What’s Wrong With Oil Prices Analysis?

(no votes) |

(0 votes) |

RIAC Expert

The fall in oil prices that has transpired in several stages during 2014–2015 has resulted in the emergence of a great number of analysts and experts in the energy sector, who, seeking to gain a foothold in the lists of the most daring forecasters, preached doom with their gloomy predictions of the imminent collapse of this or that oil-producing state. They have often used the so-called fiscal break-even oil price, an indicator for oil price levels at which the state budget would break even.

The fall in oil prices that has transpired in several stages during 2014–2015 has resulted in the emergence of a great number of analysts and experts in the energy sector, who, seeking to gain a foothold in the lists of the most daring forecasters, preached doom with their gloomy predictions of the imminent collapse of this or that oil-producing state. They have often used the so-called fiscal break-even oil price, an indicator for oil price levels at which the state budget would break even. A report by Blake Clayton and Michael A. Levi entitled “Fiscal Breakeven Oil Prices: Uses, Abuses and Opportunities for Improvement” published by the U.S. Council on Foreign Relations in November 2015 examines the feasibility of its use to evaluate the economic well-being of oil-producing countries.

As Clayton and Levi point out, until 2005, is was practically unheard of to analyse the level of oil prices at which the state budget would break even in public discussions and policy documents. Against the backdrop of falling oil prices in 2008, the International Monetary Fund (IMF) published its first report, which revealed the break-even price levels for the major oil and gas producing states in the Middle East, the Maghreb and Central Asia.

Is was practically unheard of to analyse the level of oil prices at which the state budget would break even in public discussions and policy documents.

Since then, the IMF has published its estimates annually, with regular updates being released in spring and autumn. Other financial institutions (for example, Deutsche Bank and the Institute of International Finance) also conduct regular assessments of the break-even points of oil prices, but they are irregular and often significantly differ from break-even levels established by the government or the IMF.

The break-even point of oil prices determines the price level below which the state budget of an oil-producing country falls into a deficit. Theoretically speaking, the fall in oil prices below the break-even point entails certain actions on the part of the government. That is, it will seek to compensate losses at the expense of other sources of income: by raising taxes or cutting back on costs. Such actions tend to lead to an increase in social tension and, consequently, political instability. They also contribute to the change in foreign policies of oil producing countries, presumably to less ambitious behaviour.

Theory without Practice

Fall in oil prices below the break-even point entails certain actions on the part of the government. That is, it will seek to compensate losses at the expense of other sources of income.

According to the authors of the above-mentioned paper, Russia is one of the most vivid examples of how theoretical constructs fail to translate into real life. After the drop of oil prices in the spring of 2014, reports of an imminent economic and political crisis in Russia began to appear with increasing frequency. Several scenarios were mentioned: the decline of oil production by 8–10 per cent within one year; a long-term crisis in the oil sector; and – as was to be expected from the majority of Western media – the end of Vladimir Putin’s regime. It should be noted that these estimates of break-even level of oil prices differed widely. The self-proclaimed oil sector expert William Browder and members of Citigroup set that price at $117 per barrel, while analysts at Deutsche Bank put it as $105, Stratfor landed on $90. Meanwhile, Russia’s budget for 2015–2017 indicates $80 per barrel.

Although Brent Crude Futures – the pricing benchmark for Russia’s main crude varieties –fell by half in 2015 on an annualized basis (and, as of mid-December 2015, were trading at almost $35 per barrel), the fall of Vladimir Putin’s regime did not come to pass. In addition to Russia’s proactive foreign policy, which contributed to the popularity of the Russian president, the current political class managed to avoid disaster due to two factors: accumulated financial – including foreign currency – reserves, and the floating exchange rate of the Russian rouble. However, both these factors are discounted in the analysis of break-even levels of state budgets. The rouble’s floating exchange rate to some extent softened the blow of falling oil prices, since they are widely quoted in U.S. dollars, while costs are defined in the national currency.

The rouble’s floating exchange rate to some extent softened the blow of falling oil prices, since they are widely quoted in U.S. dollars, while costs are defined in the national currency.

On a separate note, the break-even price of oil for oil-producing states does not correspond directly to production costs for oil companies. In 2015, the average cost of oil production in Russia reached $17–18 per barrel. The most efficient companies, whose production cost is lower than the national average – Bashneft, Rosneft, Gazprom Neft and Lukoil – will be able to maintain their position in the oil market even with an oil price of $35 per barrel, taking transporting costs, mineral extraction tax and export duties into account (link in Russian). The situation is different for the governments of oil-producing countries, including Russia, which, due to lack of oil windfalls, may be forced to change their political and economic course. However, in practice, states whose break-even levels are much higher than the price of oil are in no hurry to change their current course.

The most efficient companies, whose production cost is lower than the national average – will be able to maintain their position in the oil market even with an oil price of $35 per barrel.

The drop in oil prices below break-even point rarely affects a government’s decision-making process. Following the basic tenets of economic theory, oil-producing states should seek to correlate the level of production with budgetary commitments. In reality, however, all countries try to avoid production cuts so as not to lose their share of the market. In the current environment of inconsistent energy policies, reduced production by one country would simply lead to its niche being filled by another without a change in global prices.

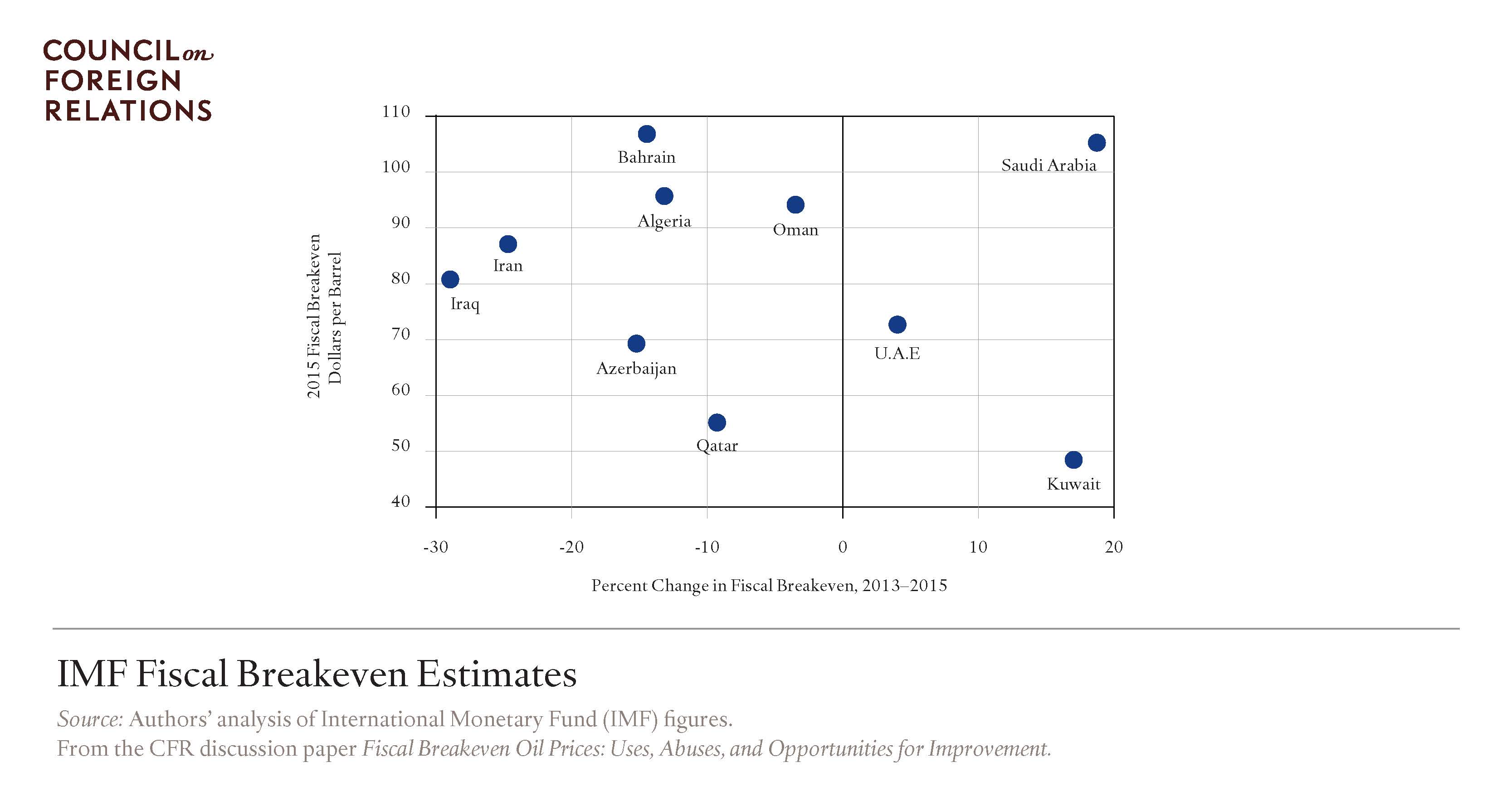

The authors also point to the fact that Saudi Arabia, having the highest spare production capacity, keeps its levels of oil production unchanged, seeking to retain its position in the United States, China and other regions of the world. Although in 2015 the break-even point for Riyadh, according to the IMF, stood at $105 per barrel, it is unlikely that global supply will see less Saudi oil. Saudi Arabia’s geopolitical interests – for example, its rivalry for power in the Middle East with Iran, also a major exporter of oil – will continue to determine its behaviour in the energy sector. Moreover, Saudi Arabia has considerable experience of living quite comfortably despite oil prices being below the break-even point: after the 1986 oil crisis, the public budget of Riyadh was in the red for 16 of the next 20 years. It is worth noting that Saudi.

public debt has fallen since 2002 and is currently less than 2 per cent of GDP. The country, therefore, is unlikely to change its energy policy, especially when you consider that only in November 2015 it discussed the possibility of issuing government bonds to consolidate its economic situation with decreasing foreign exchange reserves.

In the current environment of inconsistent energy policies, reduced production by one country would simply lead to its niche being filled by another without a change in global prices.

Other Gulf states – the United Arab Emirates (UAE), Qatar and Kuwait – also use savings accumulated during periods of high oil prices. They all increased their public spending in 2015. The United Arab Emirates controls the second largest sovereign wealth fund in the world, while Qatar controls the ninth largest, and these revenues also play a major role in covering their public budgets. As Clayton and Levi point out, with the exception of the oil sector, 40 per cent of Kuwait's revenues come from the country’s sovereign wealth fund, the Kuwait Investment Authority, and this fact should certainly be taken into account in the analysis of break-even points.

IMF (and Other) Recommendations

It is virtually impossible to determine the exact limit of oil prices beyond which a government will achieve a balanced or surplus budget, as the governments of oil-producing states have a number of measures in their arsenals to mitigate the impact of falling oil prices. However, it is possible to improve currently existing formats for determining the break-even point, primarily those used by the IMF. The authors propose their own methods for achieving this objective.

Currently, the process of calculating break-even points is not characterized by openness and transparency. The very fact that it is impossible to compare the formulae for calculating break-even points leads to situations where the break-even figures for Saudi Arabia in 2014 vary in the range of $86–97, while those for Russia are $105–117. Disclosure would also shed light on the use of such important factors as the accounting profit from sovereign investment funds in the structure of government revenue, exchange rate fluctuations, etc. It is also desirable to explain the changes made. In 2014, IMF analysts revised data for the previous year in Iraq from $117.60 to $106.10, although the figures for GDP, oil production, oil export revenues outside the oil sector and government revenue were not changed. This suggests that the formula for making the calculation changed during the revision, but the IMF report does not mention this.

The very fact that it is impossible to compare the formulae for calculating break-even points leads to situations where the break-even figures for Saudi Arabia in 2014 vary in the range of $86–97, while those for Russia are $105–117.

Moreover, the fact that the break-even point is specified in non-integral numbers implies an accuracy of estimates. Regular revisions to IMF data, however, show the opposite to be true. Thus, during 2013–2015, the break-even points for Iraq, Libya, Qatar, Kazakhstan and Turkmenistan deviated by 20 per cent or more from the original forecast for 2014. According to the authors, the IMF and other organizations should continue to determine the break-even points in price ranges that will reduce the appeal of this figure (especially among journalists), but will contribute to the greater accuracy of the analysis.

The authors also point to the fact that the IMF does not publish analyses of break-even points for countries outside the Middle East, the Maghreb and Central Asia. Such key oil exporters such as Russia, Venezuela and Mexico are not mentioned in this context, although their market position is more important than that of Azerbaijan or Turkmenistan.

According to the authors, the IMF and other organizations should continue to determine the break-even points in price ranges that will reduce the appeal of this figure but will contribute to the greater accuracy of the analysis.

Despite the above-mentioned shortcomings of the current mechanisms for analysing the break-even price of oil, it is a useful research tool when combined with indicators of the sustainability of public debt, as well as the exchange rate regime and alternative tax revenues of the country in question. Since 2002, the IMF has used Debt Sustainability Analysis, which examines the main factors of settling foreign debt and estimates the time required to improve the economic situation in a country. Consequently, an in-depth examination of acceptable debt levels is the easiest way to improve the quality of the analysis of break-even levels for oil-producing countries.

Taken as a whole, the report by Clayton and Levi is a valuable addition to the currently available body of analytics dealing with the international assessment of the sustainability of various oil-producing countries. Adhering to clear and unambiguous recommendations, the report proposes improving existing ratings to determine break-even points with a more comprehensive approach. That is why Clayton and Levi’s findings are so timely – they urge caution at a time when media hype about the future of oil prices is being fuelled by increasingly less qualified commentators.

(no votes) |

(0 votes) |