycle beyond 2030) in just three years (See: UPI). Therefore, state run firms do not have to be negatively looked upon. It is nevertheless important that this giant is guided into the right direction. It will be interesting to see how the relationship between Rosneft develops with the Russian government, as Gazprom has always been the state official and legal monopoly, but as the former's potential grows, particularly in gas, this status quo may alter. Currently, Ministry of Natural Resources backs Gazprom (See: InterfaxEnergy). Finally, whether the TNK-BP deal was led to this development or not, Exxon Mobil just issued an ambitious $190 billion exploration and development plan. US giant is known for being the market leader and trend setter, so its not surprising to see it leading the industry forward, but the figure is very substantial. It will add 1 million barrels of oil to its stock, which although not challenge Rosneft's huge oil production, nevertheless it will add more competition from a much more profitable US firm (See: Oil&Gas Journal or OGE).

- RIP el Comandante:

The death of Hugo Chavez, albeit not unexpected, has caused a mixed reaction. Naturally, the West was somewhat joyed, that the long thorn was gone, as Venezuela's leader was not popular in places like the US. In regards to energy, reactions were subdued as many expected the outcome with investments into Venezuela's $100 billion energy industry stopping in expectation that the highly personalised regime will not last much longer. Russia's input into the sector ranges around $22-$30 billion, some experts were at first worried that the country may turn Westwards, but this did not materialise as Nicolas Maduro as it appears even more socialist than Chavez (See: RBTH). Thus, the interim leader will not injure the cash-cow that supports millions of poor in Venezuela. Chavez's death was even discussed on the Russian radio, as Echo of Moscow had a special, with their experts agreeing that the country is too dependent on Russia to axe its participation. A more recent development subdued any fears further, as Rosneft and state owned PDVSA (Petróleos de Venezuela S.A.), have agreed to develop an oilfield with estimated reserves of 40 billion barrels (See: OGE), but eyes will be on the upcoming election which for the first time will no longer feature flamboyant Chavez.

| At first, Russia's Rosneft seemed to be the most vulnerable due to Chavez's death, as it hedged massive funds in developing Venezuela's energy sector; Igor Sechin, President of Rosneft, viewed it as number one foreign investment opportunity. He even famously wore a t-shirt with Chave'z picture as a sign of support, when the late leader was trying to fight against cancer (on the left).

Furthermore, China has invested huge financial resources into Venezuela, as China Development Bank sent $46.5 billion since 2008 in exchange for oil. Chavez was not the easiest person to deal with for China, but he was "their man", whom they could trust (See: Bloomberg). Interestingly, an inteview I've posted with an independent Russian oil producer touched upon working with the Chinese, apparently they are good colleagues (See: OGE). |

- Europe Gas Woes:

As much as Europe has attempted to look elsewhere for its energy needs, recent developments in Iraq have once again shown that the Middle East, Africa and South America are not as reliable as Russia - due to political risks, as well as, more technical issues like transport proximity. In Iraq, the dispute amid central government and Kurdistan has resulted in contracts being annulled with Exxon Mobil, Total and GazpromNeft; as the central government considers that only it should negotiate energy contracts, not its rebellious regions (See: Gulf Oil&Gas). As a result of anti-Russian import policy, Gazprom's European exports fell 7.5% (2011-12), with opportunities becoming more limited, but it appears that a 40 bcm potential to supply UK is still on the table; as the Russian giant only covers 10% of the island's market (See: Platts). Someone needs to remind Europe, that it made billions during the periods of the '90 and early 2000's when the long-term contracts benefited their economies, due to cheap prices, but now prices increased they tend to quickly forget the good old' days. Obviously, this is just rhetoric, as everyone always quickly forgets past benefits in business when trouble arises. This is why, Gazprom cannot simply continue going about in its slow and big way, as although the Russian state can protect it domestically, it can only do so to a limited extent abroad, particularly in more challenging EU markets (See: Economist); certainly if it ever wants to again reach the same peaks, when Miller talked that it will be the first $1 trillion company. What ever happens, Russia's companies must be quick, as time could potentially run out with alternative suppliers coming online quickly (See: Reuters)

In all, Europe continues to be an uncertain market. UK's urgency to form a hub market has led to issues for Russia, as its NBP hub (National Balancing Point Hub) influences European prices heavily against the more expensive pipelines. Althought, interestingly, UK's rush has recently backfired as it found it difficult to buy LNG due to prices being 2x higher in Asia, thus making UK an undesirable location for export of liquified gas for nations like Qatar (See: Reuters). This problem has intensified at the end of March as some deemed that the UK was close to running out of gas. Contrary to fears of some media outlets (See: Yahoo or See: TheTelegraph), this did not materialise as tankers from Qatar and Algeria arrived quicker than the two-weeks period expected. But, it does highlight that pipelines are much more secure, albeit more expensive. A recent agreement between UK and US is also a worry for Russia, but it is rather peculiar as the latter will supplier the former with shale gas from 2018 only as long as the Asian market will not be more appealing [it will be] (See: TheTelegraph). To add more misery, amazingly excessive instability in Iraq has not prevented it to expand its energy sector, as it has just issued a new plan to invest $130 billion over 5 years in developing its oil and gas fields (See: Zawya); production has already increased 24% last year, so the developments of its "giant" fields will be a big worry for Russia. Finally, on the positive side, although Turkmenistan has increased production of gas in 2013 - it has been relatively small at 3bcm, with also internal consumption growning quicker, which will lower exports to China, or potentially to the EU market (See: NaturalGasEurope). Also, political turmoil in Egypt could potentially shift it to be a net-importer with Russia dubbed as a potential supplier (See: VoiceofRussia). A lot will depends on Egyptian government as like with many countries energy imports are tightly regulated. Finally, it is a question whether Europe wants to play with its energy security as it needs to realise that investment in infrastructure is costly; it costs $100-150 million for LUKoil to drill one Arctic well for the EU (See: MoscowTimes) - as my readers may recall that is hugely more than setting up a traditional rig.

- Shale Revolution (Again...):

US shale developments are exciting as it marks a shift within the political mentality of the country. Post-WW2, US was redirected towards import of cheap energy from the global markets. It did so, after the "Paley Report" was published. Today, as energy is no longer cheap on the global markets, as well as, there are geopolitical worries, US has shifted towards more expensive, self-sufficiency. Some are still sceptical about exports, as two US House Representatives Ed Markey and Rush Holt aimed to push a new moratorium law to suspending shale oil and gas exports so US citizens, not MNC's or foreigners, benefit from shale (See: UPI). It remains to be seen, to what extent shale export will influence the domestic market - as some estimates of 2-11% by 2035 in increase of prices do not seem like a bad opportunity cost (See: InterFax). In all, international factors will play a role, as well as domestic, as recently earthquakes in Oklahoma provided more fuel for the anti-shale environmentalist lobby (See: BBC). A scary thought is, that earthquakes due to fracking can appears years after the actual process, due to a delayed reaction from the ground movements - considering the scale of fracking in the US, we could see more.

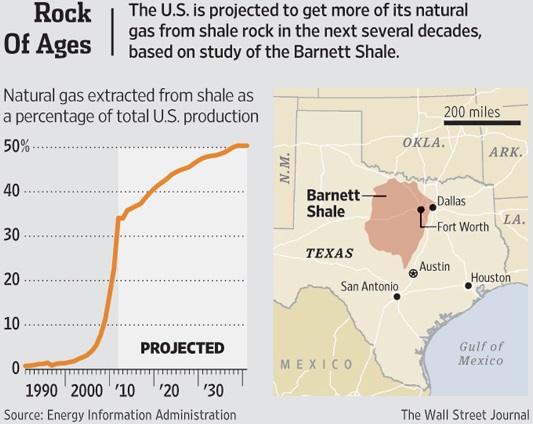

Export wise, New York Times had several times stated that the Shale Revolution has resulted in shale now accounting for 34% of the energy mix, from 1% in 2000, and with possible 43% by 2015; by 2035 it will be a bigger gas producer than Russia at 60%. Wall Street Journal has supported this view as it sees shale gas going for "decades" with acceleration in production (See: WSJ) However, with shale nothing is solid, news or the rock foundation after fracking, as other sources report that the revolution will plateau and fall by 5% from 2010-2040 (Exxon Mobil Estimates See: ChinaTimes). A positive sign is that Fitch Rating Agency does not expect US shale to impact Asian markets in the medium-term which is good for Russia and that domestic reforms currently in motion in China will also not alter the playing surface. Russia needs to secure energy contracts, but it seems time is still there (See: ShanghaiDaily). Interestingly, even with spectacular growth rates of shale production in the USA, its has had relatively small indirect impact on global prices - as many anticipated. For instance, it has not helped Japan, as the fledgling economy has seen prices explode by 77% since January 2011, with a total of 7% of GDP going to import of energy (See: CNBC). Japan’s interest in US exports has soared, but so far there are few opportunities as out of the 17 projects that have applied for a permit to export LNG to countries "without a free-trade agreement with the US", only one (Cheniere Energy’s Sabine Pass Louisiana) has been awarded the right (See: FinancialTimes).

For Russia and other traditional natural gas exporters, US reluctance to export is helping, but to repeat this may not be for long (See: Energy Tribune). On the bright side, signs have emerged that Russia may cut export duties to lower the price of oil (which faces competition from shale oil), so they country can meet Vladimir Putin's goal of 10 million barrels of oil a day (See: BusinessWeek). In regards to gas, as the Vedemosti conference pointed out, Russian duties of natural products are among, if not the highest in the world, which will need to become more competitive so newer fields can be developed. Of course this is a politicised issue as it will mean that less federal revenues will be collected and fewer socio-economic projects can be launched - question is can a right balance be achieved? The problem is that Russia's internal market prices are overpriced, a lot more than in the US and almost as much as in the net-importer Belgium (traditionally high priced area). The tax system is an area that will need a lot of attention (See: ArcticGas), particularly in more expensive areas to excavate, like the Yamal Peninsula; it is estimated that Gazprom will need to invest in a region of $100 billion to bring the area online.

In regards to other nations. A great article is produced by Bloomberg, which talks about extremely high ambitions of China in regards to shale. China is producing no commercial quantities of shale gas, yet has set a target of 80 billion cubic meters by 2020, or 23 percent of total expected demand. Output in 2020 will likely be 18 billion cubic meters, according to the average estimate of seven analysts surveyed by Bloomberg. That’s more pessimistic than a year ago when the forecast was 23 billion cubic meters. China has failed to attract enough interest in shale through auctions, with low subsidies partly being to blame, as an initial kick-start is needed (as with most projects in the energy game). Also, China lacks technology for shale production and its energy companies are not experienced with new innovative drives like shale. It is a great article, with three interviews from top experts. But, China's shale strategy is not only domestic, but international, as recent announcement to invest $40 billion into US shale was quite surprising. It has already apparently invested $1.52 billion into US shale, with an aim to increase its global oil production to 200 million tonnes by 2015 - very ambitions (See: RT). China has also pushed to invest into natural gas-stations for transport vehicles in the USA, as by switching from oil to gas reduces pollution (See: ChinaEN). One wonders, if China this way wants to get closer to US shale technology, as one must point out that the US has been highly reclusive of it, not even allowing Chinese passport holders to its production sites. For the time being, Russia will play a crucial role in aiding China in reducing its CO2 print and the two will remain close partners as proximity politically and geographically makes sense (See: ChinaDaily).

As a side note, interestingly, IMF has critically stressed that subsidies should fully end, as governments globally spend $1.9 trillion on subsidising the energy sector - with US being the biggest culprit overall, but more socialist leaning countries percentage wise (See: WashingtonPost).

Blockbuster Section:

- RITEK VIDEO (Russian Innovation Technological Energy Company): I was originally introduced to this exciting company by Gennady Schmal, President of Union of Oil & Gas Producers of Russia. This is a flagship company, parent company LUKoil, that focuses on innovation in Russia. Its exciting because it has made substantial progress in recent years in innovation and companies like this, are and will be at the forefront of innovation in Russia. As innovation or R&D, is usually not done by major energy players, it is the role of specialised innovation companies like this one to provide the forefrong progress. In more developed markets, like the US, there is a selection of firms, including Schlumberger Ltd, Halliburton Company, Emerson Process Management, etc. So it is exciting to see a Russian player growing from the domestic market. This video not only goes into the legal and formal structure of the company, but has very neat graphical illustrations how oil and gas is excavated - particularly in hard to reach places or in old fields - which will become ever more important as traditional ex-USSR fields in Russia decline. Gennady Schmal said that Russia spends only 0.86% on research and development, which is sizeably lower than the competition, but we should not underestimate the innovative nature of the oil & gas sector in the world and Russia.

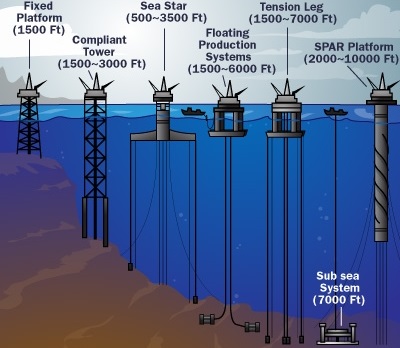

- Grup Servicii Petroliere Akcakoca Project Video: I found this video while doing research for my work piece on innovation, although it ended up having little to do with actual innovation, it nevertheless, shows the mamonth task of how 1500 tonnes and 7km cable is laid when building an offshore 'fixed platform'. Its quite 'discovery channel' like; also the image below illustrates the different types of offshore platforms to get a better understanding - offshore platforms can become almost like floating cities, but sadly, they are not undestructable as hurricanes and other weather conditions remain a serious threat:

- Cuadrilla Resources Video: The development of the UK energy market will play a crucial role for EU's gas and oil prices. Firstly, UK is a major energy consumer and its current gas and oil reserves are very quickly running out - contrary to what Scottish National Party believes - which means that unless it developes it shale potential, or finds alternative sources of domestic energy it may well soon become a major importer. Secondly, the UK is home to the most important hub in Europe, the NBP Hub (National Balancing Point), which influences all other European hubs in their pricing, which ultimately influences the price traditional suppliers like Russia and Algeria can get for their energy resources. This video is by Cuadrilla Resourcers company, a reletavily new firm focusing on shale production, it has recently hit the news due to earthquakes hitting Blackpool, after shale was produced, resulting in temporary suspension of shale production in the UK. However, this video aims to highlight now somewhat ironically how to safely produce shale - interestingly UK uses far fewer chemicals to erode shale layers (as my last blog explained), than the US.

Gallery Section:

- "World’s Richest Countries by Oil & Gas Reserves" 'InfoGraphic' by RIA Novosti. In Russia, per capita, each person holds $164,580 of fossil fuel wealth, with our overall oil and gas wealth being estimated at a huge $23.5 trillion, just below Venezuela, Saudi Arabia and Iran, due to their much bigger oil reserves (See: RIA Novosti)

- "Crude Price Roll-Over Graph + Major Events" (1998-2011) (See: Guardian).

Igor Ossipov

Oil & Gas Eurasia Correspondent, Oil/Diesel Broker and RIAC Blogger.