Route-2030

In

Log in if you are already registered

"There is nothing more difficult to take in hand or more perilous to conduct… than to take the lead in the introduction of a new order of things."

– Niccolò Machiavelli

Machiavelli's quote stresses three things. Firstly, it underlines that any new route will likely be perilous. Secondly, it highlights that someone must take the responsibility to direct the nation's path. Lastly, it grants me the chance to include Machiavelli into my blog; for those that know me, would quickly recall my keen interest in the Renaissance's jack of all trades. However, on a serious note,

Personal Note: I should have uploaded this particular post on RIAC from the start to make the Blog more chronological However, its better late than never! I adopt a similar framework to my last posts with direct links to all the sources, for easy access, as this is a blog and it doesn't require academic rigour. Please see the following link for the Energy Policy journal article on which this post builds upon: "Oil & Natural Gas in Russia's Eastern Energy Strategy: Dream or Reality. Also, please feel free to comment or leave a like, its always more productive to engage in a discussion!

Route 2030: Dream or Reality?

The rising politicization of Euro-Russian energy relations is casting doubt over future volumes of oil and gas supply to Europe, according to two researchers from Masaryk University. Their recent article evaluates the difference between policy ambitions shown by Russia and the official “Energy Strategy to 2030” (ES-2030) publication; released in 2009. M. Mareš and M. Laryš argue that China’s rise is creating a great opportunity for Russia as an extra energy market, but at the same time, current conditions could quickly alter into economic as well as political risks. Both countries want to make sure that their interests prevail, which causes stumbling blocs like price formula renegotiations or substitute suppliers: be it from Turkmenistan and Burma, or internally from China's shale gas.

The reason behind China’s appeal to energy exporters is its booming economy, which requires disproportionate amounts of energy: to create $1 of GDP China uses 5 times more energy than the US, or 12 more than Japan. Just by 2015 China’s consumption will near EU’s at 490 Mt. ES-2030 shows that by 2030 Russia aims to supply 20-25% of Asia’s oil from the current 6% – with China being the main consumer. Further, by 2020-2022 the figure should be around 14-15%. Gas wise, it is amazing that Russia, the energy superpower, sells no pipeline gas to Asia, and only marginally sells LNG from 2009. By 2020-2022 Russia ambitiously aims to reverse this trend by supplying 16-17% of Asia’s gas – with the figure rising to 19-20% by 2030. In all, this shows a positive trend as Russia must diversify its eggs among more than one basket. Its main European market accounts for 90% of its export – which is a serious security issue.

ES-2030 is quite versatile with internal ambitions as well as export intentions. Russia aims to integrate its export capacity into developing political and economic solutions for the regions. However, it is facing constraints like population decline and organized crime. But on the bright-side the former problem is improving as Russia has begun to break the continuous declining trend, which plagued it for two decades. Demographic revival in Eastern Siberia and the Far East will be vital as the sparsely populated regions will need to develop their own internal energy markets to reduce the pressure from initially expensive exports – fixed costs will need to spread. ES-2030 aims to do this by institutional methods (e.g. changing the legal system) and FDI, which will rise to around 12% of the overall Russian total. As a result, proven oil reserves will rise by 10-13 billion tonnes and gas will rise by 16 trillion cubic meters.

![]()

Problems with Heading East:

The East Siberian and Far East regions hold about ¼ of Russia’s oil and gas proven reserves, but these regions are extremely underdeveloped making casing, extraction and transport difficult. Key gas fields, like Kovykta, are isolated by taiga or encircled by canyons – these are not Gazprom friendly areas due to a lack of piping expertise. Besides technical issues, political factors have also strained development. Like the 10 year dispute amid TNK-BP, Interros, Gazprom and other stakeholders, but a light at the end of the tunnel seems nearer as Russian politicians have stepped into to resolve some of the issues. Also, TNK-BP acquisition by Rosneft naturally resolves some of the long-lasting disputes. As the below map illustrates the extent of underdevelopment is quite obvious, particularly if compared to the European part of Russia. It is not surprising, since USSR and China have fell into hostilities during the 1960s and only reached a detente by 1980s - due to this major pipeline projects and joint cooperation was simply out of the question. This does leave a question to ponder in my next posts as how will history influence energy relations amid the two giants.

Japan has indicated that it may partake in Kovykta ("3" on map) if its status is reaffirmed, due to its importance for the Asian market. In 2012, Interfax reported that Gazprom’s CEO, Alexei Miller, has launched a plan for “a pipeline from Kovykta… towards Chayanda and, in the end, gas from Kovykta will be transported through the Yakutia-Khabarovsk-Vladivostok gas pipeline… [it’s] slated for 2016”. In February 2013, ITAR-TASS reported that Gazprom has started to consider bringing forward the 2016 aim – so has the Russian energy elite realised the need to hurry? Mareš and Laryš would caution, as the dynamic diversification into Asia is somewhat abandoning the traditionally lucrative European market, than actually providing additional customers. Nevertheless, Russia must not take too long as the energy sector moves quickly and it could find the Asian market saturated.

Winding Road Ahead - Oil:

ES-2030 success will depend on the interactions between the Russian energy elite and politicians, who tend to interrelate greatly, especially at the top. The Pacific Ocean Oil Pipeline (ESPO) is even viewed by some experts as a personal aim of Russia’s current president. The central factor behind ES-2030 and ESPO’s success will be the Vankor Oil Field and its interrelation with subsidies and taxation. Rosneft cunningly managed to reclassify its geographic location as an Eastern Siberian oilfield, which initially resulted in zero and then little taxation; plus $4-5 billion subsidies. Geographically it is not in the eastern sphere, but this was not unnoticed as a fierce lobby battle ensues over its favourable taxation status. Mareš and Laryš argue that if Vankor or other fields lose their battles, they will not be able to raise output or develop. Both direct and indirect assistance is vital to cash-flow as most of these fields are situated in environmentally harsh and remote places. But, on a positive note there is a domino-effect present as by developing larger fields and their infrastructure will push smaller fields online. Vankor should hit its peak around 2014 with an output of 45 Mt. If my readers recall, I did a post on 2035 global forecast, the new forecast has just been released called the "Global and Russian Energy Outlook 2040" - this report argues that taxation will be vital in determening Russian path as really high taxes on energy currently make our resources uncompetitive in the global markets. However, its a highly political matter as taxes pay for services and social support, which cannot be easily altered.

The recent contract with China looks hopeful as Russia is getting a unique deal with a $25 billion loan for the ESPO pipeline. Under this contact, interest rates given are half the price of the ones available on the world market. However, the ESPO is not trouble free. Konstantin Simonov, the Head of the National Energy Security Fund, argues that the ESPO is too ambitious with the goal to increase oil transit to 50 Mt by 2015 and by 70-80 Mt in 2025 being unlikely. As even by official data by 2030, Eastern Siberia cannot produce more than 700 Mt from its 3000 Mt total, whereas 2500 Mt is needed – one must also keep in mind that estimates foresee new fields being opened in 2016 which may not occur. ESPO’s full output will never be reached as only about 50-80 Mt will be available; also it is only economically viable to use pipes instead of rail if over 50 Mt is shifted. Political dialogue with China and the end price (which is a trade secret) will determine the result; it is estimated that the sum is about $60 per barrel for Urals oil – surely one must question the validity of the win-win situation at that price? However, more recently, things appear to have moved in a more positive manner as Rosneft and CNPC deal to increase supplies via ESPO have a higher reported price and the deals post Xi Jinping visit show that China is interested.

Uneasy Passengers – Gas:

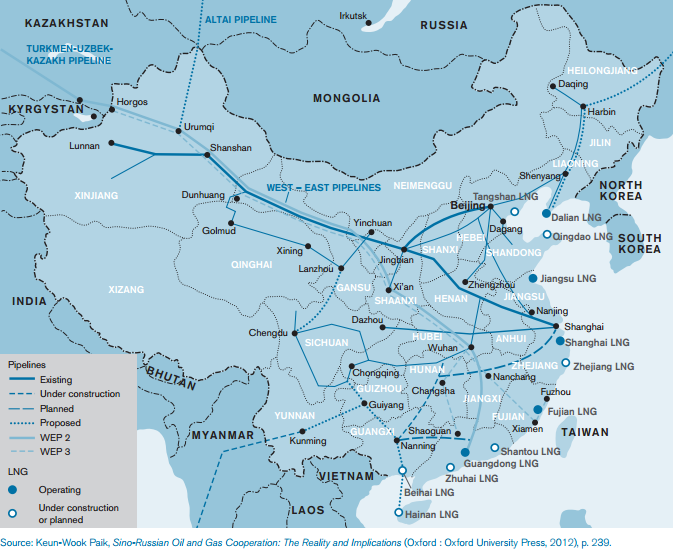

China’s feat of securing Urals oil for half the market price and being a peculiar victor amid the taxation squabble in Vankor highlights its shrewdness. However, its constant desire to change the pricing formula and its outstanding oil debts, go into the territory of poor relations; which will aggravate Moscow. Gas wise, China again acts as a hard client as experts believe that it links gas to coal prices, which differ a lot, particularly when Russia aims to receive European type sums. Mareš and Laryš argue that China’s gas market is a questionable venture, as it is traditionally orientated towards coal with gas only account for 3% of the energy mix. China has begun to move towards natural gas only 10 years ago. It is estimated that the overall total will rise to around 10% by 2020, but with increasing competition and Beijing’s strategy of diversifying imports as much as possible, it is uncertain how far Russia can penetrate the market. Unfortunately, its not all down to the exporter, as China's willingness to provide finance both to Russia for expensive projects and to its own companies will make, or break the deals. It vital for both importer and exporter to be ready, but neither yet are as the internal gas sector in China is still underdeveloped whilst Russia lacks investment and guarantees of import. Picture below illustrates the extent of underdevelopment and also that majority of infrastructure is located in the wealthier coastline part of China, away from Russian supplies which will increase their price and make Beijing less willing; unless it really pushes to diversify into gas.

China’s unconventional resources over the recent years further fuelled uncertainty, as it has equally huge reserves of shale gas (biggest in the world) and coalbed methane, and large reserves of tight sand gas. It has planned originally to extract the former in 2015, but in good news for natural gas exporters, this is unlikely to happen as over the last year shale prospects have plummeted. China’s reluctance to introduce free market mechanisms into the sector is credited as one of the main causes. Bloomberg reports that the original shale gas goal “of 80 billion cubic meters by 2020, or 23 percent of total expected demand” now appears like a far off dream. Recently, China has even hinted at increasing cooperation in developing of new fields, geological prospecting, extraction and building with Russia which could indicate a new trend.

Mareš and Laryš argue it makes no sense for Russia to supply China for the sake of a market share. In fact, it is damaging to supply it in the same fashion as Turkmenistan, which takes a huge dent in the federal budget by selling gas at half the market price. Russia has currently played its cards well, as fears of Turkmen market takeover did not materialise, but only time can tell about the possible effects of Australian, Omani, Nigerian, Egyptian, and Qatari imports. All 4 projects aimed at supplying China have not materialised even though discussions have been ongoing since 2006-2007, but it is only a matter of time before a deal is concluded as China is naturally the biggest client and Russia is the largest supplier. Talks have intensified as Gazprom realises it cannot wait forever and it even requested a 40% upfront payment by China for gasification.

At the time Mareš and Laryš wrote their article it looked like Russia had several options, like supplying China, Japan, the Korean Peninsula and even as far as India. Then it was mainly Gazprom’s modest LNG expertise that limited sizeable deliveries in the near future to the heavily LNG focused Asian states. But still, Gazprom made good progress by shifting 9% of Japanese LNG and 7% of its oil in 2011 to Asia. Vladivostok LNG terminal, due for launch in 2017, will increase capacity matching the rising demand, particularly as recent events have benefited Russia (e.g. Fukushima Disaster). However, the talk about North Korea becoming a "transit state" have been completely dashed recently. It seems that Kim Jong-un was not tempted to receive $100 million in annual transit fees - which would probably go to him more or less personally due to the nature of such authoritarian states. It was always very optimistic to even consider this option, but energy companies and academics nevertheless did not abandon the possibility that it could become a reliable partner for South Korea gas needs. Perhaps, in the perfect world, where the last delegate to DPRK is not Denis Rodman and it does not want to destroy USA, both South and North could cooperate in all fields, including energy matters.

At a junction – ES-2030:

ES-2030 follows a tradition of Russia’s psychological affection to large scale projects with political elites at the helm. It offers opportunities, but Russia must place its interests first and not enter the market for the sake of involvement, as its policies will make it hard to turn back. However, at the same time, it is difficult to imagine what else Russia can currently do. It could remain in the European market by doing what EU has set it out to do, which will not only conflict with national interests, but also not help it develop in the long-term. As the EU policy of anti-monopolization and liberalization which leads to lower energy prices, will not allow Russia to develop its new expensive fields. The China route is somewhat more straighforward, as at least China does not want to re-work the whole Russian energy industry. But the problem is that China holds the upper-hand as it realises Russia has little room to manoeuvre. It will be vital to attract additional players, most likely Japan, but as Mareš and Laryš highlight ES-2030 offers little concrete facts and mainly shows a roadmap with some directions. It will be decisive that who ever takes Russia into whichever direction, will have the right license and will not be dreaming behind the wheel as this could be the most important decision in post-USSR, Russian history.

Igor Ossipov

M.A. Higher School of Economics, Oil/Diesel Broker and RIAC Blogger.