Wary Bear and Shrewd Dragon

In

Log in if you are already registered

"Quand la Chine s'éveillera, le monde tremblera"

Napoleon Bonaparte

The awakening of this old sleeping giant, or more accurately its re-awakening, has led much ink to be spilled and many keys to be worn-down. For many, this phenomenon was of great interest naturally due to China’s huge size and its equally large potential; especially, in contrast to the economically and politically stagnating West. However, for Russia, this re-emergence plays an exceptional role which stirs much uncertainty and mistrust, as once this giant wipes of the rheum around its eyes and springs back full of energy, its only natural room to manoeuvre seems northwards. Even if the world does not tremble, Russia fears that at the least Eurasia will shake. As promised, this is the second post in this special series and once again I am joined by the Head of Oil and Gas at the Energy Research Institute of the Russian Academy of Sciences, Dr. Tatiana Mitrova. We discuss: sinicisation, geopolitical mistrust, energy deals, the Central Asian Ace & more! Please, feel free to comment & enjoy!

Personal Note:

This is the second post in a two-part special with one of the leading Russian experts on energy matters, Dr. Tatiana Mitrova. To view the first part of this series focusing on the European-Russian relations, click the following link: European Energy Woes. Moreover, for those that follow my blog, as promised in one of my earliest post's, I ask Mitrova about the validity of Mikhail Krutikhin's (leading Russian energy critic) standpoint on the possibility of subsidising the Chinese consumers with Russian gas.

Sinicisation of East Siberia and the Far East:

In the minds of many Russians a deep sociological fear exists of a Siberian takeover by China, either indirectly via immigration/demographic asymmetry, or directly by an invasion. In a former more plausible case, many can recount the relative ease with which China was able to repel those that tried to conquer it, not via warfare or guerrilla resistance, but by Sinicisation as its sheer cultural dominance and hugely asymmetrical population swept in any aggressors, as well as, regional players nearby. Even in the latter less realistic scenario (due to nuclear capabilities of all major powers), the Sino-Soviet border conflict of 1969 (Damansky Island) lingers in the minds of many, particularly as it is relatively recent in historical terms. The fear is naturally greater in areas closer to China, in some there is nearly a hysterical feeling that East Siberia could secede to the awakening dragon as demographic, cultural and socio-economic shifts accelerate as Asia moves towards becoming the world's new engine in the 21st century.

In one of Siberia’s largest cities, Irkutsk (Mitrova’s birthplace), sociological fear is particularly intense. A large portion of its population grew up under a constant threat from the next door neighbour. As Mitrova tensely recalls from her childhood, the Chinese radio transmitters send shivers down the backs of many Irkutsk'vites as they profoundly announced across the boarders: “good morning citizens of temporarily breakaway Chinese lands!” Moreover, in schools, children's little suitcases were pre-packed in case of an emergency evacuation due to an unexpected Chinese invasion. Everyone knew the well rehearsed evacuation plan with parents going in one direction, whilst children would be moved quickly from schools to the railway station which headed away from the boarder regions. Considering that Irkutsk is quite far away from the direct Chinese boarder, it highlights the immense level of hysteria and also the fact that Mongolia is a futile buffer between the two great powers. It seems, the events around Damansky Island (in Chinese: ‘Zhenbao Island’ or the ‘Rare-Treasure Island’) have left a bitter aftertaste on the tongues of many, which soured future relations for decades to come. Even though this tiny island's legal ownership was transferred to China after an agreement between PRC and then still USSR, in early 1990s, tensions still persist in the region following the blooded dispute.

The Quite Chinese Expansion:

China does not behave like a militarily expansionist state, with it becoming increasingly popular in I.R. to brand it as a 'defensive neo-realist' (even though this term was previously reserved only for democratic states), but as Mitrova sees, it uses and will continue to use a method of creeping economic incursion in areas it considers to be of national interest (e.g. Central Asia as discussed below). Jubilations aside, this is still worrisome, however, this incursion exemplifies more the Russia’s weakness of not being able to develop Siberia on its own, rather than the strength of a spring dragon. East Siberia and the Far East must receive more attention from the federal bodies as otherwise it will naturally move towards a more powerful centre, even if the Chinese do not intend for this. If an area becomes noosed by another power economically, political sovereignty will also over time lose its meaning. It is not the case now in Russia and will not be the case in the near future, but it is something to be closely monitored. However, Russia is notoriously bad at monitoring, at least officially, with worryingly such areas like East Siberia and the Far East being constantly ranked as the least well performing in this regard. For instance, RIA-Novosti Website ranks the 'Ministry for Far East Development' 32nd out 32 in the rating of the most transparent federal bodies/institutions, with by far the lowest rating of 3.74 out of 10, in contrast to the generally low overall average of 5.3. In a humorous yet sour manner, the Ministry of Emergency Situations (МЧС) ranks highest with 6.83 points, which is more than a digit higher than the official state statistic bureau (Росстат), which ranks only in the 7th place, at this pace of transparency 'emergency' may well become ever more prevalent and possibly quite unanticipated.

That said, at the moment Russia cannot even carry out construction work without foreign participation in these vast regions, due to a lack of population and cheap labour; Russian nationals just cannot compete price-wise with near inhospitable wages certain groups of workers get, predominantly from Central Asia. The groundbreaking ESPO oil pipeline was also in fact built by the Chinese workers with no Russians at ground level as Mitrova highlights in our dialogue. In the process of completing my thesis I've personally stumbled onto an academic article published in 1991 by a Chinese scholar Hao Yufan; in this article he stressed that Russia must welcome 80 million Chinese labourers into East Siberia and the Far East to develop the region as it cannot do this alone. It is true that Russia cannot accomplish this task by itself, due to huge financial investments and labour demands, but welcoming a labour group that Hao believes is needed, which equates to the size of entire Germany, with impossible guarantees of their subsequent return home after the work is done (not to mention the impossible cultural reversal as they will also bring their customs) is a frightening notion. In all it is peculiar as Russia continuous to be cautious with China by attempting to enforce measures to limit immigration into the region from China, but at the same time it needs this labour, which results in highly dysfunctional relations with its neighbour that some see as crooked logic. The main problem which exists between the two is mistrust as Russia to a degree fears China's rise, whereas the latter does not fear the former, but it does not know what the former actually wants. It has always been historically difficult to gauge what Russia wanted and in which direction it was heading, hence it being a riddle wrapped up in an enigma as many infamously viewed it. However, the combination of Russia and China results in an unprecedented regional Rubik’s cube, except no colour is the same and the two players are colour-blind with suspicion and a long history of flip-flopping between sides (e.g. China's Détente with USA, Russia's Détente with USA etc).

Power Triangle - Sino-Russian Mutuality on US:

The first and foremost issue that Russia and China can find a common ground on, as Mitrova sees, is the joint dislike of the US hegemony. It is a big factor as essentially the two can be at least close, or in favourable circumstances, even be allies. In a crude or cliché way, foe of your foe, is your friend. Hence, to no surprise at the start of 2013's visit to Moscow China's Xi Jinping said that it is “time to drop the Cold War mentality” and create a new multipolar order, which directly undermines USA’s hegemony and Barack Obama's statements that China will be more than welcomed into the world community as long as it plays by the rules (which are naturally formed by the hegemon). As US is becoming increasingly concerned with rise of China, it is perhaps only a matter of time before we will see more tensions, with the great power struggle always resulting in sides being chosen. For instance, by simply picking up an issue of Foreign Policy highlights USA’s own uncertainties and fears, as an abundance of neo-realists scream for China's containment via ‘offshore-balancing’ (e.g. Walt, Mearsheimer, Layne, Posen & many others). It is a matter of time, because a strong neo-conservative base will re-emerge in the US, as it always cyclically does, which will be more confrontational in contrast to the more diplomatic approach under a cash-strapped Obama - who typically for a Democrat was left with a unmanaged financial jungle of the preceding Republic government and thus a limited foreign policy. Please, have a look at my recent interview with the top European expert, Prof. Richard Sakwa, for more detail: Setting the Temperature.

Russia would not want to lose the chance to limit the US or miss the train of international politics as it always considered itself a major global power. Hence, the terms of Sino-Russian relations will be key in the forthcoming decades. At the moment relations are difficult partially due to asymmetry, as although the latter can be an important ally in blocking or pushing through certain decisions (e.g. via UN), the former can still accumulate enough weight on its own to be on equal grounds with the US. Only time will tell whether we will see a closer geostrategic alliance amid the two, as one wonders whether USA will sit idle and allow China to replace it as the premier world economy. Its difficult to imagine this being the case as the whole US model is based on the ideal of being number one, thus one anticipates that tensions will increase once the US regains its economic footing and will be more confrontational to China in the bid to preserve its hegemonic status. At this point Russia's role may well increase as China will not be able to counter-balance the US and its allies alone. At the moment, relations between China and Russia are still slow even in areas like energy, which should be thriving. To put it crudely, former is a global sweatshop, whilst the latter is the energy pantry, so both technically need each other. However, the Trans-Asian Energy System (TAES) or Energy Cooperation System has been in essence buried by 'pseudo-bureaucraticism', as Mitrova puts it, as Russia feels that its Asian counterpart will gain relatively more. International Relations is not a team sport as any teams change quickly and mistrust is common, so although we may see closer relations between China and Russia in the future, right now the linkages are weak. In essence, Russia does not accept the ‘young brother’ role, which as Mitrova argues, is its realistic position due to its currently weak economic stature. Russian diplomats simply cannot communicate on unequal grounds as they have a strong complex of representing a great power, thus taking a secondary role after China goes against their principles. This is why, distribution of economic capabilities in the near future will be vital as unless asymmetry is lessened, this relationship may not get very far, as asymmetry breeds conflict.

Counter-Agent Dilemma & Subsidized Gas/Oil to China:

The publicised and agreed energy deals with China are currently at the break-even point or just above it, which comparatively puts them on par with expensive Australian projects. If the market conditions do not worsen, these projects will recuperate their costs, but if there is a shift in the business climate and/or price mechanisms it could have a detrimental impact. If we see a change in US/Canadian exports, North African export and Australian export, then it could create excessive oversupply and make these projects the most expensive in the world and in turn not very desirable for China or alike – as Mitrova highlights it is already the case with some Australian projects (e.g. Orgone). Also, as the next several decades will most certainly be driven by China, which has quickly abandoned the bicycle in favour of a car, both in a cultural and physically sense (as it is now the biggest car market in the world), events here will be vital. In selected large Chinese cities, as part of a special test program, re-structuring of gas and oil markets (in all stream areas) is already taking place, which is due to be concluded in the next several years. It will be a vital event as the system these cities adopt will have a huge impact on global energy landscape if it is applied nationwide.

In contrast to what some Russian and Western experts tend to constantly do, we ought to talk about high risks, rather than obsessing that these projects are outright uneconomical. Russian new projects for Asia are very risky, but they are not build for the sake of building supply with inevitable subsidies. Yes, they are political in nature, as Russia must diversify its overdependence on Europe that has increasingly become a difficult partner and they are rational. Almost every single top expert agrees that Russia's push for Asia is rational as it cannot put all its eggs in one basket. For example, at the most recent IMEMO RAN conference which I attended, the 'superstar' energy expert Daniel Yergin has reiterated this fact numerous times. Thus, the rational thing to do would be to reduce costs as much as possible to increase competitiveness of Russian gas and oil – for instance, the taxation system needs a lot of attention as it is a very heavy burden on the energy industry. The current tax burden of 73% per barrel is unlikely to increase, but it is very high, in contrast the USA's 44% out of each barrel sold. In the UK a dual system exist with a portion of tax going to old oil/gas wells to maintain their production levels which seems very rational and perhaps a case to look into, but vitally this cumulative tax rate is still a lot less than in Russia at around 60%. The problem for Russia is that the oil and gas industry is heavily interlinked with the government's budgets so any reductions in taxes for the energy industry results in lower spending in education or health care, which means it is an opportunity cost whether to improve peoples lives today or the energy industry, which will ultimately supply the nation with future taxes and thus future generations. As the International Energy Agency (IEA) outlines the financial burden is huge, around $100 billion or ~7% of annual GDP, but it appears there is no choice, which is why this money must be injected in a way that creates a multiplying effect for the rest of economy. Mitrova believes that we will see the returns from East Siberian and Far East investment in only around 15-20 years, which makes this commitment difficult now for economic and vitally political reasons, but it is imperative if Russia is serious about maintaining the hold of the region and up keeping its production levels.

In a snapshot, Mitrova says that she does not agree with the view of subsidies as some critics portray. Russia will not end up building pipelines and then be forced to sell gas or oil at a loss which will mean that Russian tax payers will need to take the brunt. In fact, the recent oil deal with China was a fair agreement, it can even be said that Russia actually gained more as even the interest rates were favourable for the loans it acquired to complete these long term contracts, as these rates were much lower than the global average. Hence, there are no evident serious pitfalls of national interests in Mitrova's eyes, however future oil deals will likely to be less favourable for Russia as China will use its dominant position of being the main importer to gain favourable prices. Still, it is unlikely that China will push Russia to a level where it will not break-even as this will tater relations, but as we know its almost certain that if gas-pipelines are build then China will renegotiate the price to a lower level. In essence, it is an issue of counter-agent dilemma as the buyer is usually always at the winning end in contrast to the seller, as fixed assets like pipelines cannot be re-diverted in case of disagreements over price. Hence, if in the future Russia does not agree with potential Chinese demands it will be left with no options, but China will be able to get gas in Central Asia or via the sea from Australia and maybe even the USA post 2016-2017 when many anticipate possible start to shale-LNG shipping. Lastly, China can always burn coal if it is facing a trade dispute over price to pressure sellers like Russia, although as Yergin highlighted at IMEMO RAN the environmental fallout from coal is now among the leading energy issues as it has gone too far and cannot be used so excessively (2/3rd of primary energy mix right now).

China's Main Energy Sources & Central Asian 'Ace of Spades':

The main energy source for China will be domestic production, with coal still accounting for the largest share even though its environmentally damaging as underlined. In terms of import, China conducts a very careful and rational policy of enegy diversification, if we look at their oil and gas contracts and where they are from, they make sure there is ‘no single dominant supplier’. Nonetheless, Central Asia has 65 bcm of gas deliveries scheduled which is more than anyone else. Mitrova does not believe that this figure will be achieved in reality, or at least in the contractual timeframes stated as its simply too big. However, at that rate it will be the single biggest market for this awakening dragon. There will also be around 50 bcm of LNG delivered to China, but this will come from many different suppliers with no clear player and it will be based on market tendencies. My dialogue with Mitrova took place before the recent announcements that a gas deal was reached with China, but peculiarly no price was set for the Russia gas. In effect, the deal could still collapse, or not materialise if this summer's worth of negotiations does not go through. Nevertheless, Mitrova argued that we ought to see some sort of a gas deal between Russia and China in the next two years, even though gas relations amid the two have been notoriously difficult, protracted and prone to collapses. Still, if a deal is reached its obligations, realisation, quantities and deadlines, will be substantially different from the official estimates. As quantities will be lower, deadlines will be pushed back and we can expect more difficulties along the way as usually is the case when dealing with gas and oil, and this set of players. Mitrova anticipates that a maximum of 40bcm will be piped to China, not the 70bcm officially endorsed by the government which naturally tends to optimise its goals. Also, the 2017 deadline will likely be achieved closer to 2022. Unfortunately, this puts Russia at a disadvantage as by then the Chinese market may become saturated with suppliers (e.g. if USA decided to finally allow for mass export of shale gas). In all, the official Strategy 2020 (ES-2020) and Strategy 2030 (ES-2030) are very optimistic, their figures may be achieved in the long term, but the dates set will not be hit and the fact that the latter strategy re-applies the same goals as its predecessor indicates that targets are already missed.

Central Asia has an unbeatable ‘ace’ which outweighs everything in the energy game, alongside it also being a land based supplier, which cuts out the need for sea based supplies (China fears oversupply via the sea as this can be cut off in case of war). This 'ace' is ‘equity share’ in assets. In essence, Central Asia has given China the keys to its cities via actually owning all areas of oil and gas production directly, but in Russia or elsewhere, the situation is different as China's efforts to acquire equity have come to no avail. China argues that Russia ought to give it a little and then we will see how things develop, however, Russians do not share this view, as they see it in a way that by giving someone a finger, they will take your whole hand. USA follows the same principle, perhaps even more stringently, as Daniel Yergin in his 2011 masterpiece, "The Quest", describes that the proposition for a Chinese takeover of US energy businesses is equivalent to throwing a lit match into a room filled with gas; that is how Washington's elite reacts to any such moves. So in all, this will always remain the reason why Central Asian will be the priority for China. On the other hand, as a result Central Asia is now under an incredibly strong Chinese influence, the issue of sovereignty is now all but gone in the view of Mitrova. In essence everything of value is bought or being purchased in the region: infrastructure (down to small shops), social projects (hospitals) and virtually all manufacturing alongside oil and gas. No great power, which Russia sees itself as, will concede to this, as this is in essence a neo-colonial scheme and an example of economic incursion discussed at the start. Russia did allow Rosneft to buy out BP in the bid to make a new national giant and in turn BP acquired a stake in the now world's biggest oil company in terms of raw barrel output. As part of the deal equity was exchanged, but as Mitrova highlights BP is only a junior partner which will need to consult and agree with Rosneft on all matters; China will not agree to such a minor role. In all, unfortunately, as Mitrova highlights (in reference to Simon Pirani's recent work), Central Asia has completely moved towards the Chinese market and we ought to blame the squabbling between the EU and Russia over gas matters, as whilst these were ongoing the gas/oil potential of Central Asia was lured towards China. As we are currently seeing the infrastructure is being reversed away from Europe to Asia, yet again underlining that EU's actions were once again detrimental to its energy security with an additional cost of diminished relations with Russia.

Russia's Uncertain Footing and China's Roar:

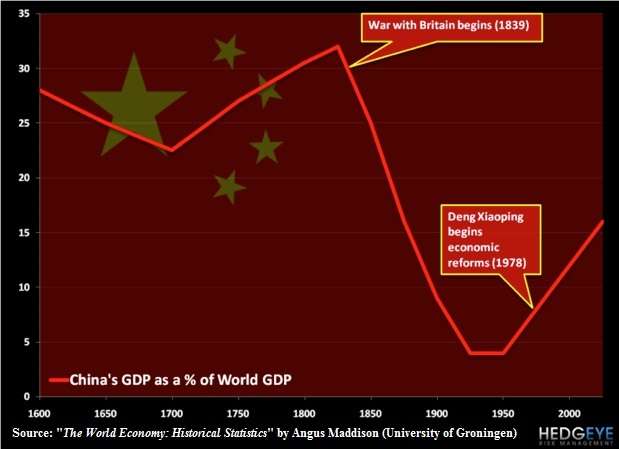

As Mitrova highlights, Russia must not be delusional about its own role in the great power's game, as from the sixth position in the global GDP rankings it will not be wheeling and dealing freely as this rank simply does not give it enough scope or strength. Russia's position will only likely to decrease in relative terms as China's growth will outpace the minor BRIC. The Energy Research Institute published a report this year: the Global & Russian Energy Outlook Up To 2040 - which I strongly recommend and I actually did a post on its predecessor the 2035 report. As the report outlines USA's global share is anticipated to fall from 19% to 14% by 2040, in contrast to China's rise from 14% to a huge 24%. It is worth noting that its not all gloom for Russia as this economy is anticipated to overtake all the European powers at 3% total of global GDP, but still be a bit part player overall. As this report draws on similar conclusions to many Western publications, one worries about the overall decline of European presence in world affairs. The re-awakening of China will bring much excitement for those that analyse the region, but for the wider world it will bring much uncertainty as it may well replace the status-quo we have today. China is still not back to its dominant position of just under 30% of global GDP, but its growing quickly and arguably in the last half-millennium it was never as strong and prospective.

Special Thanks to Dr. Tatiana Mitrova for this Discussion.

Igor Ossipov

M.A. University of Kent & Higher School of Economics, Oil/Diesel Broker and RIAC Blogger.